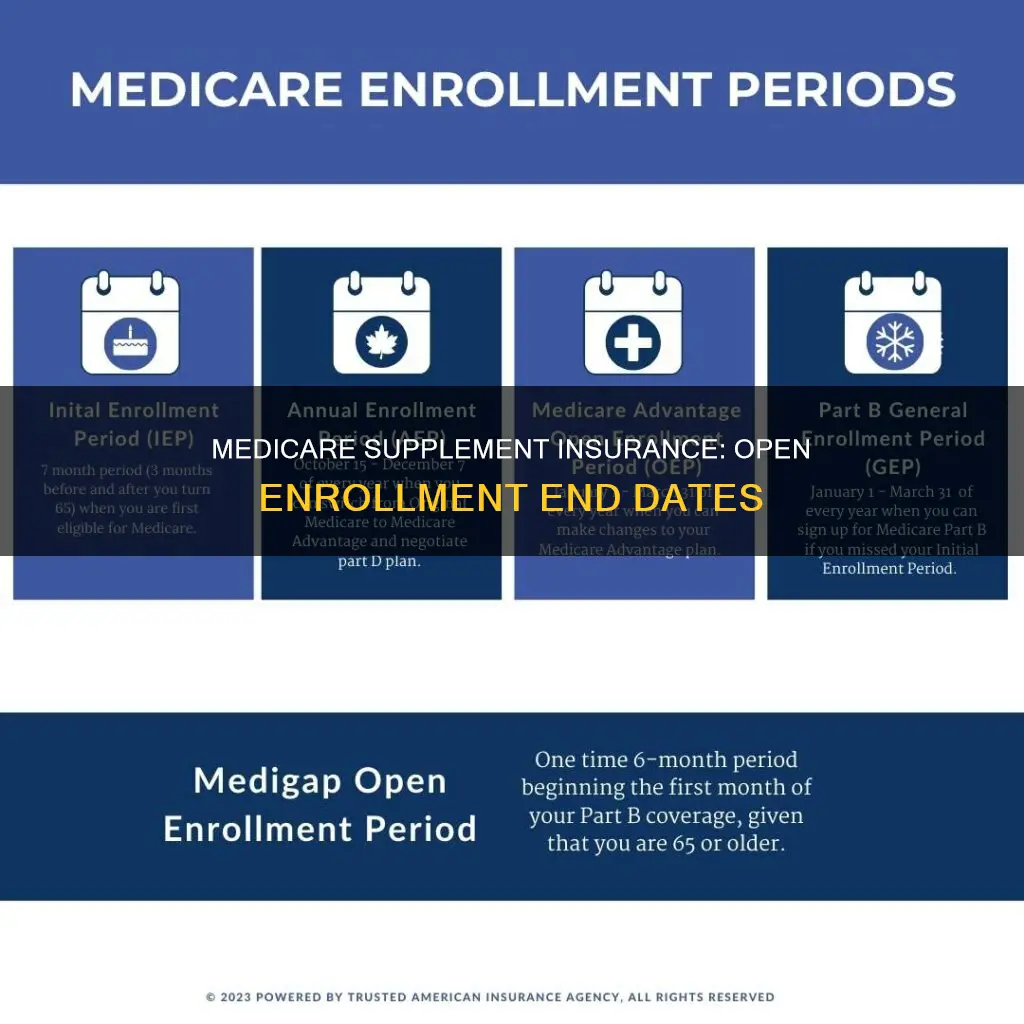

Medicare Supplement Insurance, also known as Medigap, helps cover the gaps in Original Medicare coverage, including out-of-pocket costs such as deductibles, copayments, and coinsurance. For those 65 or older enrolled in Medicare Parts A and B, there is a one-time, six-month Medigap Open Enrollment Period to purchase a Medigap policy. This period begins the first month an individual has Medicare Part B. During this time, insurance companies cannot deny coverage or charge higher premiums due to pre-existing health conditions. After this initial enrollment period ends, purchasing a Medigap policy may be more difficult and expensive, and insurance companies may consider an individual's health status when deciding on coverage.

| Characteristics | Values |

|---|---|

| Medicare Supplement Insurance plan, also known as | Medigap |

| Who can get it? | People 65 or older enrolled in Medicare Parts A and B |

| Who else can get it? | People under 65 eligible for Medicare due to disability or End Stage Renal disease |

| When is the Open Enrollment Period? | The first month you have Medicare Part B and you're 65 or older. |

| How long is the Open Enrollment Period? | 6 months |

| What happens after the Open Enrollment Period? | You may not be able to buy a Medigap policy, or it may cost more. |

| What is the best time to buy a Medigap policy? | During your Medigap Open Enrollment Period. |

| What is the Medicare Advantage Open Enrollment Period? | Jan. 1–March 31 |

| What is the Medicare Open Enrollment Period? | October 15 – December 7 |

Explore related products

What You'll Learn

![]()

Medicare Supplement Insurance is for those 65 and older

Medicare Supplement Insurance, also known as Medigap, is extra insurance that helps cover the gaps in Original Medicare coverage. This includes out-of-pocket costs like Part A and Part B deductibles, copayments, and coinsurance. These plans are offered by private insurers and can help pay costs not covered by Original Medicare.

Medicare Supplement Insurance is available to those aged 65 and older who are enrolled in Medicare Parts A and B. In some states, it is also available to those under 65 who are eligible for Medicare due to a disability or End-Stage Renal Disease (ESRD). Federal law does not require insurance companies to sell Medigap policies to people under 65, but some states do offer this option.

The Medicare Supplement Open Enrollment Period is a one-time, 6-month window that begins the first month an individual is enrolled in Medicare Part B and is 65 or older. During this time, individuals can enroll in any Medigap policy, and insurance companies cannot deny coverage due to pre-existing health problems. They must also offer the same price as those in good health.

After the open enrollment period ends, insurance companies may consider an individual's health status when deciding whether to sell a policy, and they may charge higher premiums or deny coverage based on pre-existing conditions. Therefore, it is essential to enroll during the open enrollment period to avoid potential higher costs and ensure coverage.

Medicare Supplement Insurance plans are standardized by the federal government and named with letters like A, F, G, and N. The benefits in each lettered plan are the same across insurance companies, with the price being the only difference. These plans do not include prescription drug, dental, or vision coverage, but standalone plans for these benefits can be purchased separately.

Medical Insurance for Bellies: What's Covered and What's Not

You may want to see also

Explore related products

![]()

It's a one-time, 6-month enrollment period

Medicare Supplement insurance, also known as Medigap, helps cover the gaps in Original Medicare coverage, including out-of-pocket costs like deductibles, copayments, and coinsurance. It is available to individuals aged 65 and older enrolled in Medicare Parts A and B and, in some states, to those under 65 who are eligible for Medicare due to a disability or End Stage Renal Disease (ESRD).

The Medigap Open Enrollment Period is a one-time, 6-month enrollment period that begins the first month an individual is 65 or older and enrolled in Medicare Part B. During this time, individuals can enroll in any Medigap policy sold in their state without being denied coverage due to pre-existing health problems. They will generally get better prices and more choices among policies.

After the Medigap Open Enrollment Period ends, individuals may not be able to buy a Medigap policy, or it may cost more. It is important to note that the Medigap Open Enrollment Period is not the same as the yearly Medicare Open Enrollment Period, which occurs from October 15 to December 7, during which individuals with Medicare can change their Medicare health plans and prescription drug coverage for the following year.

While the Medigap Open Enrollment Period is a one-time opportunity, there are certain situations where individuals may be able to buy a Medigap policy outside of this period. These situations are called "guaranteed issue rights" or "Medigap protections," and they vary by state. For example, individuals may qualify if they lose other health coverage or move out of the service area of their current plan. Additionally, individuals have 63 days after their current Medigap coverage ends to buy a new Medigap policy, and their rights may last an extra 12 months in certain circumstances.

In summary, the Medigap Open Enrollment Period is a one-time, 6-month window that offers the best opportunity to enroll in a Medigap policy with a wide range of choices and competitive pricing. Missing this enrollment period may result in limited options and higher costs. However, individuals should be aware of their rights and alternative enrollment opportunities outside of this period.

Understanding Pretax Medical Insurance Benefits and Savings

You may want to see also

Explore related products

![]()

It begins the first month you have Medicare Part B

Medicare Supplement Insurance, also known as Medigap, is available to those aged 65 and over who are enrolled in Medicare Parts A and B. In some states, those under 65 may be eligible for Medicare due to disability or End-Stage Renal Disease.

If you are 65 or over, you can enrol in a Medicare Supplement Insurance plan beginning the first month you have Medicare Part B. This is a one-time, 6-month open enrolment period. During this time, you can enrol in any Medigap policy sold in your state, and insurance companies cannot deny you coverage due to pre-existing health problems. You will also generally get better prices and more choices among policies.

After this initial 6-month period, you may not be able to buy a Medigap policy, or it may cost more. Your Medigap Open Enrollment Period is a one-time enrolment period and does not repeat every year like the standard Medicare Open Enrollment Period.

If you are under 65 and have Medicare because of a disability or ESRD, you might not be able to buy a Medigap policy until you turn 65. Federal law does not require insurance companies to sell Medigap policies to people under 65, although some states do offer policies to those under 65.

Becoming a Medicaid Insurance Agent in New York

You may want to see also

Explore related products

![]()

You can buy any Medigap policy sold in your state

Medicare Supplement insurance, also known as Medigap, helps cover the "gaps" in Original Medicare coverage. This includes out-of-pocket costs like Part A and Part B deductibles, copayments, and coinsurance. These plans are offered by private insurers and can help pay costs not covered by Original Medicare.

Medigap policies are available to those aged 65 and older enrolled in Medicare Parts A and B and, in some states, to those under 65 eligible for Medicare due to disability or End Stage Renal Disease (ESRD). Federal law does not require insurance companies to sell Medigap policies to people under 65, but some states do offer these policies to individuals in this age group.

Under federal law, individuals are granted a 6-month Medigap Open Enrollment Period. This period begins the first month an individual has Medicare Part B and is 65 or older. During this time, individuals can enrol in any Medigap policy, and insurance companies cannot use medical underwriting to decide whether to accept an application. In other words, they cannot deny coverage due to pre-existing health problems.

After this initial 6-month period, it may be more difficult to purchase a Medigap policy, and it may cost more. However, there are certain situations where individuals may be able to buy a Medigap policy outside of this open enrollment period. These situations are called "guaranteed issue rights" or "Medigap protections," and they vary by state. To understand your guaranteed issue rights, it is recommended to check with your State Insurance Department.

When purchasing a Medigap policy, individuals can buy any Medigap policy sold in their state. It is important to note that not all plans are offered in every state, and the availability of insurance companies selling specific plans may vary. To purchase a Medigap policy, individuals should follow these steps:

- Find insurance companies selling the desired plan.

- Compare the same lettered plans offered by different insurance companies, as the benefits in each lettered plan are the same regardless of the company.

- Shop by price, as the cost is the only difference between policies with the same letter offered by different companies. Contact multiple companies to get estimates.

- Contact your State Insurance Department to check for any complaints against the insurance companies selling the desired plan.

- Ask for your Medigap policy to become effective when you want coverage to start. Generally, Medigap policies begin on the first day of the month after applying, but individuals can decide when they want the coverage to start.

- Contact the chosen insurance company and fill out the application. The insurance company must provide a clearly worded summary of the Medigap policy, which should be carefully reviewed and kept for records.

- If you do not receive your Medigap policy within 30 days, call your insurance company. If it has been 60 days and you have not received your policy, call your State Insurance Department.

- Keep all letters, notices, emails, or claim denials from your Medigap policy, as these may be needed to prove your coverage if you decide to change your plan in the future.

It is important to be vigilant about illegal practices by insurance companies and to protect yourself when shopping for a Medigap policy. Additionally, individuals with employer or union coverage, Medicaid, or coverage through the Health Insurance Marketplace should refer to specific guidelines provided by Medicare to understand their options for purchasing a Medigap policy.

Applying for Medical Insurance in Illinois: A Guide

You may want to see also

Explore related products

![]()

You can avoid waiting periods for pre-existing conditions

Medicare Supplement Insurance, also known as Medigap, is available to those aged 65 and over who are enrolled in Medicare Parts A and B. It is also offered in some states to those under 65 who are eligible for Medicare due to a disability or end-stage renal disease.

Medicare Supplement Insurance plans are sold by private health insurance companies, which are usually allowed to use medical underwriting when evaluating insurance applications. However, there is a six-month Medigap Open Enrollment Period, during which insurers cannot use medical underwriting when considering your application. This period begins on the first day of the month in which you are 65 or older and enrolled in Medicare Part B.

During this time, insurance companies cannot refuse to sell you a policy based on your pre-existing condition and cannot charge you more than someone without health problems. This means that you can avoid waiting periods for pre-existing conditions by buying a Medigap policy during the Open Enrollment Period.

If you had six or more months of creditable coverage before enrolling, the Medigap carrier must provide coverage immediately. Creditable coverage could include individual health insurance, group health insurance, or military retiree benefits. However, if you have a gap of over 63 days, you cannot use creditable coverage to reduce your pre-existing condition waiting period.

If you miss the Open Enrollment Period, you will need to answer underwriting health questions when signing up for your policy. In this case, you may need to wait six months for your pre-existing condition to be covered. These pre-existing condition waiting periods only apply to Medigap policies, and federal law does not require insurers to cover pre-existing conditions for the first six months.

Medicaid Insurance: Where and How to Get Covered

You may want to see also

Frequently asked questions

The open enrollment period for Medicare Supplement Insurance, also known as Medigap, is a one-time, 6-month period that starts the first month you are 65 or older and enrolled in Medicare Part B.

Yes, in some cases, you may be able to buy a Medigap policy outside of the open enrollment period. These situations are called "guaranteed issue rights" or "Medigap protections." Check with your State Insurance Department to see if you qualify.

The best time to buy a Medigap policy is during the open enrollment period. After this period, your options may be limited, and the policy may cost more.

The Medicare Supplement Insurance Plan, also known as Medigap, helps cover the "gaps" in Original Medicare coverage. This includes out-of-pocket costs like deductibles, copayments, and coinsurance.

The Medicare Open Enrollment Period is when people with Medicare can change their health plans and prescription drug coverage for the following year. This period usually occurs annually from October 15 to December 7.