Medicare Supplement Insurance, also known as Medigap, is an extra insurance policy that can be purchased from a private insurance company to help pay for out-of-pocket costs in Original Medicare. Medigap policies are standardized, meaning that policies with the same letter offer the same basic benefits regardless of location or insurance company. Individuals aged 65 or older who are enrolled in Medicare Parts A and B are eligible for Medicare Supplement Insurance, and they have a one-time, 6-month open enrollment period to enroll in a Medigap policy without being subject to medical underwriting. During this period, insurance companies cannot deny coverage due to pre-existing health conditions. After this initial enrollment period ends, individuals may face limited options and higher costs for Medigap policies. To enroll in a Medigap policy, individuals can compare plans, select a plan that meets their needs, and contact the insurance company to fill out an application. It is important to carefully review the summary of the Medigap policy and be aware of potential illegal practices by insurance companies.

| Characteristics | Values |

|---|---|

| What is Medicare Supplement Insurance? | Extra insurance to help pay your share of out-of-pocket costs in Original Medicare. Also known as Medigap. |

| Who can buy it? | Those aged 65 and older enrolled in Medicare Parts A and B. In some states, those under 65 with Medicare due to disability or End Stage Renal Disease may also be eligible. |

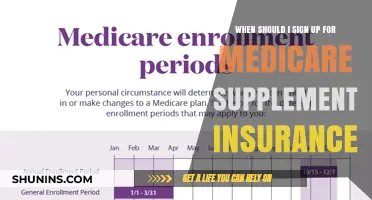

| When can you enroll? | There is a one-time 6-month Medigap Open Enrollment Period that starts the first month you have Medicare Part B and are 65 or older. |

| Where can you enroll? | You can buy a Medigap policy from any insurance company that's licensed in your state to sell one. |

| How to enroll? | Compare plans, select the plan that meets your needs, and contact the company to fill out the application. |

Explore related products

What You'll Learn

![]()

Enrollment criteria

Medicare Supplement Insurance, also known as Medigap, is an extra insurance policy that can be purchased from a private insurance company. It helps cover the gaps in Original Medicare, including out-of-pocket costs like deductibles, copayments, and coinsurance. To be eligible for Medicare Supplement Insurance, certain criteria must be met:

- You must be 65 or older and enrolled in Medicare Parts A and B. In some states, those under 65 who are eligible for Medicare due to disability or End Stage Renal Disease may also qualify.

- You must reside in the service area of the plan you wish to join.

- You must be a U.S. citizen or lawfully present in the U.S.

- You must have your Medicare Number and your Part A and/or Part B coverage start dates, which can be found on your Medicare card.

- It is important to note that you can only buy Medigap if you have Original Medicare, which includes Medicare Part A (Hospital Insurance) and Part B (Medical Insurance).

- You will have a one-time, 6-month Medigap Open Enrollment Period that starts the first month you have Medicare Part B and you are 65 or older. During this time, you can enroll in any Medigap policy, and the insurance company cannot deny you coverage due to pre-existing health conditions. After this period, your ability to purchase a Medigap policy may be restricted, and the cost may increase.

- You can purchase any Medigap policy sold by an insurance company in your state.

- To enroll, select the "Enroll" option for your chosen plan at Medicare.gov/plan-compare, or contact the plan directly by phone, website, or paper form.

- Before purchasing a Medigap policy, it is recommended to compare the benefits of each lettered plan, consider your current and future healthcare needs, and decide which benefits are most important to you.

- Remember to review the Medigap policy summary provided by the insurance company carefully and keep it for your records. If you have any questions, be sure to ask for clarification.

- Keep in mind that Medigap policies are standardized, meaning policies with the same letter offer the same basic benefits regardless of your location or insurance company. The price is the only difference between plans with the same letter sold by different companies.

Medical Insurance and Chemotherapy: What's Covered?

You may want to see also

Explore related products

![]()

Plan options

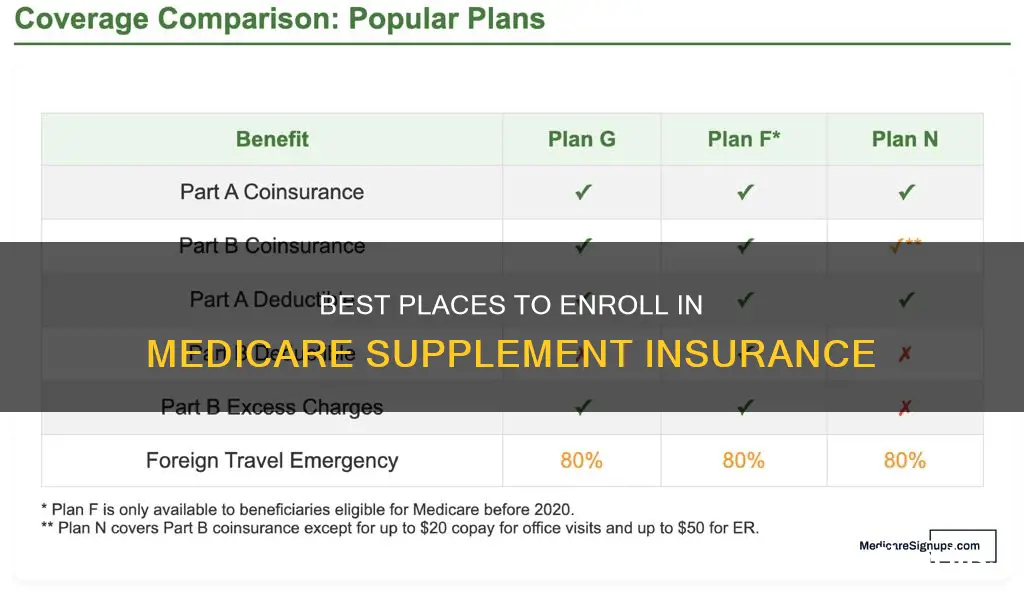

Medicare Supplement Insurance, also known as Medigap, is extra insurance that can be purchased from a private insurance company to help pay for out-of-pocket costs in Original Medicare. Medigap policies are standardized, meaning that policies with the same letter offer the same basic benefits regardless of location or insurance company. There are 10 different types of Medigap plans offered in most states, named by letters: A-D, F, G, and K-N. The price is the only difference between plans with the same letter sold by different companies.

To enroll in a Medigap policy, individuals must already have Original Medicare, which includes Medicare Part A (Hospital Insurance) and Part B (Medical Insurance). The best time to buy a Medigap policy is during the Medigap Open Enrollment Period, which is a one-time, 6-month period that begins the first month an individual is 65 or older and enrolled in Medicare Part B. During this period, individuals cannot be denied coverage due to pre-existing health conditions. After the Medigap Open Enrollment Period ends, insurance companies may deny coverage or charge higher premiums based on health status and pre-existing conditions.

In some cases, individuals may be able to buy a Medigap policy outside of the Medigap Open Enrollment Period. These situations are called "guaranteed issue rights" or "Medigap protections" and may apply if an individual loses other health coverage or moves out of the service area of their Medicare Advantage Plan. To explore plan options and determine eligibility, individuals can contact their State Insurance Department or the Medicare hotline at 1-800-MEDICARE.

It is important to compare the benefits of each lettered plan and consider current and future healthcare needs before selecting a Medigap policy. Once an individual decides on a plan, they can contact the insurance company to fill out an application and receive a summary of their Medigap policy. Additionally, individuals can seek free help from their local State Health Insurance Assistance Program (SHIP) to choose an insurance company and plan that best meets their needs.

VA Medical Insurance: Can I Join My Husband's Plan?

You may want to see also

Explore related products

![]()

Enrollment timing

Medicare Supplement Insurance, also known as Medigap, is an extra insurance policy that you can buy from a private insurance company. It helps cover the "gaps" in Original Medicare, including out-of-pocket costs like Part A and Part B deductibles, copayments, and coinsurance.

Medigap is only available to those aged 65 and over who are enrolled in Medicare Parts A and B. In some states, it is also offered to those under 65 who are eligible for Medicare due to disability or End Stage Renal Disease.

The best time to buy a Medigap policy is during your Medigap Open Enrollment Period. This is a one-time, 6-month enrollment period that starts the first month you have Medicare Part B and are 65 or older. During this time, you can enroll in any Medigap policy, and the insurance company cannot deny you coverage due to pre-existing health problems.

After the Medigap Open Enrollment Period ends, insurance companies are not required to sell you a Medigap policy, and your options may be limited. However, there are certain situations where you may be able to buy a Medigap policy outside of this period, called "guaranteed issue rights" or "Medigap protections." For example, you may qualify if you lose other health coverage or if you have a Medicare Advantage plan and move out of the plan's service area.

You can buy a Medigap policy from any insurance company licensed in your state to sell one. Not all plans are offered in every state, and the price is the only difference between plans with the same letter sold by different companies. You can contact your State Insurance Department or your local State Health Insurance Assistance Program (SHIP) to get more information and help choosing an insurance company.

AmFirst Insurance: Understanding the Connection with Medicaid

You may want to see also

Explore related products

![Medicare and Social Security: [5 in 1] Maximize Your Retirement Benefits, Secure Medical Coverage and Quality Healthcare | Proven Strategies to Protect Your Financial Future Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/71sRJGiWeQL._AC_UL320_.jpg)

![]()

Enrollment process

Medicare Supplement Insurance, also known as Medigap, is extra insurance you can buy from a private insurance company to help pay your share of out-of-pocket costs in Original Medicare. To be eligible for Medicare Supplement Insurance, you must be enrolled in Original Medicare, which includes Medicare Part A (Hospital Insurance) and Part B (Medical Insurance).

Step 1: Compare Plans

Compare the benefits of each lettered plan (e.g., Plan A, Plan B, etc.) and consider your current and future healthcare needs. Remember that not all plans are offered in every state, and the availability of plans may vary among insurance companies. You can use resources such as the State Health Insurance Assistance Program (SHIP) to get free help in choosing a plan and understanding your options.

Step 2: Select a Plan

Choose a plan that meets your specific needs and healthcare requirements. Consider factors such as the benefits offered, the premium costs, and the reputation of the insurance company. Review the standardized benefits of each lettered plan to ensure you understand what is covered.

Step 3: Check Eligibility

Ensure that you meet the eligibility criteria for Medicare Supplement Insurance. Generally, you must be 65 or older and enrolled in Medicare Part A and Part B. However, in some states, individuals under 65 who are eligible for Medicare due to disability or End Stage Renal Disease may also qualify for Medicare Supplement Insurance.

Step 4: Understand Enrollment Periods

Medigap policies have a one-time "Medigap Open Enrollment Period" that lasts for 6 months. This period begins the first month you have Medicare Part B and are 65 or older. During this time, you are guaranteed the right to buy any Medigap policy sold in your state, and insurance companies cannot deny you coverage due to pre-existing health conditions.

Step 5: Contact the Insurance Company

Once you have selected a plan and confirmed your eligibility, contact the insurance company directly. You can do this by phone, through their website, or by requesting a paper application form. Be prepared to provide the necessary information, such as your Medicare number and coverage start dates.

Step 6: Complete the Application

Fill out the application form provided by the insurance company. Provide accurate and complete information, and do not hesitate to ask questions if you need clarification. Remember to carefully review the Medigap policy summary provided by the insurance company before finalizing your application.

Step 7: Submit Required Documentation

Along with your application, you may need to submit supporting documentation. This could include copies of letters, notices, emails, or claim denials from your previous coverage. These documents help prove your coverage details and confirm your right to purchase a Medigap policy.

Step 8: Wait for Confirmation

After submitting your application and documentation, wait for confirmation from the insurance company. Keep in mind that Medigap policies typically begin on the first day of the month after you apply. If you do not receive your Medigap policy or proof of insurance within 30 days, contact the insurance company to follow up.

Please note that specific steps may vary, and it is always advisable to consult official Medicare resources or speak with a Medicare representative for the most accurate and up-to-date information regarding enrollment processes and requirements.

Alabama's Free Medical Insurance: Application and Eligibility

You may want to see also

Explore related products

![]()

Choosing an insurer

Medicare Supplement Insurance, also known as Medigap, is extra insurance that you can buy from a private insurance company to help pay your share of out-of-pocket costs in Original Medicare. It's important to choose a reputable insurer that offers a Medigap policy that meets your specific needs. Here are some factors to consider when choosing an insurer for your Medicare Supplement Insurance:

- Standardization of Policies: All Medigap policies are standardized, which means that policies with the same letter offer the same basic benefits regardless of the insurance company. There are 10 different types of Medigap plans offered in most states, named by letters: A-D, F, G, and K-N. Make sure you understand the benefits associated with each lettered plan and choose the one that best suits your current and future healthcare needs.

- Price Comparison: While the benefits of plans with the same letter are consistent across insurance companies, the price can vary. Shop around and contact multiple companies that offer Medigap policies in your state to get estimates. Compare the prices for the same lettered plan across different insurers to find the most cost-effective option.

- State Availability: Not all plans are offered in every state, and even if a plan is available in your state, not all insurance companies sell policies for it. Check with your state's insurance department or utilize the State Health Insurance Assistance Program (SHIP) to find out which insurers offer Medigap plans in your state.

- Company Reputation and Complaints: Research the reputation of the insurance companies you are considering. Contact your State Insurance Department to inquire about any complaints or issues reported against the insurers you are evaluating. This can help you identify companies with a history of customer satisfaction and avoid potential problems.

- Clear Policy Summary: When you are ready to buy, contact the insurance company and carefully review the Medigap policy summary they provide. Ensure that the summary is clearly worded and that you understand the coverage, benefits, and any potential limitations or exclusions. Don't hesitate to ask questions if anything is unclear.

- Enrollment Periods: Keep in mind that the best time to buy a Medigap policy is during your Medigap Open Enrollment Period, which is a one-time, 6-month period starting when you turn 65 and have Medicare Part B. During this period, insurance companies cannot deny you coverage due to pre-existing health conditions. After this period, your options may be limited, and the policy might cost more.

By considering these factors and comparing policies from different insurers, you can make an informed decision when choosing an insurer for your Medicare Supplement Insurance. Remember to select a plan that aligns with your healthcare needs and choose a reputable company that offers competitive pricing and clear policy details.

Emergency Room Visits: No Insurance, Now What?

You may want to see also

Frequently asked questions

You can enroll in Medicare Supplement Insurance (Medigap) by selecting "Enroll" for the plan you want to join at Medicare.gov/plan-compare. You can also contact the plan to join by calling them, visiting their website, or asking for a paper form to fill out and mail back to the plan.

If you are 65 or older and enrolled in Medicare Part B, you can enroll in Medicare Supplement Insurance during the 6-month Medigap Open Enrollment Period that starts the first month of Part B coverage. This is a one-time enrollment period.

To enroll in Medicare Supplement Insurance, you must have Medicare Part A (Hospital Insurance) and Part B (Medical Insurance), live in the service area of the plan, and be a U.S. citizen or lawfully present in the U.S. You will need your Medicare Number and your Part A and/or Part B coverage start dates, which can be found on your Medicare card.

![The Medicare Bible for Beginners: [3 in 1] Unlock Medical Benefits and Quality Healthcare | Super Easy Insider Strategies to Navigate Medicare While Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/71tm-tSiWnL._AC_UL320_.jpg)