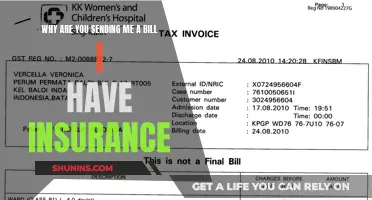

It can be frustrating to receive a bill for a service you thought your insurance had covered. This can happen for a number of reasons, such as the service being out-of-network or the insurance company requiring you to cover all costs until you reach a specified amount (known as a deductible). In some cases, the bill may be a mistake, and it's important to know your rights and how to appeal the charge if this is the case. If you have already paid for your treatment, your insurance company should reimburse you for any services covered under your claim. If you have not paid, the insurance company will pay the provider directly. It's always a good idea to check that the bill is correct and that you have not already paid it.

| Characteristics | Values |

|---|---|

| Reasons for receiving a bill after insurance has paid | The bill may be a "surprise medical bill" from an out-of-network provider or facility. |

| What to do if you receive a bill | 1. Check if the bill contains the words "insurance pending" or another indication that it has been submitted to the insurance company. 2. If not, call the doctor or hospital and ask them to bill your insurance company. 3. If they refuse or are unable to do so, fill out a reimbursement form and submit it along with the bill or statement. |

| How to avoid surprise medical bills | 1. Get a "good faith" estimate of costs before receiving care. 2. Understand your insurance plan's coverage limits, deductibles, and appeal rights. |

Explore related products

What You'll Learn

- You may have reached your maximum out-of-pocket (MOOP) expense limit for the year

- The bill could be a surprise medical bill from an out-of-network provider

- The bill is an Explanation of Benefits (EOB) from your insurance plan

- You may have to pay a copay (short for copayment)

- You may have to pay coinsurance, a percentage of the total costs

![]()

You may have reached your maximum out-of-pocket (MOOP) expense limit for the year

Once you reach this amount, you will not owe cost-sharing for Part A or Part B covered services for the remainder of the year. This means that Medicare Part A will help cover hospital costs if you are admitted as an inpatient to a hospital, and Medicare Part B will help cover your medical costs for doctor office visits and similar healthcare. After you reach your MOOP, you will not owe cost-sharing for these services for the rest of the year. Some plans may also apply the MOOP to supplemental benefits, such as vision, hearing, or dental.

The point of MOOP limits is to prevent beneficiaries from being burdened with never-ending or out-of-control expenses due to something like an ongoing health issue that requires continuous treatment. The limit is set high, but it may protect you from excessive costs if you need a lot of care or expensive treatments. For example, let's say you have an insurance plan with a $4,000 MOOP. You've had doctors' appointments and an emergency room visit, for which you paid your copays, your $400 deductible, and $3,600 in coinsurance. Once you've paid a total of $4,000, your insurance company will cover 100% of your medical expenses for the rest of the plan year.

Unlocking the Tricare Insurance Billing Process: A Comprehensive Guide

You may want to see also

Explore related products

$18.04 $36.99

![]()

The bill could be a surprise medical bill from an out-of-network provider

Surprise medical bills are a common occurrence in the US, with 2 in 3 adults worrying about unexpected medical bills. These bills arise when patients receive care from out-of-network providers or facilities, often in emergencies when patients have little to no say in where they receive care. They can also occur when patients at in-network hospitals receive care from ancillary providers who are not in-network, such as anesthesiologists.

If you receive a surprise medical bill, there are a few steps you can take to resolve the issue:

- Check your insurance plan: Many insurance companies require you to cover all costs until you reach a specified amount, known as a deductible. Once you reach this amount, the insurance company starts paying for covered services. Check if you have met your deductible for the year.

- Contact your insurance company: If you have met your deductible, contact your insurance company to clarify what is covered under your plan. Ask about any outstanding payments and confirm that they have processed the claim.

- Review the bill for errors: Medical billing errors are common, and it is possible that you were incorrectly billed. Contact the healthcare provider and ask for an itemized bill to review the charges.

- Appeal the bill: If you believe the bill is incorrect, you have the right to appeal the decision. Contact your insurance company to initiate the appeal process and provide any necessary documentation to support your case.

- Dispute the charges: If you are uninsured or self-paying, you may be able to dispute the charges if your final bill is significantly higher than the initial good faith estimate. You can use a third-party arbitrator or a state-specific dispute resolution process to resolve the dispute.

- Seek help from a Consumer Assistance Program (CAP): CAPs are available in many states and can help you understand your rights and resolve problems with health plans and providers.

It is important to stay organized and keep records of all communications and payments related to your medical care. Additionally, be sure to review your insurance plan and understand your coverage and responsibilities for medical costs. Knowing what is covered and what your out-of-pocket expenses will be can help you identify any unexpected charges.

Unraveling the Intricacies of Insurance Reserves: A Guide to Understanding This Crucial Concept

You may want to see also

Explore related products

![]()

The bill is an Explanation of Benefits (EOB) from your insurance plan

If you've received a bill from your doctor or healthcare provider and you're insured, it's likely that this is an Explanation of Benefits (EOB) from your insurance plan. An EOB is not a bill, but rather a statement or report from your insurance company that explains how your insurance processed the claim for the services you received. It's a useful document that shows you how your bill is broken down between the medical service provider(s), your insurance, and you. It can help ensure you are receiving the full benefit or discount that you are entitled to under your insurance plan.

An EOB will usually include the following:

- Personal details such as your name, member number, and plan information

- Information about your visit, including the date(s) of service, your doctor or clinic's name, and the type of care you received (e.g. preventive care or office visit)

- A breakdown of the charges for the service(s) received, so you can see how much your insurance company paid and the amount you owe

- A summary of deductible and out-of-pocket maximums

- Any reason codes explaining why a claim has been denied

If you receive an EOB, don't pay your clinic or hospital bill until you receive a separate bill from your doctor or healthcare provider. This way, you can be confident that you're not paying more than you owe.

**Understanding Short-Term Recovery Insurance: A Safety Net for the Unexpected**

You may want to see also

Explore related products

![]()

You may have to pay a copay (short for copayment)

A copay, or copayment, is a fixed dollar amount that you pay every time you receive medical care. This is a standard part of many health insurance plans and is usually paid at the time of the service. Copayments are different from deductibles, which are much larger sums, and coinsurance, which is a percentage of the bill.

Copayments are typically $25 or less and are often charged for services such as doctor visits or prescription drugs. The amount you pay for a copayment depends on the type of health plan you have and the type of doctor or specialist you see. For example, the copayment to see a specialist may be higher than the copayment to see your primary care physician.

Copayments are also usually higher for out-of-network providers than for in-network providers. It is important to be aware of how much out-of-network providers charge for copayments, especially if you are making recurring visits. Additionally, copayment amounts may change annually, so it is worth checking in with your insurance company or HR department to find out if the amounts have increased.

Copayments are one component of your out-of-pocket expenses. Other out-of-pocket expenses may include coinsurance, annual deductibles, and the cost of services not covered by your plan.

Demystifying Emergency Room Bills: Strategies for the Uninsured

You may want to see also

Explore related products

![]()

You may have to pay coinsurance, a percentage of the total costs

Coinsurance is the percentage of covered health costs that you are responsible for paying after you've met your deductible. Typically, coinsurance operates on a fixed ratio, meaning you'll always be charged the same percentage of the total bill each time. Many insurance companies operate on an 80/20 coinsurance plan, meaning your insurance company pays 80% of the total bill, and you pay the remaining 20%.

Coinsurance is different from a copay, which is a set dollar amount that you pay every time you receive medical care. For example, you might have a $20 copay for a non-preventative doctor visit, meaning you pay $20 regardless of whether the total cost for the visit is $100 or $300. However, a 20% coinsurance fee would vary depending on the cost of the service. Another key difference is that coinsurance only applies after you've met your deductible, whereas a copay can apply both before and after you've met your deductible.

Coinsurance payments contribute to your out-of-pocket maximum. That means you'll pay your coinsurance percentage until you reach your out-of-pocket maximum. Once you reach the maximum limit, you stop paying coinsurance, and your insurance company covers 100% of the remaining costs for covered services.

Coinsurance is also different from a deductible, which is the amount you pay each year for eligible medical services before your health plan begins to share in the cost of covered services. For example, if you have a $2,000 deductible, you'll need to pay the first $2,000 of your total eligible medical costs before your plan helps to cover a portion of the costs. After meeting your deductible, you may be responsible for paying coinsurance.

When it comes to out-of-network care, the coinsurance rate may be higher than what you'd pay for in-network care. In some cases, your insurance provider won't cover any of the costs for out-of-network providers, meaning you'll be responsible for the entire bill. Therefore, it's important to carefully review the coinsurance rates and policies of your insurance plan before enrolling to avoid surprises when your billing statement arrives.

Term Insurance: Understanding the Wait for Coverage

You may want to see also

Frequently asked questions

First, check if the bill contains the words "insurance pending" or any indication that the hospital/doctor has submitted the bill to the insurance company. If it does not, call the doctor or hospital and ask them to bill your insurance company. If they refuse or are unable to do so, fill out a reimbursement form and send it to your insurance company.

A surprise medical bill is an unexpected bill from an out-of-network provider or facility. Your health insurance may not cover the entire out-of-network cost, leaving you with a higher bill than if you had received care from an in-network provider.

The No Surprises Act is a law that protects people covered under group and individual health plans from receiving surprise medical bills when they receive emergency services, non-emergency services from out-of-network providers at in-network facilities, and services from out-of-network air ambulance service providers. It establishes an independent dispute resolution process for payment disputes and provides new dispute resolution opportunities for the uninsured and self-pay individuals.

If you receive a surprise medical bill, you may be able to dispute the charges. Contact the Centers for Medicare & Medicaid Services No Surprises Help Desk at 1-800-985-3059 or submit a complaint online. You can also contact your state Consumer Assistance Program for help with health insurance problems or questions about health coverage options.

An Explanation of Benefits (EOB) is a report from your health insurance plan that outlines what services are covered and how much your insurance plan will pay, based on the care you received and your health plan benefits. It is not a bill, and you should not pay anything until you receive a separate bill from your doctor for any remaining amount owed.