Whole life insurance is a type of permanent life insurance that offers lifelong coverage and provides a death benefit payout to beneficiaries when the insured person passes away. It is designed for individuals seeking lifetime protection and tax-advantaged benefits. While it may not be suitable for everyone due to its high cost, whole life insurance can be beneficial for those who want to ensure their family's financial security, especially if they have lifelong dependents or children with disabilities. This type of insurance also accumulates a cash value over time, which can be used to supplement retirement income or cover expenses.

Explore related products

What You'll Learn

![]()

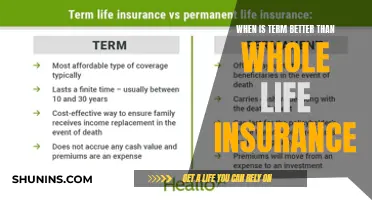

Whole life insurance vs. term life insurance

Whole life insurance and term life insurance are two types of life insurance policies that offer financial security to your loved ones in the event of your death. While both policies offer death benefit protection, there are crucial differences between the two in terms of cost, coverage length, cash value, and complexity.

Whole life insurance is a permanent policy that offers lifelong coverage. This means that it will pay out to your beneficiaries regardless of when you pass away, as long as you continue to pay the premiums. Whole life insurance tends to be more expensive than term life insurance due to its lifelong coverage and the inclusion of a cash value component. The cash value of a whole life insurance policy grows over time, providing a tax-advantaged investment opportunity. This cash value can be borrowed against or withdrawn to help cover expenses or meet financial goals. However, whole life insurance is more complex than term life insurance due to its investment component and permanent nature.

On the other hand, term life insurance provides coverage for a specific term or set period of time, typically ranging from 10 to 30 years. It is more affordable than whole life insurance because of its limited coverage period and the absence of a cash value feature. Term life insurance is simpler and easier to understand, making it a popular choice for young families and those seeking low-cost coverage. However, if you outlive the term length, your coverage will end and your beneficiaries will not receive any benefits.

When deciding between whole life and term life insurance, it is important to consider your financial goals, budget, and specific needs. Whole life insurance may be suitable if you require lifelong coverage, desire the investment potential of the cash value component, and can afford the higher premiums. On the other hand, term life insurance may be preferable if you only need coverage for a certain period, such as while your children are dependent on you, or if you are seeking a more affordable option. Additionally, term life insurance can be used to supplement a whole life policy during certain life events, such as buying a home.

Instant Life Insurance: When Does Coverage Start?

You may want to see also

Explore related products

![]()

Pros and cons of whole life insurance

Whole life insurance is a permanent policy that offers lifelong coverage. It is designed to last your entire life and never expires as long as you continue to pay the premiums, which remain fixed. It provides a death benefit payout to beneficiaries, which is generally tax-free, and can help build cash value, which accrues interest over time.

Pros

- Whole life insurance offers lifelong coverage with no termination date, providing financial security to your loved ones no matter when you pass away.

- The premiums remain fixed, making it easy to budget for them.

- It offers a cash value growth component. The cash value can be withdrawn or borrowed against to cover expenses or meet financial goals.

- It can act as an investment vehicle, providing tax benefits to beneficiaries and earning dividends that can enhance the policy's overall value.

- It is a valuable estate planning tool, as the death benefit can be used to cover estate taxes or equalize inheritances.

- It is a straightforward type of permanent policy, providing guaranteed returns.

- It can be customized to your financial needs with riders.

Cons

- Whole life insurance is generally more expensive than term life insurance and may not be suitable for everyone due to high premiums.

- It may take a few years for the policy to build significant cash value.

- It is more complex and difficult to understand compared to other types of life insurance.

- It lacks the flexibility offered by other policies, such as Universal life insurance, which allows for changes in premiums and death benefits.

Life Insurance: Irrevocable Beneficiary, Possible?

You may want to see also

Explore related products

![]()

Whole life insurance as a retirement plan

Whole life insurance is a permanent policy that offers lifelong coverage. This means that it will pay out to your loved ones no matter when you pass away. Whole life insurance is designed to last your entire life and will never expire as long as you continue to pay the premiums, which will remain fixed. In addition to a guaranteed death benefit for your beneficiaries, it can help you build cash value, which accrues interest over time.

Whole life insurance can be used as a retirement plan, as it can supplement retirement income. The cash value component of whole life insurance policies earns interest in a tax-advantaged account and offers guaranteed returns. This means that you can withdraw funds or borrow against them to help cover expenses or meet financial goals during retirement. The cash value can also be used to pay for big-ticket items, such as a new home or starting a business.

However, it's important to note that whole life insurance policies are generally expensive and may not be suitable for most people. The low rates of return may not offset the high premiums, and the inherent cost of life insurance within any permanent life insurance policy can become very expensive to maintain. Therefore, it's recommended to weigh the pros and cons of whole life insurance as a retirement plan and consider alternative options, such as investing in a 401(k) or IRA.

If you are already contributing the maximum amount to your 401(k) or IRA, or have significant financial goals for retirement, a Life Insurance Retirement Plan (LIRP) can be a good option. A LIRP can help you save additional money outside of the IRS contribution caps and provide protection for your loved ones in case of any unforeseen events.

Voluntary Life Insurance: Pre-Tax Benefits and Their Value

You may want to see also

Explore related products

![]()

Whole life insurance for high net worth individuals

Whole life insurance is a permanent policy that offers lifelong coverage. This means that it will pay out to your loved ones no matter when you pass away. It is a powerful financial tool for you and your family. Whole life insurance offers a death benefit protection that can keep your family financially secure in case you pass away. It has a guaranteed cash value growth that builds at a steady, dependable pace. That allows it to complement fixed-income investments in your portfolio.

High-net-worth individuals (HNWIs) can benefit from having life insurance despite their substantial assets. Life insurance plays a crucial role in estate planning by providing a tax-free death benefit that can cover estate taxes. It also serves as a financial safety net, offering stability and protecting the long-term financial security of loved ones. It is a necessity for high-net-worth individuals who wish to preserve their estate for future generations. By properly developing an estate plan and utilizing the right type of life insurance, they can ensure the livelihood of their loved ones even when they have passed on.

Whole life insurance can be a good option for high-net-worth individuals as it offers permanent coverage that accumulates a cash value. When you pay your premium, the insurer invests a portion to give your policy a cash value. The cash value grows over time at a fixed rate guaranteed by your insurer. This cash value can be used to help pay for big-ticket items like a new home or launching a business. It can also be used to supplement retirement income.

High-net-worth individuals may also consider term life insurance if they have substantial debts that their dependents would struggle to repay without them. Term life insurance offers coverage for a designated period, typically ranging from 10 to 30 years. If they outlive the term, the policy expires, and no death benefit is paid out unless they renew the term. Additionally, some term policies offer the option to convert to whole life insurance at the end of the term, providing continued coverage as long as it is done by the deadline set by the insurance provider.

Life Insurance: Understanding the Legal Purpose

You may want to see also

Explore related products

![]()

Whole life insurance and tax

Whole life insurance is a permanent policy that offers lifelong coverage. It is a powerful financial tool for individuals and their families. It provides a death benefit payout to beneficiaries and has a secure cash value account that grows over time. This cash value can be used to pay for big-ticket items, such as a new home or starting a business. It can also be used to supplement retirement income.

Whole life insurance is an appropriate option for those seeking lifetime protection and tax-advantaged benefits. The death benefit is typically tax-free, and the cash value component grows tax-deferred. This means that the cash value is not taxed while it is growing, allowing it to grow faster as it is not reduced by taxes each year. The interest earned on the cash value is applied to a higher amount, resulting in greater overall growth.

Additionally, whole life insurance policies can provide tax-free dividends, depending on the company's financial performance. These dividends can be used to purchase additional coverage, increasing the death benefit protection and further enhancing the cash value accumulation. However, it is important to note that dividends are not guaranteed and may vary across different companies.

The proceeds received by beneficiaries due to the death of the insured are generally not considered taxable income. This means that the money left to loved ones is typically untaxed and can be received more quickly than other assets. However, any interest earned on the proceeds is taxable and should be reported accordingly.

While whole life insurance offers tax advantages, it is important to carefully consider your unique tax situation before purchasing a policy. Consulting with a financial professional and a tax advisor is recommended to fully understand the tax implications and ensure that whole life insurance aligns with your financial goals.

Updating Military Life Insurance: Changing Your Beneficiary Details

You may want to see also

Frequently asked questions

Whole life insurance is appropriate for those who want lifelong coverage and can afford the high premiums. It is a good option for parents with lifelong financial dependents, such as a child with a disability, as it provides financial stability and peace of mind. It may also be suitable for high-net-worth individuals who have maxed out their retirement accounts and have a diversified portfolio.

Whole life insurance offers guaranteed returns and lifelong coverage, providing financial security for your loved ones in the event of your death. It also has a cash value component, which accumulates over time and can be used to supplement retirement income or help with big-ticket items like a new home or starting a business.

Whole life insurance is generally more expensive than term life insurance and may take over a decade to earn reasonable investment returns. It is also complex and may not be suitable for those who do not need lifelong coverage or have a limited budget.