Life insurance is a financial safety net for your loved ones after you die. It's a way to ensure your family is taken care of if something happens to you. But when is the best time to get it?

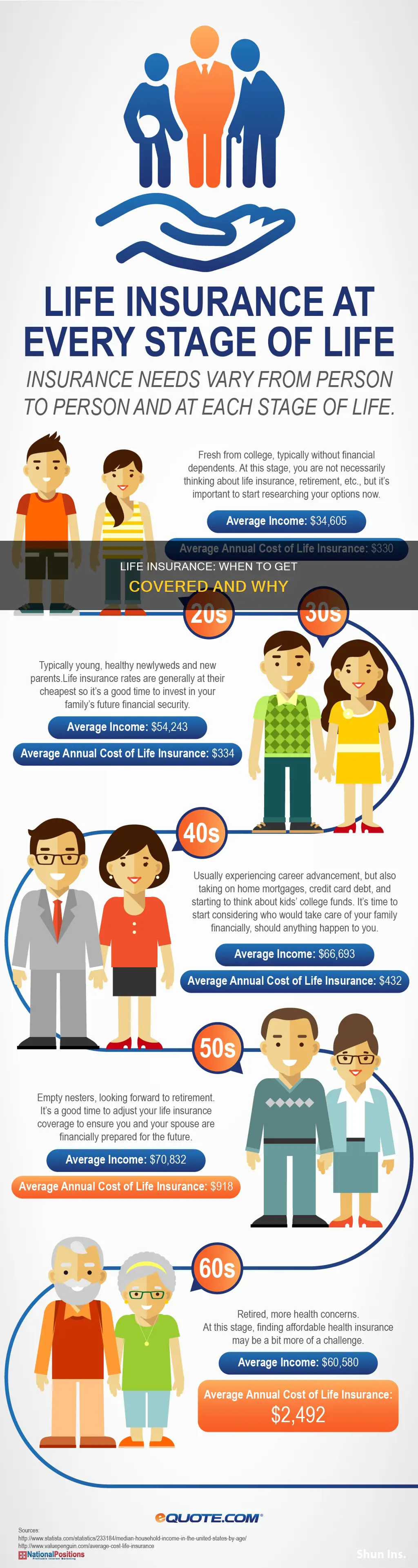

The short answer is: as soon as possible. The younger and healthier you are when purchasing life insurance, the lower your premium will generally be. As we age, we are at a higher risk of developing health conditions, which can result in higher mortality rates and life insurance rates. So, if you're in your 20s or 30s, now is a good time to consider adding life insurance to your financial strategy.

However, the decision to buy life insurance depends on your personal and financial circumstances. If you have people who depend on your income, such as a spouse, children, or ageing parents, then you should strongly consider getting life insurance. It can help protect them financially and ensure they can maintain their standard of living if something happens to you.

Even if you don't have dependents, life insurance can still be beneficial. For example, if you have significant debt, life insurance can ensure that your loved ones won't be burdened with those debts if you pass away. It can also help cover funeral costs, which can be expensive.

So, while there's no one-size-fits-all answer, the bottom line is that life insurance is an important tool to protect your loved ones, and the earlier you get it, the more affordable it will generally be.

| Characteristics | Values |

|---|---|

| Age | Younger people benefit from lower premiums. |

| Dependents | If you have people depending on your income, you should get life insurance. |

| Debt | Life insurance can help pay off your debt after you die. |

| Health | The healthier you are, the lower the cost of a life insurance policy. |

| Marriage | Life insurance can help your spouse pay off debt if you die. |

| Children | Life insurance can help cover the costs of raising children if you die. |

| Retirement | Life insurance can help cover the costs of retirement if you are a dependent. |

| Savings | If you have substantial savings for end-of-life expenses, you may not need life insurance. |

Explore related products

What You'll Learn

![]()

Young and single

Being young and single, you may not think life insurance is necessary. After all, you likely don't have anyone depending on your income, and you may feel you're already burdened with student loan debts and daily expenses. However, there are several reasons why getting life insurance now can be beneficial.

Firstly, life insurance premiums are cheaper when you buy your policy at a younger age. Your age and health are significant factors in determining the cost of life insurance, and the younger and healthier you are, the lower your insurance costs will be. By locking in lower rates now, you can ensure financial protection for your loved ones at a more affordable price.

Secondly, life insurance can help protect those who rely on you financially, even if you don't have a spouse or children. If you have a parent, sibling, or business partner who depends on your income, life insurance can provide for them in the event of your premature death. It can also help cover any debt you may have, including student loans and other liabilities. While federal student loans are typically discharged upon your death, private loans may become the responsibility of a co-signer. Life insurance can ensure that your loved ones aren't burdened with these financial obligations.

Thirdly, life insurance can provide a safety net for your future family and financial goals. Even if you don't plan on having a family or buying a home, things can change. By obtaining life insurance at a young age, you can save money in the long run, as premiums increase with each passing year. Additionally, developing health conditions as you age may make it more difficult and expensive to get coverage later on.

Finally, permanent life insurance policies can serve as a savings vehicle, as they often include a cash value component. This money can grow tax-deferred and be accessed later in life to supplement retirement income, purchase a home, or fund other expenses. The earlier you start, the more time your cash value has to grow.

In summary, while life insurance may not seem like a priority for young and single individuals, there are several compelling reasons to consider it. By purchasing life insurance now, you can secure lower rates, protect your loved ones, cover existing debts, and build savings for the future. Speak with a financial advisor to determine if life insurance is right for you and to navigate the different types of policies available.

LPR Diagnosis: Impact on Life Insurance Rates

You may want to see also

Explore related products

![]()

Newly married

Life insurance is a contract between you and an insurance company designed to provide financial protection for your loved ones if you pass away. Newly married couples often combine their finances, making them financially responsible for significant shared purchases and debts. Therefore, life insurance is essential to ensure that your partner is financially secure in the event of your death.

One partner is the primary earner

Life insurance is crucial if you or your spouse earns the majority of the household income. It can help protect your family financially and allow them to maintain their standard of living if the primary earner passes away. Life insurance can also help your spouse repay any debts, such as a mortgage, car payments, or student loans, and prevent them from feeling overwhelmed by these financial obligations.

You want to manage living expenses

Living expenses, such as a mortgage, utilities, and groceries, can be a burden for a single income. With life insurance, you can help protect your spouse from bearing these costs alone upon your death.

You want to cover final expenses

Life insurance can also alleviate high end-of-life expenses, such as funeral costs and medical bills, for your loved ones.

When deciding on the best life insurance policy for married couples, you can choose between separate life insurance policies or a joint life insurance policy. A separate policy will only cover one spouse, while a joint policy will cover both. Both options have their advantages and disadvantages, so it's important to weigh them carefully before making a decision.

Joint life insurance policies

Also known as dual life insurance, a joint policy covers both spouses. This option is ideal for couples looking to save money on life insurance and protect their assets from taxes after death. There are two types of joint policies: first-to-die and second-to-die. With a first-to-die policy, the surviving spouse receives the death benefit after the first spouse's death. On the other hand, a second-to-die or survivorship policy pays out the death benefit once both spouses have passed away.

Separate life insurance policies

A separate life insurance policy will only cover one spouse and pay out a death benefit to the surviving partner if the insured spouse passes away. You can choose between a term life insurance policy, which provides coverage for a set period, such as 10, 20, or 30 years, or a whole life policy, which offers lifelong protection. Separate policies allow each spouse to focus on their unique needs and tailor the coverage accordingly.

The ideal life insurance policy for married couples depends on their specific needs. If you only need coverage for a set period and want a more favourable premium, term life insurance is a good option. On the other hand, if you prefer the idea of lifelong coverage and a cash value component that may earn interest over time, a permanent policy like whole life insurance may be more suitable.

Life Insurance Sales: Lucrative Career or Waste of Time?

You may want to see also

Explore related products

![]()

Young children

Life Insurance for Young Children

Life insurance for young children is a permanent life insurance policy that provides a fixed death benefit to the beneficiary if the insured child dies while covered. It can also be used as a long-term savings mechanism, as the policy typically includes a cash value component and grows over time.

When to Get Life Insurance for Young Children

You can buy life insurance for a child as soon as they are born, with some insurers offering coverage for newborns. The cutoff age for buying a child life insurance policy varies from insurer to insurer, with some companies offering coverage for children up to the age of 18, while others may have a lower age limit, such as 14 or 17.

Pros of Life Insurance for Young Children

- Guarantees Insurability: You can secure coverage for your child even if they develop a health condition later in life or take up a dangerous hobby or high-risk career as an adult.

- Locks in a Low Rate: You can get a lower rate on life insurance for a child than for an adult, and this rate will be locked in for the duration of the policy.

- Provides Funds for Funeral Expenses: While the chances of a child dying are very low, a life insurance policy can provide funds for funeral costs and allow grieving parents to take time off work.

- Has Cash Value: Whole life insurance policies for children have a cash value component that grows over time, providing a financial cushion for the child's future.

Cons of Life Insurance for Young Children

- Low Rate of Return: Whole life insurance policies for children typically have a low rate of return compared to other investment options, such as a 529 college savings plan.

- Long-Term Commitment: Paying premiums on a whole life insurance policy can be a financial burden over time, especially if cash flow becomes tight.

- Low Coverage Amounts: Coverage amounts for children's life insurance policies tend to be low, typically $50,000 or less, and may not meet the child's needs in adulthood.

- Financial Trade-Off: Buying life insurance for a child may mean giving up money that could be spent on other priorities, such as education or retirement savings.

Alternatives to Life Insurance for Young Children

Before purchasing life insurance for a young child, consider the following alternatives:

- Assess your own life insurance needs: Ensure that you have adequate coverage for yourself and your family before considering a policy for a child.

- Build an emergency fund: Focus on building a solid financial foundation with an emergency fund, retirement savings, and paying off high-interest debt.

- Explore other investment options: Compare the returns on whole life insurance policies with other investment vehicles, such as mutual funds or 529 college savings plans.

Understanding Dividends on Life Insurance Policies

You may want to see also

Explore related products

![]()

Empty nester

As an empty nester, you may be wondering if you still need life insurance. After all, your children are no longer financially dependent on you, and your financial obligations may seem lighter. However, there are several compelling reasons why you should consider maintaining or even enhancing your life insurance coverage. Here are some key considerations for empty nesters:

Providing for Your Spouse

Even if your spouse is financially independent, your death could still impact their financial stability. Your income contributes to your household, and without it, your spouse may have to make significant adjustments to their living arrangements. Additionally, if you are the primary breadwinner, your spouse relies on your financial contributions for retirement savings. A life insurance policy can help offset the loss of income for your spouse, ensuring they can maintain their standard of living.

Supporting Adult Children

Today, it is common for adult children to require financial support beyond the age of 18. Factors such as unsteady job markets, rising education costs, and high housing prices can make it challenging for young adults to achieve complete financial independence. As an empty nester, you may still want to provide financial support to your adult children, especially if they are facing challenges like divorce, career setbacks, or health issues. Life insurance can be a valuable tool to help them through these difficult times and ensure they can complete their education, purchase a home, or overcome financial obstacles.

Meeting Specific Obligations

Even as an empty nester, you may still have financial obligations such as a mortgage, car loans, business loans, or credit card debt. In the event of your death, these obligations could become a significant burden for your loved ones. Life insurance proceeds can be used to pay off these outstanding debts, ensuring your family is not left struggling to make ends meet.

Covering Estate Taxes

If you are single or anticipate outliving your spouse, consider obtaining life insurance to cover estate taxes. This is particularly relevant for individuals with high-value estates, as the liability can be substantial. Life insurance can ensure your heirs or chosen beneficiaries are not burdened with unexpected tax obligations.

Paying Uncovered Medical Expenses

The rising cost of healthcare and the limitations of health insurance coverage can result in significant out-of-pocket medical expenses. In the event of a prolonged illness or unexpected health crisis, these costs can quickly escalate. Life insurance can provide a financial safety net, covering any uncovered medical costs and protecting your loved ones from additional financial strain.

Creating a Financial Safety Net

Life insurance can serve as a financial safety net for your family in the event of your untimely death. It can help cover final expenses, including funeral and burial costs, medical expenses, estate administration fees, and taxes. Additionally, it can provide a source of income for your spouse or dependents, ensuring they have the resources to maintain their standard of living.

In summary, while your life insurance needs may change as an empty nester, it is essential to carefully consider your circumstances before making any decisions. By evaluating your financial situation, ongoing obligations, and the potential needs of your dependents, you can make an informed choice about maintaining or adjusting your life insurance coverage to fit your new life stage.

Life Insurance and Mental Illness: What's Covered?

You may want to see also

Explore related products

![]()

High-debt

If you have a lot of debt, life insurance can be a good idea to ensure that your loved ones are not burdened with it in the event of your passing. While federal student loans are discharged when you pass away, private loans are not. Life insurance can also cover funeral costs, so your family won't have to worry about these expenses.

The younger and healthier you are, the less you will pay for life insurance premiums. Therefore, it is a good idea to lock in lower rates when you are young, even if you are focused on paying off debt. Life insurance can be particularly beneficial for those with high-interest debt, such as credit card debt, as it can be used to pay off these debts without passing them on to loved ones.

There are two main types of life insurance: permanent and term. Term life insurance covers you for a specific period and is generally more affordable for young people, whereas permanent life insurance covers you for your whole life and has a cash value component that grows over time.

If you have a lot of debt, you may opt for a high-value term life insurance policy until the debt is paid down. This can provide a financial safety net for your family at a lower cost. However, it is important to note that term life insurance does not accumulate cash value, so you may want to consider permanent life insurance if you want to build cash value over time.

In summary, if you have high-interest debt or debt that outweighs your assets, life insurance can be a wise decision to protect your loved ones financially. The type of policy and amount of coverage will depend on your individual circumstances, but it is generally more cost-effective to purchase life insurance when you are young and healthy.

Life Insurance: First Group's Offerings and Benefits Explored

You may want to see also

Frequently asked questions

Yes, the best time to buy life insurance is usually as soon as possible. The younger and healthier you are when you purchase a policy, the lower your premium will generally be.

If you have a family or are planning on starting one soon, you should consider a life insurance policy. Life insurance can cover your family’s living expenses and debts if you pass away.

If you pass away before paying off certain debts and you don't have life insurance, your loved ones may end up responsible for those loans. Life insurance can help you not pass on debt to your loved ones.