Life insurance is a way to safeguard your family's financial stability and future. It is a good idea to consider getting life insurance when you are young and healthy, as it can be more affordable and you will be able to avail a larger amount of coverage at a lower price. The cost of life insurance is based on several factors, including age, gender, lifestyle, occupation, medical history, and current health. While it is not required by law in Canada, life insurance can provide peace of mind, knowing that your loved ones will be financially supported in the event of your death. It can help cover expenses such as funeral costs, debts, and mortgage payments, ensuring that your family can maintain their standard of living.

| Characteristics | Values |

|---|---|

| Best age to buy life insurance | There is no best age to buy life insurance, but there are benefits to buying a policy in your 20s and 30s, such as more affordable costs. |

| Who should buy life insurance | People with dependents, such as a spouse and kids, who would be impacted financially by their death. |

| Why buy life insurance | Life insurance can help protect the people you love by providing financial support after you die. It can also help cover mortgage costs, funeral costs, and other expenses. |

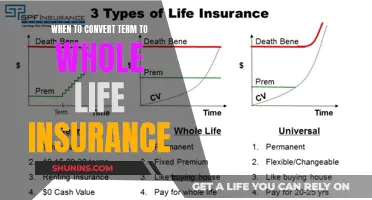

| Types of life insurance | There are two basic types of life insurance: term and permanent. Term life insurance is more affordable and provides coverage for a specific period, while permanent life insurance offers lifetime coverage and usually builds up a cash value. |

| Cost of life insurance | The cost of life insurance depends on age, gender, lifestyle, occupation, medical history, and current health. |

Explore related products

$20.17 $20.17

![Report Of The Royal Commission On Life Insurance [and Supplementary Return]](https://m.media-amazon.com/images/I/51KUkhWivPL._AC_UY218_.jpg)

What You'll Learn

![]()

If you're young and healthy

Secondly, even if you're young and healthy, you may already have some serious financial responsibilities. For example, you may have student loans or credit card debt, or you may be thinking of getting married or starting a family. In any of these situations, it can be helpful to have some coverage in the event of your death, so your loved ones can have financial support and won't be left in a financially challenging situation. Term life insurance can provide temporary coverage and is much more affordable for young people who are just starting out. It can provide a large amount of coverage at a low price and can be renewable every 10, 15, 20, or even 30 years, depending on the policy.

Thirdly, you may already have some life insurance through your workplace benefits, but this type of insurance is usually basic and is often lost when you change jobs. Additionally, if you're carrying a mortgage, life insurance can help your family cover these costs and afford to stay in their home if something happens to you. Plans that offer investment opportunities can also add equity to your estate and give you more options for getting loans or paying down debts later.

Finally, while life insurance is not required by law in Canada, purchasing a life insurance policy is considered good planning. It can give you peace of mind, knowing that if something happens to you, any expenses related to your death will be taken care of, and your loved ones will receive a death benefit – a lump sum of tax-free or tax-deferred money.

Gender's Role in Life Insurance: A Complex Dynamic

You may want to see also

Explore related products

![]()

If you're starting a family

Financial Protection

Life insurance can provide financial stability for your family in the event of your death. It ensures that your family will have the money to maintain their standard of living, cover expenses, and pay off debts. The death benefit from a life insurance policy is typically tax-free, providing a lump-sum payment to your beneficiaries. This can include your spouse, children, or other dependents.

Education Expenses

Life insurance can help cover the cost of your children's education, including college or university tuition, and other related expenses. This ensures that your children will have the financial support they need to pursue their educational goals, even in your absence.

Mortgage and Debt Coverage

Life insurance can help your family pay off the mortgage and any other outstanding debts. It can prevent your loved ones from inheriting your financial burdens and ensure they can maintain their home and stability.

Funeral and Final Expenses

Life insurance can assist with funeral costs and final expenses. This can alleviate the financial strain on your family during an already difficult time, allowing them to focus on grieving and emotional recovery.

Long-Term Financial Planning

Permanent life insurance policies can offer long-term financial benefits, such as accumulating cash value over time. This can be accessed later in life for various purposes, including education expenses, retirement income, or establishing a financial legacy for your children or grandchildren.

When considering life insurance, it's important to work with an advisor who can help you navigate the different types of insurance, such as term and permanent, and create a plan that fits your family's budget and needs. It's also essential to review and adjust your policy periodically, especially after significant life events like the birth of a child.

By investing in life insurance, you can gain peace of mind knowing that your family will be financially secure, even in your absence. It's a thoughtful and responsible step towards protecting your loved ones and ensuring their well-being.

Writing Off Life Insurance: Corporate Strategies and Benefits

You may want to see also

Explore related products

$8

$9.67 $12.99

![]()

If you have a pre-existing medical condition

First, it's important to understand what is considered a pre-existing condition. A pre-existing condition is any medical condition for which you have symptoms or have been diagnosed prior to applying for life insurance. Common pre-existing conditions include diabetes, asthma, high blood pressure, and heart disease.

When applying for life insurance with a pre-existing condition, you may be offered a "rated" policy. This means that your policy may carry a higher premium, and you will likely need to undergo medical tests, such as blood or urine tests, to ensure that you don't have any other conditions. The specific tests and questions will depend on the insurance company and the type of policy you are applying for.

There are several types of life insurance policies available in Canada that may be suitable for individuals with pre-existing conditions. These include:

- Simplified issue life insurance: This type of policy requires applicants to answer limited medical questions to determine eligibility, but no physical examination is required. Simplified issue life insurance typically offers more maximum coverage and lower premiums than guaranteed issue life insurance, making it a good option for those with less severe medical conditions.

- Guaranteed issue life insurance: This type of policy does not require any medical questions or examinations, and your acceptance is guaranteed. However, these policies tend to be more expensive and offer lower death benefits, typically around $25,000 to $50,000.

- Term life insurance: This type of policy covers you for a specified term, usually 10, 20, or 30 years. Term life insurance may be attainable if your condition is not expected to affect your health within the term. Term life premiums will likely be higher if you have a pre-existing condition.

It's important to be truthful and upfront about your pre-existing conditions when applying for life insurance. Failing to disclose a pre-existing condition could result in your claim being denied. Additionally, different insurance companies have different standards for acceptable health conditions, so it may be helpful to make an informal inquiry before applying to find a company that is more likely to accept you.

Getting a Life Insurance License: How Long Does It Take?

You may want to see also

Explore related products

![]()

If you're a homeowner

Mortgage life insurance is group insurance that can be convenient to get when arranging your mortgage. It may be easier to qualify for coverage than with personal life insurance, and it features a simple application process. It is marketed towards new homeowners who may worry that an unexpected death or illness could leave their loved ones with a large mortgage. This type of insurance can free up money from other insurance policies and help your family stay in their home by ensuring that the insurance money payable is applied to the mortgage balance.

Personal life insurance, on the other hand, can more easily handle new financial realities as your family's financial situation changes. There are two main types: term life insurance and permanent life insurance. Term life insurance provides a tax-free payout to your chosen beneficiaries if you die within the term you choose. The payments, or premiums, remain the same for the term you select and won't change during that period. Permanent life insurance offers lifelong coverage and protection for your loved ones. Over time, your policy can accumulate value that you can access for cash during your life.

The amount of life insurance you need depends on your situation, including factors such as whether you're married or single, have children, or own a home. It's recommended to start with coverage equivalent to five times your income. An advisor can help you determine the right amount and type of insurance for your specific needs.

Primerica Life Insurance: Payout Process and Benefits Explained

You may want to see also

Explore related products

$13.1 $19.99

![]()

If you're starting a business

Starting a business is a significant life event that warrants a review of your life insurance coverage. Here are some key considerations if you're starting a business and thinking about life insurance in Canada:

Types of Life Insurance

In Canada, there are two basic types of life insurance: term and permanent. Term life insurance is generally more affordable, especially when you're younger, as it provides coverage for a specific period and doesn't accumulate cash value. Permanent life insurance offers lifelong coverage and often includes an investment component, allowing you to build wealth for your beneficiaries. While permanent insurance provides more comprehensive protection, it tends to be more expensive, especially as you get older.

Business Protection

Life insurance can provide financial protection for your business. If you have business partners, life insurance ensures that the surviving partners have the funds to continue running the company. It can also help cover any business loans or debts you may have incurred when starting the business. This ensures that your business can continue operating even in your absence.

Beneficiary Considerations

When purchasing life insurance, you can designate a beneficiary who will receive the death benefit. In the context of your business, you may choose to name a business partner, a trust, or even a charitable organization as your beneficiary. This allows you to provide financial support to causes or entities that are important to you.

Financial Planning

Starting a business often involves taking on financial risks and obligations. Life insurance can provide peace of mind by ensuring that your business and personal finances are protected. It can help cover expenses, debts, or loans associated with your business, ensuring that your business ventures do not burden your loved ones financially.

Health and Age Considerations

The cost of life insurance is influenced by your age and health. Generally, the younger and healthier you are, the lower your premiums will be. If you're starting a business at a young age, it may be advantageous to purchase life insurance early, as it can provide you with more affordable coverage options.

In summary, if you're starting a business in Canada, life insurance can be a valuable tool to protect your business and personal finances. It's important to consider the different types of insurance, choose appropriate beneficiaries, and factor in your age and health to make informed decisions about the level of coverage you need. Consulting with a financial advisor or insurance specialist can help you tailor a plan that suits your specific circumstances.

Life Insurance: Buying the Right Coverage for Peace of Mind

You may want to see also

Frequently asked questions

Life insurance in your 20s can help you protect your financial future. It is usually more affordable to purchase a plan when you’re young and healthy rather than waiting until later when you may have developed health issues.

By your 30s, you may have more financial responsibilities, such as a mortgage, marriage, or children. Life insurance can help cover these expenses in the event of your death.

There are two basic types of life insurance in Canada: term life insurance and permanent life insurance. Term life insurance is generally less expensive but does not include cash value, while permanent life insurance offers lifelong protection and can be used to build wealth for your beneficiaries.