Life insurance proceeds are generally not taxable as income, but there are certain situations in which taxes are assessed. For example, if you cancel your policy and withdraw the cash value, or sell your policy in a life insurance settlement, you may be subject to capital gains or income taxes. If you decide to make a withdrawal from a universal life insurance policy, the IRS will only tax the portion that exceeds your cost basis (the total amount of premiums you've paid into the policy). If you receive the proceeds in installments, any interest that accumulates on those payments will be taxed as regular income. If you want to avoid federal taxation, you can transfer ownership of your policy to another person or entity, or set up an irrevocable life insurance trust (ILIT).

| Characteristics | Values |

|---|---|

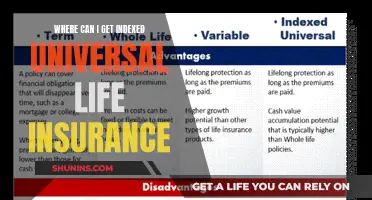

| Are life insurance proceeds taxable? | Life insurance proceeds are typically not taxable as income. |

| When are life insurance proceeds taxable? | Life insurance proceeds can be taxed as part of your estate if the amount being passed to your heirs exceeds federal and state exemptions. |

| How to avoid federal taxation? | Transfer ownership of your policy to another person or entity. |

| How to avoid life insurance payouts being taxed as part of your estate? | Set up an irrevocable life insurance trust (ILIT). |

| When are life insurance dividends taxable? | Life insurance dividends are not taxable unless they exceed the amount you paid in premiums over the course of the year. |

| When are life insurance proceeds not taxable? | Life insurance death proceeds are not taxable with respect to income tax as long as the proceeds are paid out entirely as a lump-sum, one-time payment. |

| When are life insurance proceeds taxable to the beneficiary? | If the beneficiary receives the life insurance payment as a series of installments, the insurer will typically pay interest on the outstanding death benefit. |

| When are life insurance proceeds taxable when surrendered? | If you surrender the policy and your surrender proceeds exceed the cumulative premiums, the excess may be subject to income taxes. |

| When are life insurance proceeds taxable when sold? | If the sales proceeds exceed your cumulative premiums, minus the portion of your premiums attributed to the cost of insurance, the excess may be subject to income taxes. |

Explore related products

What You'll Learn

![]()

Proceeds as income tax

Life insurance proceeds are typically not taxable as income. However, there are certain situations in which the beneficiary may be taxed on some or all of a policy's proceeds.

If the beneficiary of a life insurance policy is a spouse, the life insurance payout is not taxed and will be passed on to them in full. This is because spouses typically have an unlimited exemption with regards to estate taxes. However, if the beneficiary is not a spouse, the life insurance payout will be added to the value of the estate, and taxes may be due.

If the policyholder elects to delay the benefit payout and the money is held by the life insurance company for a given period, the beneficiary may have to pay taxes on the interest generated during that time. This is because any interest earned on the proceeds is taxable and should be reported. This also applies if the beneficiary receives the life insurance proceeds in installments; they must pay taxes on the interest, even though the original death benefit is not taxable.

If the policy is a modified endowment contract (MEC), the tax treatment is different. In this case, all withdrawals are treated as taxable income until they equal the total interest earned on the contract.

To avoid paying taxes on life insurance proceeds, a taxpayer can transfer ownership of the policy to another person or entity. However, it is important to note that if the policy was transferred for cash or other valuable consideration, the exclusion for proceeds is limited to the sum of the consideration paid, additional premiums paid, and certain other amounts.

Assured Life Insurance: What You Need to Know

You may want to see also

Explore related products

![]()

Estate and inheritance tax

Life insurance proceeds are generally not taxable as income. However, there are certain circumstances where the beneficiary may be taxed on some or all of a policy's proceeds.

Life insurance proceeds can be taxed as part of your estate if the amount being passed to your heirs exceeds federal and state exemptions. In the US, the value of an estate that exceeds $12.06 million per individual will be subject to a tax rate of up to 40%. There are 17 states, plus Washington, D.C., with an inheritance or estate tax. The estate tax exemption amount varies by state but ranges from $1 million to $7 million, with tax rates as high as 20%.

To prevent estate tax on life insurance proceeds, the insured must avoid two things:

- Payment to the insured's estate

- "Incidents of ownership"

One way to avoid this is to have another person or entity apply for and purchase a new policy on the insured's life. Another method is to transfer all "incidents of ownership" in an existing policy to another person or entity.

If the beneficiary is anyone besides the spouse, such as a child or parent, the life insurance payout will typically be added to the value of the estate. This is fine if the total value of the estate is less than the federal and state exemptions. However, if the total value exceeds the exemption, any amount over it is subject to estate and inheritance taxes.

It is important to note that careful estate planning can ensure that life insurance provides liquidity or replaces the value used to pay the estate tax, thereby reducing the burden on the beneficiaries.

Borrowing Money from Supplemental Life Insurance: Is It Possible?

You may want to see also

Explore related products

![[OLD VERSION] TurboTax Deluxe 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71UbHaUeeUL._AC_UL320_.jpg)

![]()

Beneficiary receives proceeds

When you purchase a life insurance policy, you can designate a beneficiary to receive the proceeds upon your death. The person you choose as a beneficiary will receive the full funds from your policy. You can name a single beneficiary, or you can name both a primary beneficiary and one or more contingent beneficiaries. A primary beneficiary is the person who is first in line to receive the proceeds from your life insurance policy upon your death. A contingent beneficiary is the person who is second in line to receive the proceeds in the event that the primary beneficiary has passed away.

If you name more than one primary beneficiary and one of them dies, the remaining beneficiaries would be entitled to the death benefit. Typically, they would each receive the same amount of money, but you can request a different type of distribution if you prefer. If your contingent beneficiary passes away, and your primary beneficiary is also deceased, any remaining beneficiaries will receive the payout. If there are no remaining beneficiaries, the death benefit would be paid into your estate.

In most cases, life insurance proceeds are not taxable. However, any interest earned is taxable and should be reported. If the policyholder elects to delay the benefit payout and the money is held by the life insurance company for a given period of time, the beneficiary may have to pay taxes on the interest generated during that period. When a death benefit is paid to an estate, the person or persons inheriting the estate may have to pay estate taxes.

Finding Life Insurance Beneficiaries: A Comprehensive Guide

You may want to see also

Explore related products

![H&R Block Tax Software Deluxe + State 2024 with Refund Bonus Offer (Amazon Exclusive) Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51+fonAXhPL._AC_UL320_.jpg)

![[OLD VERSION] TurboTax Home & Business 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71b5aAzdXOL._AC_UL320_.jpg)

![]()

Surrendering or selling a policy

If you surrender or sell a life insurance policy, you may have taxable income to report. The amount you receive from the insurance company when you surrender or sell a policy is called the "cash surrender value." This is the cash amount that the insurance company has set aside to fund the policy's benefits. When you surrender or sell the policy, you may receive more or less than the cash surrender value, depending on the terms of your policy and any outstanding loans or withdrawals you've made against the policy.

Any amount you receive that is more than the total of the premiums you paid into the policy (known as your "basis" in the policy) is generally taxable as ordinary income. However, there are a few exceptions. If you paid premiums for a policy that was supposed to last your entire life, and the policy ends because of the insured person's death, you don't have to report any of the proceeds as income. Similarly, if you have a policy that is considered a "modified endowment contract," and it ends because of the insured person's death, you don't have to report any of the proceeds as income.

On the other hand, if you sell your life insurance policy through a life settlement, the amount you receive may be taxable. A life settlement is the sale of your life insurance policy to a third party for more than your cash surrender value but less than the death benefit amount. The amount you receive from a life settlement that is more than your basis in the policy (the total premiums you paid) is generally taxable. However, if the insured person is terminally ill and meets certain other requirements, some or all of the gain from the life settlement may be excluded from income.

It's important to keep track of all the premiums you pay into a life insurance policy, as well as any other amounts you add to the policy, such as through policy dividends or interest. These amounts increase your basis in the policy and reduce the amount of any taxable gain when you surrender or sell the policy. Additionally, if you've taken out any loans or made any withdrawals against the policy, these amounts generally reduce your basis and increase the amount of any taxable gain.

Life Insurance: Exploring Healthshare-like Programs

You may want to see also

Explore related products

![[OLD VERSION] TurboTax Premier 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71yj6wGqynL._AC_UL320_.jpg)

$114.99

![H&R Block Tax Software Premium 2024 Win/Mac with Refund Bonus Offer (Amazon Exclusive) [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51tob7UDgCL._AC_UL320_.jpg)

![]()

Avoiding federal taxation

Life insurance death benefits are typically tax-free, but there are some situations in which taxes are assessed. Life insurance proceeds are usually not taxable as income, but can be taxed as part of your estate if the amount being passed to your heirs exceeds federal and state exemptions.

If you want your life insurance proceeds to avoid federal taxation, you'll need to transfer ownership of your policy to another person or entity. Here are some guidelines to remember when considering an ownership transfer: Choose a competent adult/entity to be the new owner (it may be the policy beneficiary), then call your insurance company for the proper assignment or transfer of ownership forms. New owners must pay the premiums on the policy. However, you can gift up to $16,000 per person in 2022 and $17,000 in 2023, so the recipient could use some of this gift to pay premiums. You will give up all rights to make changes to this policy in the future. However, if a child, family member, or friend is named the new owner, changes can be made by the new owner at your request. Because ownership transfer is an irrevocable event, be cautious of divorce situations when planning to name the new owner.

Another way to avoid life insurance payouts being taxed as part of your estate is to set up an irrevocable life insurance trust (ILIT). You transfer ownership of the policy to the ILIT and cannot be the trustee. However, you can determine who you want as the trust beneficiary. While an ILIT is an effective way to make sure that your life insurance death benefit is not taxable as part of your estate, there are a couple of situations in which you may face a tax event: When setting up the trust, if the life insurance policy’s cash value is greater than the gift tax exemption, you may need to pay a gift tax when transferring ownership.

The IRS has developed rules that help to determine who owns a life insurance policy when an insured person dies. The primary regulation overseeing proper ownership is known as the three-year rule, which states that any gifts of life insurance policies made within three years of death are still subject to federal estate tax. This applies to both a transfer of ownership to another individual and the establishment of an ILIT. So, if you die within three years of the transfer, the full amount of the proceeds is included in your estate as though you still owned the policy. The IRS will also look for any incidents of ownership by the person who transfers the policy. In transferring the policy, the original owner must forfeit any legal rights to change beneficiaries, borrow against the policy, surrender or cancel the policy, or select beneficiary payment options.

Life Insurance Blood Tests: HIV Testing Included?

You may want to see also

Frequently asked questions

Life insurance proceeds are typically not taxable as income, but can be taxed as part of your estate if the amount being passed on exceeds federal and state exemptions.

You can set up an irrevocable life insurance trust (ILIT) and transfer ownership of the policy to the trust. You can then designate a beneficiary of your choice.

The federal estate tax exemption was $13.61 million as of 2024. This number can vary from year to year.

Yes, you may be subject to capital gains or income taxes if you cancel your policy and withdraw the cash value or surrender it to your insurer.

Yes, any interest accrued by the annuity account is subject to taxes.

![[OLD VERSION] TurboTax Business 2024 Tax Software, Federal Tax Return [PC Download]](https://m.media-amazon.com/images/I/71NKT0cDwnL._AC_UL320_.jpg)

![[Old Version] TurboTax Deluxe 2023, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/719rCYQpjdL._AC_UL320_.jpg)

![H&R Block Tax Software Premium & Business 2024 Win with Refund Bonus Offer (Amazon Exclusive) [PC Online code]](https://m.media-amazon.com/images/I/51yZ-hIg8vL._AC_UL320_.jpg)