Life insurance is a financial tool that helps protect your loved ones and their future by providing financial security. It involves a careful evaluation of your financial situation to determine the right amount of coverage, and it's important to consider factors like income replacement and outstanding debts. Life insurance can also assist with estate planning and ensure business continuity. When choosing a policy, it's crucial to compare quotes from multiple insurers and consider policy features beyond the death benefit, such as riders and premium flexibility. The application process typically includes a medical exam to assess health. Life insurance plays a significant role in safeguarding the financial well-being of those you care about.

Explore related products

What You'll Learn

- Life insurance calculators and financial advisors can help estimate the right amount of coverage

- Policy features like riders, death benefits, and premium flexibility should be considered

- Income replacement and outstanding debts are factors in determining coverage needs

- Online quote tools help compare premiums, coverage options, and policy features

- Medical exams are often required to assess health as part of the application process

![]()

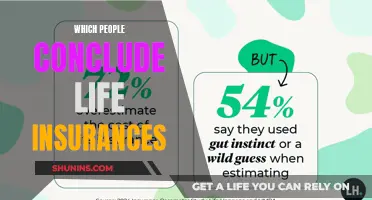

Life insurance calculators and financial advisors can help estimate the right amount of coverage

Life insurance is a crucial tool for protecting your loved ones and securing their financial future. It can be challenging to determine the right amount of coverage, as it depends on various factors, including your income, financial obligations, debts, and future expenses. This is where life insurance calculators and financial advisors can be incredibly valuable.

Life insurance calculators are easily accessible online and can provide a quick estimate of your insurance needs. These calculators take into account multiple factors, such as your annual income, the number of dependents, debt, future college costs, funeral expenses, savings, and any existing life insurance coverage. By entering these details, you can instantly get an estimate of the coverage amount that may be appropriate for your situation.

While online calculators are convenient, they may not capture the full complexity of your financial situation and goals. This is where financial advisors come in. Licensed financial advisors or agents can offer tailored advice and help you assess your unique needs and goals. They can guide you in determining the right type and level of coverage, taking into account your specific circumstances. Financial advisors can also assist in comparing policies from multiple insurers, ensuring you find the best coverage for your budget.

It is recommended to use a combination of these approaches. First, use a life insurance calculator to get a preliminary estimate. Then, consult a financial advisor to fine-tune that estimate and ensure it aligns with your financial goals and circumstances. By doing so, you can feel confident that you have the right amount of coverage to protect your loved ones.

Additionally, when deciding on the appropriate coverage, it is essential to evaluate your financial situation and determine how much coverage you need. Consider factors such as income replacement, where your family would need a certain amount of money to maintain their standard of living, and include any outstanding debts like mortgages, loans, or credit card balances that your family would need to pay off.

Combining Careers: Life Insurance Agent and Real Estate Pro

You may want to see also

Explore related products

![]()

Policy features like riders, death benefits, and premium flexibility should be considered

Life insurance is a financial tool that safeguards your loved ones and their future. It is a crucial decision that impacts the people you care about, so it's essential to choose a policy that meets their current and future requirements. When considering life insurance, it's important to evaluate your financial situation and determine the level of coverage you need. This includes factors such as income replacement and debts.

While riders offer additional benefits, they typically come at an extra cost, and it's important to understand the terms before purchasing. Riders can be added later in some cases, but this may be more complicated and expensive due to age and health changes. It is recommended to discuss these options with a financial advisor to evaluate the costs and benefits based on your specific situation.

Death benefits are another crucial aspect of life insurance. While the primary purpose of life insurance is to provide financial support after your death, some policies now offer living benefits, providing financial security and flexibility while you're still alive. This makes life insurance a valuable tool for financial planning and enhancing your peace of mind.

Finally, premium flexibility is an important consideration. Life insurance policies may offer different options for paying premiums, including the frequency and amount. Some riders, like the Paid-Up Addition Rider, allow policyholders to use dividends to buy extra portions of fully paid life insurance, increasing the cash value and death benefits of the policy. This provides immediate and long-term financial security without additional out-of-pocket expenses.

In conclusion, when considering life insurance, it is essential to evaluate the policy features, including riders, death benefits, and premium flexibility. These options ensure that your chosen policy aligns with your financial goals and provides comprehensive protection for your loved ones. By understanding these features, you can make a well-informed decision that meets both their current and future needs.

How to Cash Out Whole Life Insurance Policies?

You may want to see also

Explore related products

![]()

Income replacement and outstanding debts are factors in determining coverage needs

Life insurance is a crucial tool for protecting your loved ones and securing their financial future. It can be challenging to determine how much life insurance you need, but the primary goal is to ensure your loved ones can maintain their lifestyle, cover any debts, and meet future financial goals without your economic contribution.

Income replacement and outstanding debts are key factors in determining the coverage you need. When considering income replacement, you should calculate how much money your family would require to maintain their standard of living in your absence. A common guideline is to aim for 60% to 80% of your individual post-tax income, but this can vary depending on your specific circumstances. For example, if you are the sole breadwinner, you may need a higher level of coverage to replace your income entirely. On the other hand, if your spouse also works, a lower coverage amount may be sufficient.

Outstanding debts, such as mortgages, car loans, student loans, and credit card balances, are another critical factor in determining your life insurance needs. The insurance coverage should ideally provide enough funds to pay off these debts, ensuring that your loved ones are not burdened by them. For example, if you have a significant mortgage debt, your life insurance coverage should aim to include this amount to relieve your family of this financial obligation.

Additionally, it is essential to consider future expenses and financial goals when determining your life insurance coverage. This includes estimating the cost of children's education, future medical expenses, and retirement savings. By using an online calculator or consulting a financial advisor, you can estimate the right amount of coverage tailored to your specific needs and goals.

Furthermore, it is worth noting that your life insurance needs may change over time. As you age and accumulate more savings, your life insurance need may decrease. Therefore, it is advisable to periodically review and adjust your coverage to ensure it aligns with your changing circumstances and goals.

Life Insurance and Tax: What's the Code?

You may want to see also

Explore related products

![]()

Online quote tools help compare premiums, coverage options, and policy features

Life insurance is a crucial tool for protecting your loved ones and securing their financial future. It can be a complex process with long-term financial implications, so it's important to make an informed decision that aligns with your financial goals and provides lasting protection for those you care about.

Online quote tools are an excellent resource for comparing life insurance premiums, coverage options, and policy features. These tools allow you to quickly and efficiently evaluate multiple options simultaneously, saving you time and money compared to contacting insurance agents individually. By using online quote tools, you can gain a comprehensive understanding of the market and make a more informed decision.

When using these tools, you will typically be required to provide personal details such as your age, weight, height, smoking habits, home address, income, marital status, and occupation. This information is essential for insurers to assess your health and estimate your life expectancy, which are critical factors in determining your premium.

Online quote tools offer a convenient and accessible way to compare life insurance policies. They enable you to explore the range of options available, including term life insurance, whole life insurance, universal life insurance, and final expense insurance, each with its unique features and benefits. By using these tools, you can make a well-informed decision that aligns with your financial situation and goals.

While online quote tools are incredibly helpful, it's important to remember that they may not cover every insurer in the market. Additionally, for more complex financial planning needs or specific health considerations, consulting an independent agent or a trusted financial advisor can provide a more tailored assessment and guidance in navigating the various policy options and coverage types.

Life Insurance: Impact on Net Worth Calculation

You may want to see also

Explore related products

![]()

Medical exams are often required to assess health as part of the application process

Life insurance is a crucial tool for protecting your loved ones and securing their financial future. It can be a major financial decision that impacts the people you care about, so it is important to choose a policy that meets their current and future needs. When considering life insurance, it is essential to evaluate your financial situation and determine the level of coverage you require. This includes assessing your income, debts, and liabilities to ensure that your family can maintain their standard of living and manage any outstanding financial obligations in your absence.

Medical exams are often required as part of the application process for traditional life insurance policies. These exams serve to assess an individual's health and determine their eligibility for coverage. The specific requirements and procedures included in the medical exam can vary, but they typically involve a comprehensive evaluation of an individual's physical health and medical history. This may include measurements of height, weight, and body mass index (BMI), as well as blood pressure readings and laboratory tests, such as blood and urine analyses.

The medical exam helps insurance providers evaluate the applicant's overall health and identify any potential risks or pre-existing conditions. By reviewing an applicant's medical history and current health status, insurers can make informed decisions about the level of coverage they can offer and the associated premiums. This process allows them to assess the likelihood of future claims and adjust the terms of the policy accordingly.

While the medical exam is a standard component of the life insurance application process, it is important to note that not all insurers have the same requirements. Some companies may offer alternative options, such as simplified issue or guaranteed issue life insurance policies, which do not require a medical exam for approval. These policies typically have lower coverage amounts and may be more expensive, but they can be a viable solution for individuals who are unable or unwilling to undergo a medical evaluation.

Additionally, the weightage given to the medical exam may vary depending on other factors considered during the application process. For example, insurers often review an applicant's lifestyle choices, such as smoking status, occupation, and participation in risky activities. They may also take into account family medical history and existing health conditions. By considering these additional factors, insurance providers can gain a more comprehensive understanding of the applicant's overall health and make more informed underwriting decisions.

Borrowing Against Universal Life Insurance: Is It Possible?

You may want to see also

Frequently asked questions

Life insurance is a crucial tool for protecting your loved ones and securing their financial future.

It is critical to choose a policy that meets the current and future needs of your loved ones. Some factors to consider are income replacement, debts and liabilities, and additional features like riders.

You can use an online life insurance calculator or consult a licensed financial advisor to estimate the right amount of coverage based on your needs.

The life insurance application process typically involves a medical exam to assess your health. After the medical exam, you can apply for the policy.

In a joint life insurance policy, the surviving insured may have the option to continue the existing joint policy or buy an individual policy after providing evidence of insurability.