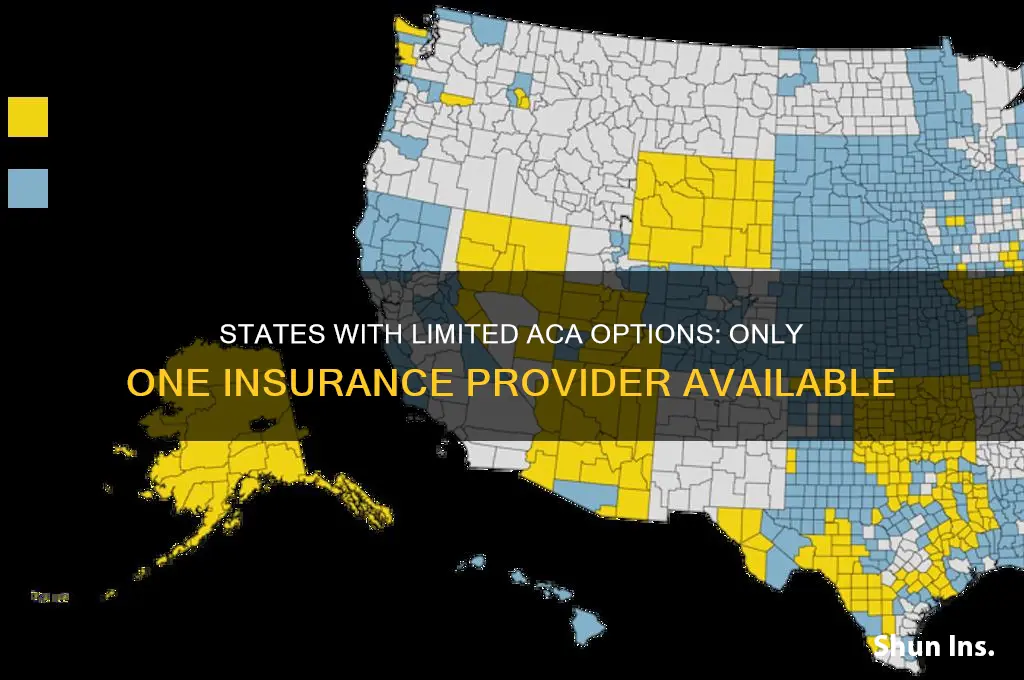

The Affordable Care Act (ACA), also known as Obamacare, has significantly reshaped the health insurance landscape in the United States, but disparities in market competition persist across states. Notably, some states have only one insurance company offering plans on their ACA marketplaces, limiting consumer choice and potentially affecting premiums and coverage options. This lack of competition often stems from factors such as smaller populations, higher provider costs, or insurer reluctance to enter less profitable markets. Understanding which states face this challenge is crucial for policymakers and consumers alike, as it highlights areas where additional support or incentives may be needed to attract more insurers and ensure robust, competitive marketplaces.

| Characteristics | Values |

|---|---|

| States with One Insurer | As of the latest data (2023), no states have only one insurer on the ACA. |

| Closest Scenario | Some rural counties in states like Wyoming, Nebraska, and Mississippi have limited options, often with only one or two insurers. |

| Reason for Limited Options | Insurers may avoid areas with low population density or high-risk pools due to financial viability concerns. |

| Federal Efforts | The ACA includes subsidies and risk-adjustment programs to encourage insurer participation in underserved areas. |

| State Efforts | Some states offer reinsurance programs to stabilize markets and attract more insurers. |

| Impact on Consumers | Limited choices may result in higher premiums and fewer plan options for residents. |

| Trend | Competition has improved in recent years, reducing the number of single-insurer counties. |

Explore related products

What You'll Learn

- States with Limited ACA Options: Identify states where only one insurer offers ACA plans

- Monopoly in Health Insurance: Explore reasons for single-insurer dominance in certain states

- Impact on Premiums: Analyze how limited competition affects ACA plan costs in these states

- Consumer Choice Constraints: Discuss challenges for consumers with only one insurer option

- Policy and Regulatory Factors: Examine state and federal policies contributing to single-insurer markets

![]()

States with Limited ACA Options: Identify states where only one insurer offers ACA plans

In the landscape of the Affordable Care Act (ACA), some states face a unique challenge: they have only one insurer offering plans on their marketplaces. This limitation can significantly impact consumer choice, premium costs, and access to care. As of recent data, states like Wyoming, Alaska, and Alabama are prime examples where residents have just one insurer to choose from. This lack of competition often leads to higher premiums and fewer plan options, leaving consumers with little flexibility in selecting coverage that meets their needs.

Analyzing the reasons behind this phenomenon reveals a complex interplay of factors. Rural states, such as Wyoming, often struggle to attract multiple insurers due to smaller population sizes and higher healthcare costs per capita. Insurers may find it financially unviable to operate in these markets, leading to monopolistic conditions. In contrast, urbanized states with larger populations typically enjoy more competition, driving down costs and expanding consumer options. Policymakers in single-insurer states must address these structural issues to encourage market entry and improve access to affordable care.

For consumers in these states, navigating the ACA marketplace requires strategic planning. First, review the available plan thoroughly, focusing on coverage details, provider networks, and out-of-pocket costs. Second, consider off-exchange plans, which may offer additional options but often lack premium tax credits. Third, explore Medicaid eligibility if income qualifies, as it provides a viable alternative to ACA plans. Lastly, advocate for policy changes at the state and federal levels to incentivize insurer participation and increase competition.

Comparatively, states with multiple insurers benefit from lower premiums and more tailored plan options. For instance, California and New York have robust marketplaces with numerous insurers competing for customers, resulting in lower average premiums. This contrast highlights the importance of market competition in driving affordability and accessibility. Single-insurer states can learn from these models by implementing policies that reduce barriers to entry for insurers, such as reinsurance programs or state-based subsidies.

In conclusion, states with only one ACA insurer face significant challenges that affect both consumers and policymakers. By understanding the underlying causes and adopting targeted strategies, these states can work toward expanding insurer participation and improving healthcare access. For residents, proactive steps in evaluating available options and advocating for change can mitigate the impact of limited choices. Addressing this issue is crucial for achieving the ACA’s goal of providing affordable, comprehensive coverage to all Americans.

Denied PIP Insurance? What to Do After a Medical Exam

You may want to see also

Explore related products

![]()

Monopoly in Health Insurance: Explore reasons for single-insurer dominance in certain states

In the Affordable Care Act (ACA) marketplace, several states have only one insurance company offering plans, creating a de facto monopoly. This concentration of power raises questions about consumer choice, pricing, and the overall health of the insurance market. Wyoming, Alabama, and Alaska are notable examples where residents face limited options, often leaving them at the mercy of a single insurer’s rates and coverage terms. Such monopolies are not merely coincidental but stem from a complex interplay of economic, regulatory, and geographic factors.

One primary reason for single-insurer dominance is the high cost of market entry and operation in sparsely populated or rural states. Insurers must balance the expense of provider networks, administrative overhead, and regulatory compliance against the potential revenue from a limited customer base. In Wyoming, for instance, the small population of approximately 580,000 makes it financially risky for multiple insurers to compete. Without sufficient volume, companies may incur losses, leading to market exits and leaving only the most established or risk-tolerant insurer remaining.

Regulatory environments also play a critical role in shaping insurer participation. States with stringent regulations or unpredictable policy changes can deter competition. Alabama, for example, has historically faced challenges in attracting insurers due to its regulatory framework and the financial instability of its ACA marketplace. Conversely, states with more flexible regulations or incentives for insurers may see greater participation. However, even in these cases, the allure of larger, more profitable markets often draws insurers away from smaller states, leaving a single company to fill the void.

Geographic and demographic factors further exacerbate the issue. Rural states like Alaska face unique challenges, including vast distances between populations and higher healthcare delivery costs. These conditions make it difficult for insurers to negotiate competitive provider contracts or manage care efficiently. Additionally, older or less healthy populations in these states can increase claims costs, discouraging insurers from entering or remaining in the market. The result is a monopoly that, while unintended, becomes a practical necessity for ensuring residents have *some* access to health insurance.

Addressing single-insurer dominance requires targeted interventions. Policicians could explore subsidies or risk-sharing mechanisms to incentivize insurer participation in underserved states. For example, reinsurance programs, which protect insurers from high-cost claims, have successfully attracted more insurers to states like Wisconsin and Oregon. Consumers in monopoly states should also be proactive, advocating for policy changes and exploring alternative coverage options, such as employer-sponsored plans or Medicaid, where eligible. While monopolies in health insurance are far from ideal, understanding their root causes is the first step toward fostering a more competitive and equitable marketplace.

Health Insurance and Medicaid: Understanding the Interplay

You may want to see also

Explore related products

![]()

Impact on Premiums: Analyze how limited competition affects ACA plan costs in these states

In states where only one insurer offers Affordable Care Act (ACA) plans, premiums often soar due to the absence of competitive pressure. Without rivals to undercut prices or innovate, the sole insurer can set rates with minimal restraint. For instance, in 2023, Wyoming and West Virginia saw average premiums exceed $800 per month for a 40-year-old nonsmoker, compared to the national average of $456. This disparity highlights how monopolistic markets can inflate costs, leaving consumers with fewer affordable options.

To understand the mechanics, consider the role of competition in pricing. In competitive markets, insurers vie for customers by lowering premiums or enhancing benefits. In contrast, a single insurer faces no such incentive, often leading to higher administrative costs and profit margins being passed to consumers. A 2021 study by the Kaiser Family Foundation found that counties with one insurer had premiums 5-10% higher than those with multiple carriers. This trend underscores the direct correlation between limited competition and elevated ACA plan costs.

However, the impact isn’t solely financial; it also affects plan quality and consumer choice. With no competition, insurers may offer fewer plan variations or skimp on provider networks, forcing enrollees into narrow or inadequate coverage. For example, in Alabama’s sole-insurer counties, 40% of plans had networks rated "poor" by the Commonwealth Fund, compared to 15% in competitive markets. This trade-off between cost and quality further exacerbates the challenges faced by residents in these states.

Policymakers and consumers alike must address this issue through targeted interventions. Expanding insurer participation, offering incentives for new entrants, and strengthening rate review processes can mitigate premium increases. For individuals, leveraging subsidies and carefully comparing plan details—even in a limited market—can help offset costs. While systemic change is needed, proactive steps can provide immediate relief in states where competition remains scarce.

Travel Insurance: Using Cigna Medical Insurance Abroad

You may want to see also

Explore related products

![]()

Consumer Choice Constraints: Discuss challenges for consumers with only one insurer option

In states where only one insurer offers plans on the Affordable Care Act (ACA) marketplace, consumers face a stark reality: limited choice. This constraint isn’t merely about fewer options; it’s about the erosion of bargaining power, reduced competition, and potential compromises in coverage quality. For instance, Wyoming and Alabama have counties with only one insurer, leaving residents with no alternative if premiums rise or coverage terms become unfavorable. This monopoly-like scenario forces consumers to accept whatever terms are offered, often with little recourse.

Consider the practical implications: without competition, insurers lack the incentive to lower premiums or improve benefits. A family in a single-insurer county might find themselves paying 20% more for a plan with higher deductibles than similar plans in competitive markets. For low-income individuals, this can mean forgoing necessary care due to cost. Even subsidies may not offset the burden, as the benchmark plan—used to calculate subsidy amounts—is often the second-lowest-cost silver plan, which doesn’t exist in these markets. This leaves consumers with fewer protections and higher out-of-pocket costs.

The lack of choice also stifles innovation. In competitive markets, insurers might offer telehealth services, wellness programs, or reduced copays for preventive care to attract customers. In single-insurer markets, such incentives disappear. For example, a diabetic patient might be denied access to a comprehensive disease management program simply because the insurer sees no need to invest in such services. This not only affects health outcomes but also perpetuates disparities in care quality across regions.

To navigate this challenge, consumers must become proactive advocates. First, research the insurer’s track record for customer satisfaction and claims processing. Second, leverage state insurance departments to file grievances if coverage terms are unfair. Third, explore off-exchange plans, though these often lack ACA subsidies. Finally, stay informed about policy changes at the federal and state levels, as legislative shifts could reintroduce competition. While these steps won’t eliminate the constraint, they empower consumers to make the most of their limited options.

Ultimately, the absence of choice in ACA marketplaces isn’t just an inconvenience—it’s a systemic issue that undermines the very principles of accessible, affordable healthcare. Until policymakers address this gap, consumers in single-insurer states must adapt, advocate, and demand better. Their health—and financial stability—depend on it.

Ambulance Coverage: Understanding Your Medical Insurance Benefits

You may want to see also

Explore related products

![]()

Policy and Regulatory Factors: Examine state and federal policies contributing to single-insurer markets

The Affordable Care Act (ACA) marketplaces were designed to foster competition among insurers, yet several states have ended up with only one insurer offering plans. This phenomenon isn’t random; it’s deeply rooted in policy and regulatory decisions at both the state and federal levels. To understand why some states have single-insurer markets, it’s essential to dissect the regulatory environment that shapes insurer participation. Federal policies, such as funding cuts for cost-sharing reductions and the elimination of the individual mandate penalty, have increased market uncertainty, prompting insurers to exit less profitable regions. Simultaneously, state-level regulations, like stringent network adequacy requirements or restrictive provider contracting rules, can deter insurers from entering or remaining in certain markets. These overlapping layers of policy create a complex landscape where only the most resilient or specialized insurers survive.

Consider the role of state-specific regulatory hurdles. States with rigorous approval processes for premium rate increases often force insurers to operate on thin margins, discouraging new entrants. For example, in states like Wyoming and Alaska, insurers must navigate both high healthcare costs and strict regulatory oversight, making it financially unviable for multiple insurers to compete. Conversely, states with more flexible regulatory frameworks, such as Georgia or Texas, tend to attract a broader range of insurers. This disparity highlights how state policies can either incentivize or stifle market competition. Policymakers must balance consumer protection with market viability, ensuring that regulations don’t inadvertently create monopolies.

Federal policies also play a pivotal role in shaping single-insurer markets. The Trump administration’s decision to shorten the ACA open enrollment period and reduce funding for outreach and advertising diminished consumer participation, shrinking the risk pool. Smaller risk pools mean higher per-member costs, which smaller insurers cannot sustain. Additionally, the federal government’s inconsistent approach to reinsurance programs has left insurers exposed to high-cost claims, further discouraging participation. States without their own reinsurance programs, like Mississippi and West Virginia, are particularly vulnerable to insurer exits. Implementing federal or state-based reinsurance programs could mitigate this risk, but political gridlock often stalls such initiatives.

A comparative analysis of states with single-insurer markets reveals a common thread: rural or low-population states face unique challenges. In these areas, the customer base is too small to justify the administrative and operational costs of entering the market. Federal policies aimed at rural healthcare, such as increased funding for rural providers, could indirectly improve insurer participation by stabilizing healthcare costs. However, without targeted interventions, these states will continue to struggle with limited insurer options. For instance, Nebraska’s recent success in attracting a second insurer came after the state implemented its own reinsurance program, demonstrating the impact of proactive policy measures.

To address single-insurer markets, policymakers must adopt a multi-pronged approach. First, federal and state governments should collaborate to stabilize the ACA marketplaces by reinstating cost-sharing reduction payments and strengthening reinsurance programs. Second, states should streamline regulatory processes to reduce administrative burdens on insurers without compromising consumer protections. Finally, targeted incentives, such as tax credits for insurers serving rural areas, could encourage market entry. By addressing both federal and state-level barriers, policymakers can foster a more competitive insurance landscape, ensuring consumers have meaningful choices in the ACA marketplaces.

Drug Rehab: Medical Insurance Coverage Explained

You may want to see also

Frequently asked questions

As of recent data, states like Wyoming, Alaska, and parts of Nebraska often have only one insurer offering ACA plans due to limited competition.

Factors like small population sizes, high healthcare costs, and low profit margins often discourage multiple insurers from participating in these states.

Yes, having only one insurer reduces plan options, potentially limiting flexibility in coverage, costs, and provider networks for consumers.

Yes, state and federal initiatives, such as subsidies for insurers and expanded Medicaid, aim to attract more companies to underserved markets.