Insurance companies are financial institutions that provide risk management services by offering policies to individuals and businesses, protecting them against potential losses in exchange for premium payments. These companies assess and underwrite risks, pool resources from policyholders, and pay out claims when insured events occur, such as accidents, property damage, or health issues. They operate across various sectors, including life, health, auto, home, and business insurance, and play a critical role in stabilizing economies by providing financial security and peace of mind to their customers. Understanding who insurance companies are and how they function is essential for making informed decisions about coverage and protection.

Explore related products

$36.99 $245.95

![Catalogue of Insurance Publications, American and Foreign: a Comprehensive List of Works Upon All Classes of Insurance, by Well Known Authors of All Countries 1911 [Leather Bound]](https://m.media-amazon.com/images/I/617DLHXyzlL._AC_UY218_.jpg)

What You'll Learn

- Company History: Founding date, key milestones, and evolution of the insurance company over time

- Products Offered: Types of insurance policies provided, including life, health, auto, and home

- Financial Strength: Ratings, assets, and stability indicators from agencies like A.M. Best

- Customer Service: Claims process, support channels, and customer satisfaction ratings or reviews

- Market Position: Competitive standing, market share, and industry rankings of the company

![]()

Company History: Founding date, key milestones, and evolution of the insurance company over time

The origins of insurance companies trace back to ancient civilizations, but the modern insurance industry as we know it began to take shape in the late 17th century. One of the earliest and most influential insurance companies, Lloyd’s of London, was established in 1688. Founded by Edward Lloyd, a coffeehouse owner whose establishment became a hub for merchants and shipowners to discuss trade and insure their ventures, Lloyd’s set the foundation for marine insurance. This marked the beginning of a structured approach to risk management, a concept that would evolve into the global insurance industry.

A key milestone in the evolution of insurance companies came in the 19th century with the rise of life insurance. The Equitable Life Assurance Society, founded in 1762 in London, is often credited as the first life insurance company. However, it was the Massachusetts Mutual Life Insurance Company, established in 1851, that popularized the concept in the United States. This period saw the introduction of actuarial science, enabling companies to calculate premiums based on statistical risk, a practice still central to the industry today. By the late 1800s, insurance had expanded beyond marine and life to include property, casualty, and health coverage, reflecting the growing complexity of industrial societies.

The 20th century brought significant technological and regulatory changes that reshaped the insurance landscape. The Great Depression of the 1930s forced governments to implement stricter regulations to protect policyholders, leading to the creation of state insurance commissions in the U.S. and similar bodies worldwide. Post-World War II, the industry experienced rapid growth as economic prosperity increased demand for insurance products. Companies like State Farm, founded in 1922, and Allstate, established in 1931, became household names by offering auto insurance to the burgeoning middle class. This era also saw the rise of reinsurance companies, which allowed primary insurers to manage risk more effectively.

In recent decades, the insurance industry has been transformed by digitalization and globalization. The advent of the internet in the 1990s enabled companies to streamline operations, offer online quotes, and reach a global customer base. Progressive Insurance, for example, pioneered the use of comparison tools in the 1990s, setting a new standard for transparency in pricing. Meanwhile, mergers and acquisitions have led to the consolidation of the industry, with giants like AIG and AXA dominating the market. Today, insurtech startups are disrupting traditional models by leveraging artificial intelligence, blockchain, and big data to offer personalized policies and faster claims processing.

Looking ahead, the evolution of insurance companies will likely be driven by climate change, cybersecurity risks, and shifting consumer expectations. Companies are increasingly offering specialized products, such as cyber insurance and parametric policies tied to weather events, to address emerging risks. As the industry continues to adapt, its history serves as a reminder of its core purpose: to provide financial security in an uncertain world. From Lloyd’s coffeehouse to today’s digital platforms, insurance companies have consistently innovated to meet the evolving needs of society.

Best Return of Premium Insurance Options for New York Residents

You may want to see also

Explore related products

![]()

Products Offered: Types of insurance policies provided, including life, health, auto, and home

Insurance companies are the architects of financial security, offering a suite of policies designed to protect individuals and families from life’s uncertainties. Among their core products are life, health, auto, and home insurance, each tailored to address specific risks. Life insurance, for instance, provides a financial safety net for beneficiaries in the event of the policyholder’s death, with options ranging from term life (coverage for a set period) to whole life (lifelong coverage with cash value accumulation). Understanding these distinctions is crucial for selecting a policy that aligns with long-term financial goals.

Health insurance, another cornerstone product, mitigates the financial burden of medical expenses. Policies vary widely, from comprehensive plans covering preventive care, hospitalization, and prescription drugs to high-deductible plans paired with health savings accounts (HSAs). For example, a 30-year-old individual might opt for a Bronze plan with a $6,000 deductible to lower monthly premiums, while a family with frequent medical needs may prioritize a Gold plan with higher premiums but lower out-of-pocket costs. Navigating these options requires assessing personal health needs and budget constraints.

Auto insurance is legally mandated in most regions, yet its components—liability, collision, and comprehensive coverage—offer flexibility. Liability coverage pays for damages to others in an accident, while collision and comprehensive protect the policyholder’s vehicle against accidents, theft, and natural disasters. A practical tip: drivers with older cars may consider dropping collision coverage if the annual premium exceeds 10% of the car’s value. This balance ensures adequate protection without overspending.

Home insurance, often bundled with auto policies for discounts, safeguards homeowners and renters against property damage and liability claims. Standard policies cover perils like fire, theft, and storms, but exclusions (e.g., floods, earthquakes) necessitate additional riders. Renters insurance, a subset of home insurance, protects personal belongings and liability at a fraction of the cost, typically $15–$30 monthly. For homeowners, regularly updating coverage to reflect property value and inflation is essential to avoid underinsurance.

In summary, insurance companies provide a diverse array of policies to address life’s unpredictable challenges. By dissecting the nuances of life, health, auto, and home insurance, individuals can make informed decisions that fortify their financial resilience. Each policy type demands careful consideration of personal circumstances, ensuring protection without unnecessary expense.

Primary Medical Insurance: What You Need to Know

You may want to see also

Explore related products

![]()

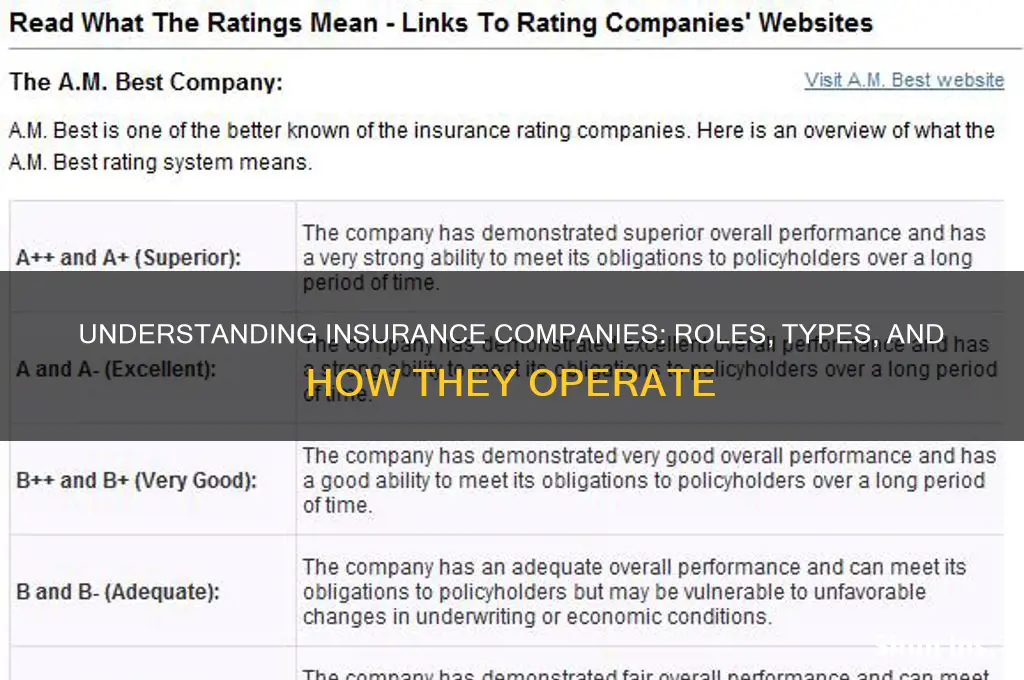

Financial Strength: Ratings, assets, and stability indicators from agencies like A.M. Best

Insurance companies are only as reliable as their ability to pay claims, making financial strength a non-negotiable criterion for policyholders. Agencies like A.M. Best, Moody’s, and Standard & Poor’s evaluate insurers using ratings (e.g., A++ for superior, B for fair), asset size, and stability indicators such as liquidity ratios and capital adequacy. For instance, a company with $50 billion in assets and an A.M. Best rating of A+ is generally considered safer than one with $5 billion and a B rating. These metrics aren’t just numbers—they’re a promise that your insurer will be there when disaster strikes.

To assess an insurer’s financial health, start with their A.M. Best rating, which ranges from A++ (superior) to D (poor). For example, State Farm and USAA consistently hold A++ ratings, reflecting their robust financial stability. Next, examine their total assets; larger assets often correlate with greater capacity to handle claims, though size alone isn’t decisive. Prudential Financial, with over $900 billion in assets, demonstrates scale, but smaller insurers like Erie Insurance (A+ rating) prove stability isn’t exclusive to giants. Cross-reference these with stability indicators like risk-based capital ratios, which measure an insurer’s ability to absorb losses—a ratio above 300% is typically reassuring.

While ratings and assets are critical, they’re only part of the story. A company’s investment portfolio, debt levels, and claims-paying history provide deeper insights. For instance, an insurer heavily invested in volatile markets may face liquidity issues during downturns, despite a high A.M. Best rating. Similarly, a company with a history of delayed claims payouts could signal operational inefficiencies. Policyholders should also consider the insurer’s market share and geographic focus; a regional insurer might excel in localized risks but lack the resources of a national player.

Practical tip: Before purchasing a policy, compare at least three insurers’ financial ratings and assets. Use A.M. Best’s website or tools like the National Association of Insurance Commissioners (NAIC) to access this data. For life insurance, prioritize companies with A+ or higher ratings and diverse asset portfolios to ensure long-term stability. For auto or home insurance, focus on liquidity ratios and claims-paying history, as these policies require quicker payouts. Remember, a financially strong insurer isn’t just about survival—it’s about peace of mind.

Top Agreed Value Insurance Companies: Which One Fits You Best?

You may want to see also

Explore related products

![]()

Customer Service: Claims process, support channels, and customer satisfaction ratings or reviews

The claims process is often the moment of truth for insurance customers, where the promise of protection meets reality. A streamlined, transparent process can turn a stressful situation into a manageable one. Leading insurance companies, such as State Farm and Allstate, have invested in digital tools like mobile apps and online portals that allow customers to file claims instantly, track progress in real time, and upload documents seamlessly. For instance, State Farm’s app enables policyholders to submit photos of damage directly from their smartphones, reducing processing times by up to 40%. However, not all companies excel here—some still rely on cumbersome paperwork and phone-only submissions, which can delay payouts and frustrate customers. The takeaway? A modern, user-friendly claims process isn’t just a perk; it’s a necessity for maintaining trust.

Support channels are the lifelines of customer service, and their effectiveness varies widely across insurers. Progressive, for example, offers 24/7 support via phone, chat, and email, ensuring customers can reach out whenever they need assistance. In contrast, smaller regional insurers often limit support to business hours, leaving customers in the lurch during emergencies. Chatbots, increasingly popular in the industry, can handle simple queries efficiently but often fall short for complex issues, leading to frustration. A study by J.D. Power found that customers prefer human interaction for claims-related inquiries, with 72% rating phone support as the most effective channel. The key is to strike a balance: offer multiple channels, ensure they’re staffed adequately, and integrate technology without sacrificing the human touch.

Customer satisfaction ratings and reviews provide a candid look at how insurers perform in the eyes of their policyholders. According to the 2023 U.S. Auto Insurance Study by J.D. Power, Amica Mutual and USAA consistently rank at the top for customer satisfaction, with scores of 900 and 890 out of 1,000, respectively. These companies excel in areas like claims handling, communication, and policy offerings. On the flip side, companies with lower ratings often struggle with delayed payouts, poor communication, and inflexible policies. Online reviews on platforms like Trustpilot and the Better Business Bureau (BBB) echo these trends, with customers praising responsive service and criticizing red tape. For consumers, these ratings are invaluable—they highlight which insurers deliver on their promises and which fall short.

To maximize satisfaction, customers should proactively engage with their insurer’s resources. Familiarize yourself with the claims process before an incident occurs; most companies provide step-by-step guides on their websites. Test their support channels—call, chat, or email—to gauge responsiveness. And don’t overlook the power of reviews; they offer unfiltered insights into real-world experiences. For insurers, the message is clear: invest in customer service, simplify processes, and prioritize transparency. After all, in the insurance business, satisfaction isn’t just a metric—it’s a measure of reliability when customers need it most.

Life Insurance and Medicaid: Understanding the Income Impact

You may want to see also

Explore related products

![]()

Market Position: Competitive standing, market share, and industry rankings of the company

The global insurance market is a highly competitive landscape, with thousands of companies vying for dominance. To understand an insurance company's market position, one must delve into its competitive standing, market share, and industry rankings. These metrics provide a snapshot of the company's strength, stability, and growth potential. For instance, as of 2023, Allianz SE holds a significant market share of approximately 8.5% in the global insurance market, ranking it among the top three insurance companies worldwide. This position is a testament to its robust product portfolio, strategic acquisitions, and strong brand presence.

Analyzing competitive standing involves examining a company’s ability to differentiate itself from rivals. Take Progressive Corporation, for example, which has carved out a niche in the auto insurance sector through its innovative usage-based insurance (UBI) programs. By leveraging telematics and data analytics, Progressive has not only increased customer retention but also captured a larger share of the tech-savvy demographic. Such differentiation is critical in a commoditized industry, where price competition often dominates. Companies that invest in technology, customer experience, and unique value propositions tend to outperform their peers in both market share and profitability.

Market share is a quantifiable measure of a company’s dominance within its industry. In the U.S. health insurance market, UnitedHealth Group leads with a market share of over 15%, driven by its diversified offerings, including health services and pharmacy benefits. However, market share alone does not tell the full story. It’s essential to consider growth trends and regional performance. For instance, while AXA has a smaller global market share compared to Allianz, its strong foothold in emerging markets like Asia positions it for faster growth in the coming years. Companies with a balanced geographic presence and diversified revenue streams are better equipped to weather economic fluctuations.

Industry rankings provide a comparative benchmark, highlighting a company’s standing relative to competitors. In the life insurance sector, companies like Prudential Financial and MetLife consistently rank among the top players due to their extensive product lines and strong distribution networks. However, rankings can be misleading if not contextualized. A company ranked lower in premium volume might still excel in customer satisfaction or financial stability, as measured by ratings agencies like A.M. Best or Moody’s. For instance, USAA, despite its smaller size, consistently ranks high in customer loyalty and financial strength, making it a formidable competitor in the markets it serves.

To assess market position effectively, stakeholders should focus on both quantitative and qualitative factors. Start by examining financial reports for market share and revenue growth. Next, analyze competitive differentiation through product innovation, customer reviews, and technological investments. Finally, cross-reference industry rankings with independent ratings to gain a holistic view. For investors, companies with a strong market position and sustainable competitive advantages offer lower risk and higher long-term returns. For consumers, understanding a company’s market standing can help in selecting a reliable insurer with the financial capacity to honor claims. In a dynamic industry like insurance, staying informed about market position is not just beneficial—it’s essential.

Keep Your Record Clean: Strategies to Reduce Accident Points

You may want to see also

Frequently asked questions

The insurance company is a financial institution that provides risk management services by offering policies to individuals or businesses in exchange for premiums. They protect against potential losses by pooling risks from multiple clients.

The role of an insurance company is to assess, underwrite, and manage risks, provide financial protection against unforeseen events, and compensate policyholders for covered losses as per the terms of their policies.

Insurance companies make money by collecting premiums from policyholders, investing those funds, and paying out claims only when necessary, ensuring that their income exceeds their expenses and claims payouts.

No, insurance companies vary in size, specialization, and the types of policies they offer. Some focus on life insurance, while others specialize in health, auto, or property insurance, and their services, rates, and coverage can differ significantly.

To choose the right insurance company, consider factors like financial stability, customer reviews, coverage options, premiums, claims process efficiency, and the company’s reputation in the industry. Research and compare multiple providers before deciding.