Health insurance is a critical component of financial and personal well-being, providing coverage for medical expenses and ensuring access to healthcare services. The question of who sells health insurance encompasses a wide range of entities, including private insurance companies, government-sponsored programs, and employer-based plans. Private insurers, such as Aetna, UnitedHealthcare, and Blue Cross Blue Shield, dominate the market, offering individual, family, and group policies tailored to diverse needs. Government programs like Medicare and Medicaid serve specific populations, including seniors, low-income individuals, and disabled persons. Additionally, many employers provide health insurance as part of employee benefits packages, often partnering with insurers to design comprehensive plans. Understanding the various sellers of health insurance is essential for individuals and families seeking the best coverage options to meet their healthcare needs.

Explore related products

What You'll Learn

- Insurance Brokers: Independent agents offering policies from multiple providers to suit individual needs

- Direct Insurers: Companies selling policies directly to consumers without intermediaries

- Employer-Sponsored Plans: Health insurance provided by employers as part of benefits packages

- Government Programs: Public health insurance like Medicare, Medicaid, and ACA Marketplace plans

- Online Marketplaces: Digital platforms comparing and selling health insurance policies from various providers

![]()

Insurance Brokers: Independent agents offering policies from multiple providers to suit individual needs

Insurance brokers are the Swiss Army knives of the health insurance world, offering a level of flexibility and customization that direct providers often can’t match. Unlike captive agents tied to a single company, independent brokers partner with multiple insurers, giving them access to a wide array of policies. This means they can tailor coverage to your specific health needs, budget, and lifestyle, whether you’re a 25-year-old freelancer seeking catastrophic coverage or a 55-year-old with chronic conditions needing comprehensive care. For instance, a broker might pair a high-deductible plan with a health savings account (HSA) for a healthy individual, while recommending a PPO with robust prescription drug benefits for someone managing diabetes.

Consider the process of working with a broker as a guided tour through the complex landscape of health insurance. They start by assessing your medical history, financial situation, and coverage priorities. For example, if you’re planning to start a family, they’ll prioritize plans with strong maternity benefits and pediatric care. Brokers also handle the legwork of comparing premiums, deductibles, and out-of-pocket maximums across providers, saving you hours of research. A practical tip: bring a list of your current medications and preferred doctors to your first meeting to ensure the broker can find a plan that aligns with your existing healthcare routine.

One of the most persuasive arguments for using a broker is their ability to navigate policy nuances that could save you money in the long run. For instance, some plans exclude specific treatments or require prior authorization for certain procedures—details that are easy to overlook when shopping solo. Brokers are trained to spot these red flags and explain how they might impact your care. Additionally, they can assist with subsidies and tax credits if you qualify for the Affordable Care Act marketplace, potentially lowering your monthly premiums by hundreds of dollars.

Comparatively, while online marketplaces offer convenience, they often lack the personalized touch of a broker. Algorithms can’t account for the subtleties of your health or financial situation, and they may steer you toward plans with hidden limitations. Brokers, on the other hand, act as your advocate, even after you’ve purchased a policy. They can help resolve claims disputes, explain benefits, and adjust your coverage as your life circumstances change. For example, if you switch jobs or move to a new state, a broker can quickly identify a new plan that maintains your current level of care without gaps in coverage.

In conclusion, insurance brokers are invaluable allies in the quest for the right health insurance policy. Their independence allows them to prioritize your needs over any single insurer’s bottom line, and their expertise ensures you’re not paying for coverage you don’t need or missing out on benefits that could protect your health and finances. If you’re overwhelmed by the options or unsure where to start, reaching out to a broker could be the most practical step you take in securing your healthcare future.

Placer County Medical Insurance: Enrollment Periods and You

You may want to see also

Explore related products

![]()

Direct Insurers: Companies selling policies directly to consumers without intermediaries

Direct insurers are reshaping the health insurance landscape by eliminating intermediaries, offering policies directly to consumers. This model cuts out brokers, agents, and other middlemen, often resulting in lower premiums for policyholders. Companies like Oscar Health and Bright Health Group exemplify this approach, leveraging technology to streamline the purchasing process. By using digital platforms, these insurers provide instant quotes, customizable plans, and transparent pricing, making it easier for consumers to compare options and make informed decisions. This direct-to-consumer model appeals particularly to tech-savvy individuals who value efficiency and autonomy in managing their healthcare coverage.

One of the key advantages of direct insurers is their ability to tailor policies to specific demographics or health needs. For instance, some companies focus on young, healthy individuals by offering lower premiums and wellness incentives, such as discounted gym memberships or telehealth services. Others target seniors with comprehensive Medicare Advantage plans that include prescription drug coverage and preventive care benefits. This specialization allows direct insurers to compete effectively with traditional providers, who often offer one-size-fits-all policies. However, consumers must carefully review plan details to ensure the coverage meets their unique health requirements.

Despite the benefits, the direct insurer model has limitations. Without intermediaries, consumers may miss out on personalized advice from agents who understand the nuances of different policies. This lack of guidance can lead to confusion, especially for those unfamiliar with insurance terminology or coverage options. Additionally, direct insurers may not offer the same breadth of plans as larger, established companies, limiting choices for individuals with complex health needs. To mitigate these risks, consumers should use online resources, such as comparison tools and customer reviews, to evaluate direct insurers thoroughly.

For those considering direct insurers, practical steps can enhance the decision-making process. Start by assessing your healthcare needs—consider factors like pre-existing conditions, prescription medications, and anticipated medical expenses. Next, compare plans from multiple direct insurers, focusing on premiums, deductibles, and out-of-pocket maximums. Take advantage of free trials or consultation services offered by some companies to test their platforms and customer support. Finally, read the fine print to understand exclusions and limitations, ensuring the policy aligns with your long-term health goals. By approaching the process methodically, consumers can maximize the benefits of direct insurance while minimizing potential drawbacks.

Appealing a Cigna Medical Insurance Claim: Your Step-by-Step Guide

You may want to see also

Explore related products

![]()

Employer-Sponsored Plans: Health insurance provided by employers as part of benefits packages

Employer-sponsored health insurance plans are a cornerstone of the American healthcare system, covering approximately 157 million workers and their dependents as of 2023. These plans, offered as part of employee benefits packages, typically share costs between the employer and the employee, making coverage more affordable than individual market plans. For instance, employers often cover 70-85% of premium costs for single employees and a slightly lower percentage for family coverage. This cost-sharing model not only reduces financial burden on employees but also serves as a strategic tool for employers to attract and retain talent in a competitive job market.

When evaluating employer-sponsored plans, employees should scrutinize the specifics of their coverage options. Most employers offer a choice between Health Maintenance Organizations (HMOs) and Preferred Provider Organizations (PPOs). HMOs generally require selecting a primary care physician and obtaining referrals for specialists, while PPOs offer more flexibility in choosing providers but at a higher out-of-pocket cost. For example, an HMO might charge a $20 copay for a primary care visit, whereas a PPO could charge $30 with the same provider. Employees should also review the plan’s deductible, typically ranging from $1,000 to $3,000 for individual coverage, and the out-of-pocket maximum, which caps annual expenses at $7,000-$8,000 for in-network services.

One often-overlooked aspect of employer-sponsored plans is their role in preventive care and wellness programs. Many employers incentivize healthy behaviors by offering reduced premiums or cash rewards for completing health assessments, participating in fitness challenges, or achieving specific health metrics, such as lowering cholesterol levels or quitting smoking. For instance, an employee might save $200 annually on premiums by participating in a workplace wellness program. These initiatives not only benefit employees’ health but also reduce long-term healthcare costs for both the individual and the employer.

Despite their advantages, employer-sponsored plans are not without limitations. Employees tied to their employer’s plan may face challenges during job transitions, as coverage often ends with employment. While COBRA allows individuals to continue their plan temporarily, it requires the employee to pay the full premium plus an administrative fee, often making it prohibitively expensive. Additionally, part-time workers or those in small businesses may not qualify for employer-sponsored insurance, as federal law only mandates coverage for companies with 50 or more full-time employees. This gap highlights the need for complementary policies, such as subsidies for individual market plans or expanded Medicaid eligibility, to ensure broader access to healthcare.

To maximize the benefits of an employer-sponsored plan, employees should actively engage in open enrollment periods, typically held annually. This is the time to assess changes in personal health needs, compare available plans, and adjust coverage accordingly. For example, an employee expecting a child might switch to a plan with lower copays for prenatal care and pediatric visits. Additionally, contributing to a Health Savings Account (HSA) or Flexible Spending Account (FSA) can provide tax advantages and help cover out-of-pocket expenses. By understanding and leveraging these features, employees can optimize their health insurance while minimizing costs.

Why Life Insurance Companies Require Death Certificates for Claims

You may want to see also

Explore related products

![]()

Government Programs: Public health insurance like Medicare, Medicaid, and ACA Marketplace plans

Government programs play a pivotal role in providing health insurance to millions of Americans, particularly those who might not otherwise afford coverage. Among these, Medicare, Medicaid, and the Affordable Care Act (ACA) Marketplace plans stand out as the cornerstone of public health insurance. Each program is designed with specific eligibility criteria and benefits, catering to diverse demographic needs. For instance, Medicare primarily serves individuals aged 65 and older, while Medicaid targets low-income families and individuals. The ACA Marketplace, on the other hand, offers subsidized plans to those who don’t qualify for Medicare or Medicaid but still need affordable coverage. Understanding these programs is essential for anyone navigating the complex landscape of health insurance.

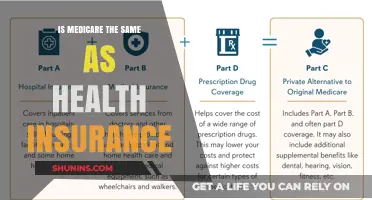

Medicare, established in 1965, is a federal program divided into several parts, each covering different healthcare services. Part A covers hospital stays, Part B handles outpatient services, Part C (Medicare Advantage) offers private insurance options, and Part D provides prescription drug coverage. Eligibility begins at age 65, though younger individuals with certain disabilities or conditions like End-Stage Renal Disease (ESRD) may also qualify. For example, a 67-year-old retiree might enroll in Part A and B for comprehensive coverage, while adding Part D to manage costly medications like insulin or statins. Medicare’s structured approach ensures seniors and disabled individuals have access to essential healthcare without overwhelming out-of-pocket costs.

Medicaid, a joint federal and state program, is tailored to assist low-income individuals and families, including children, pregnant women, and people with disabilities. Eligibility and benefits vary by state, but the program generally covers doctor visits, hospital stays, and long-term care services. For instance, a single parent earning below the federal poverty level in California could qualify for Medi-Cal (California’s Medicaid program), ensuring their children receive vaccinations, dental care, and mental health services. Unlike Medicare, Medicaid also covers custodial care, such as nursing home stays, making it a lifeline for those with limited financial resources.

The ACA Marketplace, established under the Affordable Care Act, provides a platform for individuals and families to purchase private health insurance plans at subsidized rates. Eligibility for subsidies is based on income, with those earning between 100% and 400% of the federal poverty level qualifying for premium tax credits. For example, a family of four earning $50,000 annually might save hundreds of dollars monthly on premiums through the Marketplace. Plans are categorized into metal tiers (Bronze, Silver, Gold, Platinum), each offering different levels of coverage and out-of-pocket costs. Silver plans, in particular, are popular because they qualify for cost-sharing reductions, reducing deductibles and copays for eligible enrollees.

While these government programs provide critical coverage, navigating them requires careful consideration. For instance, Medicare beneficiaries must enroll during specific periods to avoid penalties, and Medicaid applicants must meet stringent income and asset tests. ACA Marketplace enrollees should compare plans annually during open enrollment to ensure their coverage aligns with their healthcare needs. Practical tips include using online tools like the Medicare Plan Finder or Healthcare.gov to compare options, consulting certified navigators for personalized guidance, and keeping detailed records of enrollment and benefits. By leveraging these resources, individuals can maximize the value of public health insurance programs and secure the care they need.

Who Qualifies for Insurance Company Grants: Eligibility and Criteria Explained

You may want to see also

Explore related products

![]()

Online Marketplaces: Digital platforms comparing and selling health insurance policies from various providers

Online marketplaces have revolutionized the way consumers shop for health insurance, offering a centralized platform to compare policies from multiple providers. These digital hubs aggregate plans, allowing users to filter by coverage type, premium costs, deductibles, and network size. For instance, platforms like eHealth and HealthCare.gov provide side-by-side comparisons, making it easier to identify plans that align with specific needs, such as maternity care, prescription drug coverage, or mental health services. This transparency empowers consumers to make informed decisions without the pressure of direct sales tactics.

One of the key advantages of online marketplaces is their ability to simplify complex information. Many platforms use intuitive interfaces, with tools like cost estimators and coverage calculators. For example, a 35-year-old nonsmoker in California might discover that a Bronze plan with a $6,000 deductible costs $300 monthly, while a Gold plan with a $1,500 deductible costs $550. Such clarity helps users balance affordability with comprehensive coverage. Additionally, these platforms often highlight provider ratings and customer reviews, offering insights into claim processing efficiency and customer service quality.

However, navigating online marketplaces requires caution. While they offer convenience, the sheer volume of options can overwhelm users. For instance, HealthCare.gov lists over 50 plans in some regions, each with varying copays, coinsurance, and out-of-pocket maximums. To avoid decision paralysis, start by defining priorities: Is a low monthly premium more important than a broad provider network? Are specific medications or specialists non-negotiable? Practical tips include using the platform’s chat support for clarification and verifying that preferred doctors are in-network before enrolling.

Another critical aspect is understanding enrollment periods. Most online marketplaces adhere to strict open enrollment windows, typically from November 1 to January 15 for individual plans. Missing this deadline requires qualifying for a Special Enrollment Period (SEP), which applies to life events like marriage, job loss, or moving. For example, a 28-year-old who recently relocated can use an SEP to enroll within 60 days of the move. Platforms often include eligibility quizzes to guide users through these exceptions, ensuring compliance with regulations.

In conclusion, online marketplaces serve as invaluable tools for comparing and purchasing health insurance, but their effectiveness depends on user engagement. By leveraging their features—from cost comparisons to enrollment guidance—consumers can secure policies tailored to their health and financial needs. However, success hinges on proactive research, clear prioritization, and adherence to enrollment timelines. As the digital insurance landscape evolves, these platforms will likely incorporate AI and personalized recommendations, further streamlining the decision-making process.

Workers' Comp Insurance in Ohio: Application Process Simplified

You may want to see also

Frequently asked questions

Health insurance is sold by various entities, including private insurance companies, government agencies, and health insurance marketplaces. Examples include Aetna, Blue Cross Blue Shield, UnitedHealthcare, and state-based exchanges like Covered California.

No, hospitals do not sell health insurance. They provide medical services and may accept insurance from various providers, but insurance must be purchased through insurers, brokers, or marketplaces.

Employers do not sell health insurance but often offer group health insurance plans as part of employee benefits. These plans are typically provided through partnerships with insurance companies.

Yes, licensed insurance agents and brokers can help individuals and businesses find and purchase health insurance plans. They work with multiple insurers to offer a range of options.