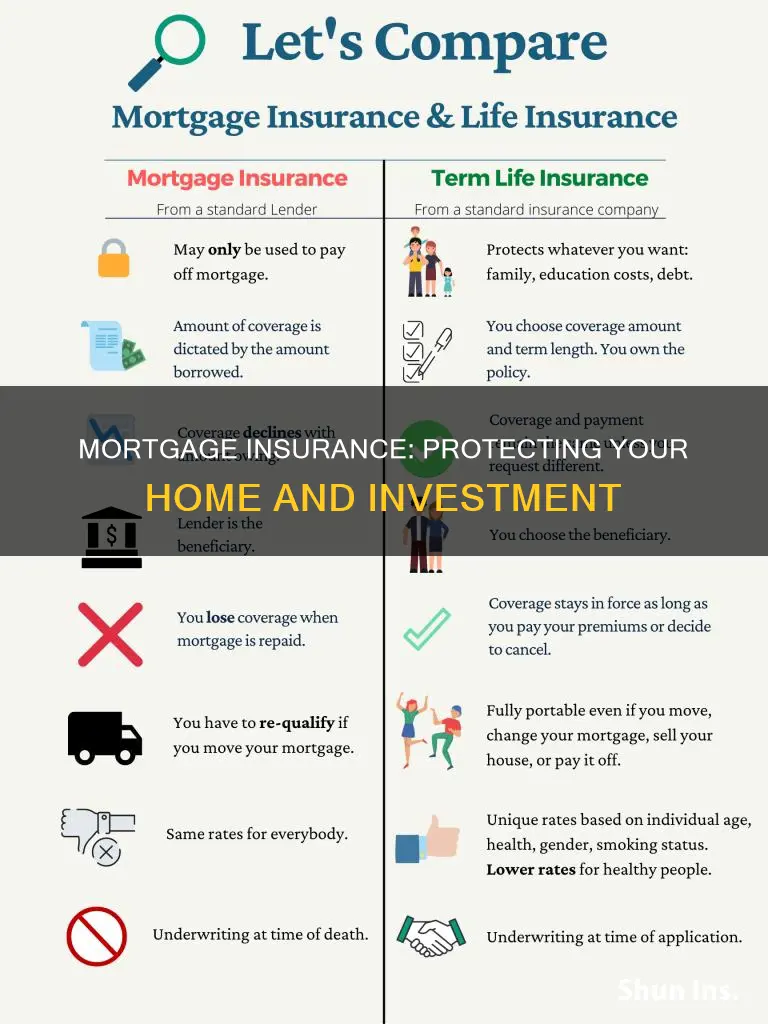

Mortgage insurance is a type of insurance that protects the lender in the event that the borrower can't repay their loan. It is typically required when a homebuyer's down payment is less than 20% of the purchase price of the home, as a larger down payment presents a lower level of risk to the lender. There are several types of mortgage insurance, including private mortgage insurance (PMI), borrower-paid mortgage insurance (BPMI), lender-paid mortgage insurance (LPMI), and Federal Housing Administration (FHA) mortgage insurance. The cost of mortgage insurance can be paid upfront, included in the monthly payments, or a combination of both, and it can increase the overall cost of the loan.

| Characteristics | Values |

|---|---|

| Who does mortgage insurance protect? | The lender, in the event that the borrower can't repay their loan. |

| Who needs mortgage insurance? | Homebuyers whose down payment is less than 20% of the purchase price of the home. |

| Types | Borrower-paid mortgage insurance (BPMI), lender-paid mortgage insurance (LPMI), single-premium mortgage insurance, split-premium mortgage insurance, private mortgage insurance (PMI), Federal Housing Administration (FHA) mortgage insurance, U.S. Department of Agriculture (USDA) loans, Department of Veterans' Affairs (VA)-backed loans. |

| Cost | The cost of mortgage insurance is included in the monthly payments on top of the regular mortgage payment. The cost varies depending on the size and type of the loan, the amount of the down payment, and the credit score. |

| Cancellation | Once the borrower has paid off some of the loan, they may be eligible to cancel their mortgage insurance. |

Explore related products

$12.98 $17.99

What You'll Learn

![]()

Lenders require mortgage insurance for low down payments

The exact cost of PMI depends on the specific terms of the loan and can be found in the mortgage documents. Borrowers can use a PMI calculator to estimate the cost before purchasing a home. Additionally, there are alternative options to avoid paying PMI, such as lender-paid mortgage insurance, special first-time homebuyer loans without PMI, or piggyback loans, which are a type of second mortgage that can help borrowers avoid PMI even with a low down payment.

While PMI is a common requirement for conventional mortgages, Federal Housing Administration (FHA) loans require a different type of mortgage insurance called a mortgage insurance premium (MIP). MIP is required for all FHA loans, regardless of the down payment amount, and has both upfront and annual costs. Similarly, loans from the U.S. Department of Agriculture (USDA) and the Department of Veterans Affairs (VA) have borrower-paid fees to protect lenders, even though they do not require mortgage insurance.

It is important to note that mortgage insurance does not protect the borrower but instead helps the lender manage the risk associated with offering loans to buyers with low down payments. By requiring PMI, lenders can lower their financial risk and qualify borrowers who might not otherwise be eligible for a loan. Once the borrower has achieved 20% equity in their home, they may be eligible to cancel their PMI and stop paying the monthly cost.

Overall, lenders require mortgage insurance for low down payments to mitigate their financial risk and ensure protection in case of borrower default. While this adds to the cost of the loan, it also enables borrowers with lower down payments to qualify for loans they might not have otherwise secured.

Greatland Insurance: Is It Worth Selling Their Policies?

You may want to see also

Explore related products

![]()

It protects the lender, not the borrower

Mortgage insurance, also called private mortgage insurance (PMI), is not designed to protect the borrower but the lender. It lowers the risk to the lender of making a loan to the borrower, so the borrower can qualify for a loan they might not otherwise be able to get. However, it increases the cost of the loan.

Mortgage insurance is typically required when a homebuyer's down payment is less than 20% of the purchase price of the home. In this case, the borrower is more likely to stop making payments if finances become strained or the value of the home decreases. With a smaller down payment, the buyer has less to lose by defaulting on the loan. The lender will then have to sell the property to make up for the unpaid loan balance.

Mortgage insurance protects the lender in the event that the borrower can't make their mortgage payments. If the property is sold through foreclosure and the sale is not enough to cover the mortgage balance in full, the insurance proceeds will allow the lender to recoup a portion of the loss.

FHA mortgage insurance includes an upfront premium included in the closing costs and a monthly premium, which is added to the principal, interest, real estate taxes, and homeowners' insurance that make up the mortgage payment. The upfront premium can be included in the loan, but monthly premiums must still be paid.

Rent Guarantee Insurance: Worth the Cost?

You may want to see also

Explore related products

![]()

It's included in your monthly payment

If you've taken out a mortgage with a down payment of less than 20% of the home's value, you likely have to pay mortgage insurance. This insurance protects the lender in case you default on your loan. It's included in your monthly payment, and there are two types: private mortgage insurance (PMI) and mortgage insurance premiums (MIP).

PMI is provided by private insurance companies to protect lenders, and its cost depends on various factors, including the loan type, the size of your down payment, and your credit score. The smaller your down payment, the higher the PMI you'll likely pay. You can typically request to have PMI removed once you reach 20% equity in your home.

MIP, on the other hand, is associated with government-backed loans like FHA loans. The FHA mortgage insurance, for instance, has two parts: an upfront fee paid at closing and an annual fee paid in 12 instalments as part of your monthly mortgage payment. Unlike PMI, FHA mortgage insurance usually lasts for the entire duration of the loan.

The monthly cost of mortgage insurance varies depending on the type of loan and the loan amount. It typically ranges from 0.2% to 1.5% of the loan amount on an annual basis. For example, if you borrow $200,000 and your mortgage insurance rate is 0.5%, you'll pay $1,000 for the first year of mortgage insurance. This amount is usually included in your monthly payments, so you'd pay about $83 extra each month.

It's important to note that mortgage insurance only protects the lender and doesn't provide any coverage for you as a homeowner. It's a necessary cost if you want to purchase a home with a small down payment, but it's in your best interest to cancel it as soon as you're able to meet the 20% equity threshold.

Home Insurance: Why It's Part of Your Mortgage

You may want to see also

Explore related products

![]()

You can cancel it once you've paid off some of your loan

Mortgage insurance is usually required when a homebuyer's down payment is less than 20% of the purchase price of their new home. It protects the lender in the event that the borrower defaults on their loan.

Mortgage insurance can be cancelled once you've paid off some of your loan. This is because, as you pay off your loan, the risk to the lender decreases. The specific requirements for cancelling your mortgage insurance will depend on the type of loan you have. For example, if you have a Federal Housing Administration (FHA) loan, you may not be able to cancel your mortgage insurance.

To cancel your mortgage insurance, you will need to submit a request in writing to your lender. You will also need to provide evidence that your loan balance is 80% or less of your home's original value. This can be done through a home sales contract or an appraisal. It's important to note that some lenders may require the principal balance to be reduced to 78% or even lower, so it's best to check with your lender before submitting your request.

In addition to paying off a portion of your loan, it's important to maintain a good payment history and ensure that your payments are current as required by the terms of your mortgage. By meeting these requirements, you can successfully cancel your mortgage insurance and save money on your monthly payments.

Cheapoair Insurance: Is It Worth the Cost?

You may want to see also

Explore related products

![]()

It's not required for VA loans

Mortgage insurance is typically required for homebuyers whose down payment is less than 20% of the purchase price of the home. This insurance lowers the risk to the lender of offering a loan to the buyer, but it increases the overall cost of the loan. Mortgage insurance is usually paid as a monthly premium on top of the regular mortgage payment.

However, VA loans do not require private mortgage insurance (PMI) or any other type of ongoing mortgage insurance. Instead, VA loans require a one-time VA funding fee, which can be financed into the loan amount. This fee ranges from 0.5% to 3.3% of the loan's total value and helps support the VA benefits program for future borrowers. The VA funding fee is a unique benefit of VA loans, as most home loan options have some form of monthly mortgage insurance.

The VA guarantee replaces mortgage insurance and functions similarly. The VA assures the lender that it will be repaid if the veteran can no longer make payments. This allows lenders to issue loans at superior terms, such as purchasing with no money down, capping what borrowers pay in closing costs, and offering competitive interest rates.

Therefore, VA loans provide an alternative for buyers who cannot put down more than 20% of the purchase price, as they may not have to pay PMI when taking out a home loan.

Farmers Insurance Open: Navigating Parking Options

You may want to see also

Frequently asked questions

Mortgage insurance protects the lender in the event that you fall behind on your payments. It lowers the risk to the lender of making a loan to you, so you can qualify for a loan that you might not otherwise be able to get.

The cost of mortgage insurance depends on the type of loan you have. For FHA loans, there is an upfront premium included in your closing costs and a monthly premium, which is added to the principal, interest, real estate taxes, and homeowners' insurance. For conventional loans, private mortgage insurance (PMI) rates vary by down payment amount and credit score.

Yes, once you’ve paid off some of your loan, you may be eligible to cancel your mortgage insurance. If you have a conventional loan, you can cancel your PMI after you have over 20% equity in your home. For FHA loans, you will continue to pay your mortgage insurance premiums throughout the life of the loan if you make a down payment of less than 10%.