Receiving a ticket can have a significant impact on insurance rates, with costs potentially increasing by hundreds of dollars annually. This is because insurance companies view traffic violations as indicators of risky behaviour, which could lead to accidents and subsequent claims. While the impact of a first-time offence may be less severe, the accumulation of multiple tickets will likely result in substantial premium increases. Additionally, factors such as age, driving experience, and claims history can further influence insurance rates. Understanding these factors and managing driving records is crucial for drivers aiming to minimise insurance costs.

| Characteristics | Values |

|---|---|

| Average increase in insurance cost | $2,486 per year or $80 per month |

| Highest increase in insurance cost | $121 per month |

| Lowest increase in insurance cost | $22 per month |

| Average increase in insurance cost (North Carolina) | $1,000 per year |

| Average increase in insurance cost (Geico, North Carolina) | $121 per month |

| Average increase in insurance cost (State Farm, North Carolina) | $47 per month |

| Average increase in insurance cost (State Farm) | $22 per month |

| Average increase in insurance cost (Idaho Farm Bureau) | $0 |

| Average increase in insurance cost (Maryland Auto Insurance) | $0 |

| Average increase in insurance cost (Umialik) | $0 |

| Number of points added to license (Arizona) | 3 points |

| Number of points for license suspension (Arizona) | 8 points |

Explore related products

What You'll Learn

![]()

A single ticket can increase insurance costs by hundreds of dollars

The increase in insurance costs after a ticket is due to insurers viewing traffic violations as indicators of risky behaviour, which could potentially lead to accidents. As a result, insurance companies may increase premiums to offset the perceived higher risk. Additionally, a speeding ticket can result in points being added to a driver's license, which further increases the likelihood of higher insurance rates.

To mitigate the impact of a ticket on insurance costs, drivers can consider the following strategies:

- Shopping around for a new insurance policy: Different insurers may have varying rates for drivers with a speeding ticket, so it's worth comparing quotes to find a more affordable option.

- Raising the deductible: Increasing the deductible can lower the premium, but it's important to ensure sufficient funds to cover the higher deductible in case of an accident.

- Asking about discounts: Bundling insurance policies or considering usage-based insurance for low-mileage drivers can help reduce overall insurance costs.

- Contesting the ticket: In some cases, it may be possible to plead guilty with a deferral, where the court agrees to delay entering the ticket into the driver's record. If no additional traffic citations occur by the scheduled date, the original ticket may be dismissed.

It's important to note that insurance rates may not increase immediately after receiving a ticket. Insurers typically review a driver's Motor Vehicle Record (MVR) at policy renewal, so the rate increase may occur at that time. Additionally, the impact of a speeding ticket on insurance rates may lessen over time if no new violations are incurred.

Why Insurance Rates are Increasing for Everyone

You may want to see also

Explore related products

![]()

The number of points on your license increases with traffic violations

In most states in the US, a certain number of points are added to your license for every traffic law violation. The number of points added per violation varies by state. For example, Arizona assigns three points for a speeding violation. If a driver accumulates eight or more points within 12 months, the state may require them to attend traffic school or suspend their license for up to a year. While insurance companies do not directly consider these points when calculating car insurance rates, accumulating a significant number of points due to multiple violations will likely result in higher insurance premiums.

Insurers view traffic violations as indicators of risky driving behaviour, which could potentially lead to accidents. As a result, they may increase insurance premiums to offset the perceived higher risk. The impact of a traffic violation on insurance rates can vary depending on factors such as the insurer, driving record, insurance history, and the specific violation. Some insurers may not increase rates after a single speeding ticket, while others may significantly raise premiums.

The number of points on a driver's license and the associated insurance implications can vary depending on the state and the nature of the violation. For instance, in North Carolina, a speeding ticket typically remains on the driving record for three years from the conviction date, but its impact on insurance rates may persist even longer. Most insurers in the state apply a surcharge for three to five years after a violation, and the base rate may continue to increase at renewal.

It's important to note that the presence of points on a driver's license can have significant financial consequences. Higher-risk drivers may face increased insurance premiums or even difficulty finding insurance coverage. Additionally, the accumulation of points can result in penalties such as license suspension or the requirement to attend traffic school. Therefore, it is advisable to prioritise safe driving practices and adhere to traffic laws to minimise the risk of accumulating points and incurring higher insurance costs.

To mitigate the impact of traffic violations on insurance rates, drivers can consider several options. Firstly, shopping around for insurance policies can help identify insurers who do not significantly penalise first-time violations. Secondly, raising the deductible can lower the premium, but it's important to ensure sufficient funds to cover the higher deductible in the event of an accident. Lastly, exploring discounts, such as bundling insurance policies or considering usage-based insurance, can help reduce overall insurance costs.

How Long Until Your Insurance Rates Drop After a Citation?

You may want to see also

Explore related products

![]()

Out-of-state tickets can increase insurance costs

Out-of-state speeding tickets can increase insurance costs, but this is not always the case. Most states have interstate reciprocal agreements, such as the Driver License Compact (DLC), that require them to share information on convictions for moving violations. However, some states, like Colorado and Pennsylvania, don't add minor out-of-state violations like speeding tickets to your driving record. Additionally, insurance companies usually check your driving record for the past 3-5 years, but due to state laws, some violations may only be visible for 3 years.

The impact of an out-of-state speeding ticket on your insurance costs also depends on your state and insurer. Some states forbid insurance companies from considering texting tickets or red-light camera tickets for rate-setting purposes. In states where it's not prohibited, insurers may treat these as minor moving violations, which can lead to a rate increase. Similarly, the number of points added to your license for a speeding violation varies by state, and a significant accumulation of points can indirectly lead to higher insurance rates.

The number of speeding tickets you've received also plays a role in insurance rate increases. While a single ticket may not affect your insurance costs, multiple speeding tickets within a certain period, such as two or more in three years, will likely result in an insurance rate increase. Additionally, the type of violation matters; more serious offenses will generally lead to higher premium increases.

To mitigate the impact of an out-of-state speeding ticket on your insurance costs, you can consider taking a defensive driving class, which can help remove points from your motor vehicle record and may even provide discounts with certain insurers. Additionally, maintaining a good driving record and shopping around for insurance policies can help you find more favourable rates, as insurers differ in how they treat violations.

Go Skippy Insurance: Is It Worth the Hype?

You may want to see also

Explore related products

![]()

A DUI conviction will likely increase your insurance premium

In some cases, insurance companies may refuse to renew policies or offer coverage to those with a DUI conviction. This refusal to insure drivers with a DUI conviction can result in significant financial consequences, impacting an individual's ability to continue living their life as normal. The cost of insurance after a DUI can be a burden, with some people experiencing increases of upwards of $1,000 in their annual premium.

The length of time that a DUI conviction will impact your insurance rates can vary. In most states, a DUI will remain on your driving record for three to five years, after which the impact on your insurance rates may lessen. However, a DUI conviction will remain on your driving record permanently, and you may still be considered a high-risk driver even after the initial period has passed.

It is important to note that the impact of a DUI on your insurance rates is not immediate and will typically occur at the time of policy renewal. This delay gives individuals time to seek legal counsel and explore options to reduce the charges or have them dismissed. Additionally, shopping around and comparing rates among multiple insurers can help individuals find the best deal for their insurance coverage after a DUI conviction.

Non-Admitted Insurance Carriers: What's the Deal?

You may want to see also

Explore related products

![]()

The type of car you drive affects insurance costs

The type of car you drive can significantly impact your insurance costs. The make and model of your car influence your insurance premiums. Cars with expensive components or repairs tend to have higher insurance premiums. On the other hand, vehicles with safety features like anti-lock brakes, electronic stability control, and theft prevention systems often have lower insurance costs, as these features reduce the likelihood of accidents and the cost of damages.

The age of your car also matters. Older cars are generally cheaper to insure than newer ones, except for classic or collectible cars. The brand and model year of a car are crucial factors in determining insurance rates. Foreign cars, for instance, often have more expensive parts than domestic vehicles, and luxury cars tend to be more costly to repair and insure.

In addition to the type of car, other factors such as your driving record, location, credit history, and policy choices can also influence your insurance costs. Your insurance rates may increase due to speeding tickets, DUIs, or accidents. Insurance companies consider these factors when assessing your risk as a driver.

It's worth noting that insurance rates can vary by state, city, and ZIP code. Some states, like California, Hawaii, Massachusetts, and Michigan, have restricted the use of credit scores in determining insurance rates. When shopping for insurance, it's beneficial to compare quotes from different companies, as rates can vary significantly.

AmFam's Customer-Centric Approach to Insurance

You may want to see also

Frequently asked questions

Insurance companies view speeding tickets as indicators of risky behaviour, which could potentially lead to accidents. As a result, they may increase your premiums to offset the perceived higher risk. The more tickets you have, the more likely your insurance rates will rise.

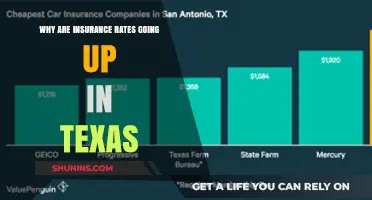

According to a 2024 analysis by NerdWallet, the cost of car insurance typically goes up by about 25% after a speeding ticket. On average, a driver convicted of speeding will pay $2,486 a year for full coverage insurance. However, the increase in cost may vary depending on factors such as your insurance company, driving record, insurance history, and the state you live in.

If you have received your first speeding ticket, it may not affect your insurance costs at all. Some insurers do not raise rates after a single violation. If your insurer does increase your premium, you may be able to find another company that will not penalise you. Additionally, you can try to lower your premium by raising your deductible, shopping for quotes after your driving record improves, or reconsidering the type of car you drive.