Life insurance is a crucial tool for Canadians to protect their loved ones financially in the event of their death. It is a contract between the policyholder and the insurer, where the insurer agrees to pay a lump sum of money to the beneficiaries chosen by the policyholder upon their death. This lump sum can be spent by the beneficiaries in any way they choose, such as covering mortgage and loan payments, children's education, or investments and retirement plans. In Canada, there are two main types of life insurance: term life insurance and permanent life insurance. Term life insurance covers a specified period, usually 10, 20, or 30 years, and provides affordable coverage with flexible options. On the other hand, permanent life insurance offers lifetime coverage and often includes a cash value component, allowing policyholders to borrow or withdraw funds. Understanding the different types of life insurance and their benefits is essential for Canadians to make informed decisions about their financial security and the well-being of their loved ones.

| Characteristics | Values |

|---|---|

| Purpose | Financial protection for loved ones |

| Types | Term life insurance, permanent life insurance, whole life insurance, universal life insurance, disability insurance, joint life insurance |

| Benefits | Tax-free death benefits, tax-sheltered cash value growth, non-taxable policy loans, reduced tax liability |

| Considerations | Age, health, lifestyle habits, number of dependents/beneficiaries, existing coverage through employer |

What You'll Learn

- Peace of mind: knowing your family is financially secure

- Tax benefits: tax-free death benefits, tax-sheltered cash value growth

- Affordability: term life insurance is a popular, affordable option

- Flexibility: choose from term or whole life insurance

- Additional benefits: borrow against your policy or receive a cash value payout

![]()

Peace of mind: knowing your family is financially secure

Life insurance is a contract between an insurer and a policyholder. In exchange for monthly payments, the life insurance company pays a death benefit to your beneficiaries when you pass away. This benefit is a lump sum of tax-free money that can be spent in any way your beneficiaries choose.

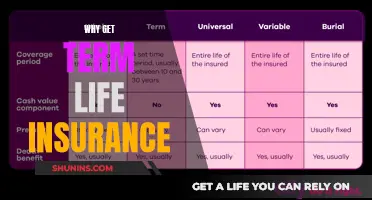

Life insurance can help financially protect your loved ones. Canadian residents can choose from term life insurance or permanent life insurance plans. Term life insurance is a temporary option that expires at the end of each term, usually after 10, 20, or 30 years. Permanent life insurance, on the other hand, lasts for a lifetime and often builds up a cash value that can be borrowed against or withdrawn.

If you have dependents, life insurance premiums are worth the cost as they provide peace of mind knowing your family will be taken care of financially when you pass away. This is especially important during key life events such as buying a home, having children, or getting married, as there are those who depend on your income to maintain their quality of life.

With life insurance, your family won't have to sell assets to cover outstanding debt, such as mortgage and loan payments. It can also help with children's education expenses, allowing them to graduate without student debt, and ensure your family can keep up with investment and retirement plans. In addition, permanent life insurance policies can provide a tax-preferred savings portion, allowing you to borrow or withdraw funds. However, it's important to note that borrowing or withdrawing funds may reduce the policy's death benefit and could have tax implications.

Fixed Annuities: Life Insurance's Secure Investment Option

You may want to see also

![]()

Tax benefits: tax-free death benefits, tax-sheltered cash value growth

Life insurance is a valuable tool for tax planning in Canada. It can be used to minimise tax liabilities and protect assets. One of the primary advantages of life insurance in Canada is the tax-free death benefit. When a policyholder passes away, the proceeds paid to their named beneficiaries are generally tax-free. This allows families to receive the full value of the policy without any deductions, providing financial security during difficult times. The death benefit can be used to cover funeral expenses, pay off debt left behind, supplement income, or provide for other needs.

There are certain instances where a life insurance policy may be taxable in Canada. For example, if you do not name a beneficiary, your estate will become the default beneficiary, and the death benefit will be subject to estate taxes. It is important to appoint a beneficiary to simplify the settlement process and eliminate extra fees and potential taxes. Your beneficiary can be a spouse, child, other family member, friend, or even a charitable organisation, trust, or business.

Another instance where life insurance may be taxable is when you withdraw from the cash value of a permanent policy or you sell or cancel a permanent policy. The cash value of permanent life insurance policies grows tax-free while the policy is in effect. However, if you withdraw from the cash value or cancel the policy, you may be subject to taxes or fees. Permanent life insurance policies, such as whole and universal, are more likely to have tax implications, such as paying tax on cash value.

Term life insurance, on the other hand, does not include a cash value, and therefore, there is no cash value to withdraw or surrender. However, term life insurance death benefits may be taxable if there is no named beneficiary. It is important to note that the tax rules regarding life insurance can be complex and may depend on various factors. Consulting with a qualified tax professional is recommended to determine the best type of life insurance policy and coverage amount for your individual needs.

Misrepresentation in Life Insurance: Understanding the Fine Line

You may want to see also

![]()

Affordability: term life insurance is a popular, affordable option

Life insurance is a way to financially protect your loved ones after you die. In Canada, there are two main types of life insurance: term life insurance and permanent life insurance. Term life insurance is a popular option for those seeking an affordable way to ensure their loved ones are taken care of when it matters most.

Term life insurance is a temporary coverage option that provides financial protection for a set period, typically between 5 to 40 years. You can choose the length of coverage that best suits your needs, whether it's 10, 15, 20, or more years. The flexibility of term life insurance allows you to customise your coverage, including additional benefits and the option to convert to permanent life insurance later on.

One of the most significant advantages of term life insurance is its affordability. When you purchase a term life insurance policy, you pay a fixed premium for the entire duration of the term. These premiums are generally lower than those of permanent life insurance, especially when you first buy the policy. The premiums remain the same and won't increase during the term, making it easy to factor into your budget.

The affordability of term life insurance makes it an attractive option for individuals and couples seeking financial security for their families. For example, joint first-to-die term insurance covers both partners under the same policy, and it is usually less expensive than two identical single policies. Additionally, term life insurance can be tailored to your specific needs and budget. Advisors are available to help you determine the right amount of coverage and the length of the term, ensuring that you get the protection you need at a price you can afford.

In summary, term life insurance is a popular choice in Canada due to its affordability and flexibility. It allows individuals and families to obtain financial protection at a lower cost compared to permanent life insurance. With customisable coverage, fixed premiums, and the option to convert to permanent insurance later, term life insurance provides a practical solution for those seeking to secure their loved ones' financial future.

Life Insurance: Knowing When to Downsize Your Policy

You may want to see also

![]()

Flexibility: choose from term or whole life insurance

When it comes to life insurance in Canada, you have the flexibility to choose between term life insurance and whole life insurance (also known as permanent life insurance). Both options are widely available from Canada's biggest life insurance companies.

Term life insurance provides coverage for a specific period, making it ideal for temporary needs such as mortgage payments, funding children's education, or income replacement. It is generally more affordable than whole life insurance, with premiums based on the length of the term. However, term life insurance does not accumulate cash value, and once the term ends, the coverage ends without any payout.

On the other hand, whole life insurance offers lifelong coverage as long as you continue paying your premiums. It includes an investment component that grows over time, allowing you to build retirement wealth. Whole life insurance policies have higher premiums due to their lifelong coverage and savings feature, but these premiums are typically fixed for your lifetime.

The choice between term and whole life insurance depends on your individual needs and financial goals. Term life insurance is suitable if you require coverage for a specific period and want an affordable option. In contrast, whole life insurance is ideal if you want lifelong coverage, estate planning capabilities, and the ability to build retirement savings through the policy's cash value.

It is generally recommended to purchase life insurance, including term or whole life policies, at a younger age to lock in lower premiums. By considering your financial situation, future goals, and the level of flexibility you desire, you can make an informed decision about the type of life insurance that best suits your needs in Canada.

Life Insurance: Is It Legally Compulsory?

You may want to see also

![]()

Additional benefits: borrow against your policy or receive a cash value payout

Life insurance is a way to financially protect your loved ones after you die. In Canada, there are two main types of life insurance: term life insurance and permanent life insurance. Term life insurance is generally cheaper and only covers you for a limited period, whereas permanent life insurance covers you for your entire life and often includes additional benefits, such as the ability to borrow against your policy or receive a cash value payout.

Permanent life insurance policies usually build up a cash value, meaning you get a payout if you cancel your policy. This cash value can be used as collateral for a loan, allowing you to borrow money from your insurer. This can be a quick and easy way to access cash, and it doesn't affect your credit score. You can pay back the loan on your own schedule, and if you pay it back early, you may even receive a refund for any interest you overpaid. Additionally, since the loan is secured by the cash value of your policy, there is no need for a credit check.

However, it's important to consider the potential downsides of borrowing against your life insurance policy. It can take a long time, often upwards of 10 years, to build up enough cash value to borrow from. Interest on the loan will accumulate over time, and if left unpaid, could significantly reduce the amount of money your beneficiary will receive upon your death. Withdrawing money from your policy also reduces your current and future dividends and may have tax implications.

Another option is to simply withdraw the cash value from your policy instead of borrowing against it. Withdrawing the money means liquidating that part of the asset, and you cannot put the money back into your policy. While this option avoids interest charges and penalties associated with loans, it can still impact your taxes and reduce your death benefit.

Overall, while borrowing against your life insurance policy or receiving a cash value payout can be a useful financial tool, it's important to carefully consider the potential advantages and disadvantages before making any decisions.

Life Insurance: Open Enrollment and You

You may want to see also

Frequently asked questions

Life insurance is a contract between an insurer and a policyholder. In exchange for monthly payments, the life insurance company pays a death benefit to your beneficiaries when you pass away.

Life insurance policies fall into two categories: term life insurance and whole life insurance. Term life insurance is temporary and expires at the end of each term, while whole life insurance is permanent and lasts a lifetime.

Life insurance can help financially protect your loved ones in the event of your death. It can also help with mortgage and loan payments, children's education, and investments and retirement. Additionally, it can reduce your tax liability and provide peace of mind, knowing your family will be taken care of.

The first step is to consult an experienced insurance advisor to understand the different options available. Consider your personal situation, financial goals, and the amount of coverage you need. Factors such as age, health, and lifestyle habits will also impact the cost of premiums.