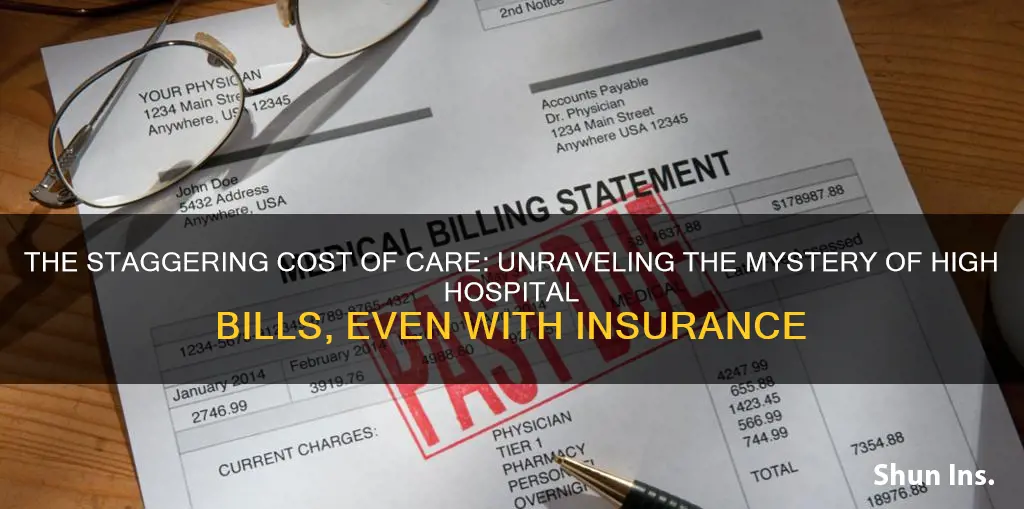

The cost of healthcare in the US is rising, and even those with insurance are facing high medical bills. There are several reasons for this, including surprise medical bills, administrative costs, rising doctors' fees, the high cost of surgical procedures and diagnostic tests, and soaring drug costs. High insurance premiums and deductibles can also contribute to high hospital bills, even for those with insurance. Additionally, insurance companies may not be motivated to keep costs low, as they earn a percentage of the bill. The lack of competition in the healthcare market also plays a role, as insurers are limited in their ability to negotiate lower prices.

| Characteristics | Values |

|---|---|

| High insurance premiums | High premiums can cause employers to worry about how they will pay for their company plans. |

| Lack of competition | Insurance companies have to include specific healthcare systems in their network and are unable to refuse their charges. |

| Insurance company incentives | Insurance companies may not be incentivized to reduce costs for large, self-insured company plans as they earn a percentage of the bill. |

| Hospital consolidation | When hospitals consolidate, prices go up. |

| High doctor and nurse salaries | American doctors and nurses earn more than their counterparts in other wealthy countries. |

| Administrative costs | Administrative costs account for at least 25% of healthcare costs in the US. |

| High drug costs | A RAND Corporation report found that prescription drug prices in the US are on average 256% higher when compared to 32 other countries. |

| High surgical procedure costs | The cost of a hip replacement in the US is about $10,000 higher than the next highest cost in Australia. |

| High diagnostic test costs | An MRI scan in the US costs between $1,110-$3,031, compared to $811 in New Zealand. |

| Deductibles | Deductibles are a fixed dollar amount that needs to be paid within a defined period before an insurer will start to cover costs. |

| Copays | A copay is a fixed dollar amount that is paid every time medical care is received. |

| Coinsurance | Coinsurance is when a patient pays a percentage of the total cost, e.g. 80/20 split between the insurance company and the patient. |

Explore related products

What You'll Learn

![]()

High premiums and deductibles

A premium is the amount paid monthly for health insurance. A deductible is an annual threshold, distinct for every plan, that must be paid out of pocket before insurance starts covering bills. Deductibles may range from a few hundred dollars to several thousand.

High-deductible health plans (HDHPs) are affordable health insurance plans with relatively low monthly premiums. However, these plans have higher deductibles and out-of-pocket maximums, meaning more healthcare expenses are paid by the individual. Because of this, HDHPs are best suited for younger, healthier individuals who don't need to visit the doctor or hospital often.

For those with high-deductible plans, there is the option to pair the insurance with a health savings account (HSA). An HSA is a savings account that allows individuals to put pre-tax dollars aside to pay for qualified medical expenses. Funds in an HSA can be used to pay deductibles, copayments, coinsurance, and other healthcare costs. Additionally, unspent HSA funds roll over to the next year, and the account may earn interest or other earnings.

While high-deductible plans can save money for those who are young and healthy, they can be more expensive than anticipated if unexpected medical bills arise. A deductible can be very high, and these plans can be more costly for those with many medical issues.

Explore related products

![]()

Surprise medical bills

Surprise billing, also known as balance billing, can add hundreds or thousands of dollars to a patient's medical bill. It occurs when a doctor or provider who is not in a patient's insurance network becomes involved in their care. For instance, a patient may go to an in-network hospital but receive treatment from emergency room physicians or anesthesiologists who are out-of-network, resulting in unexpected bills.

This issue has gained widespread attention, with 70% of Georgians reporting struggles with healthcare costs. In response, consumer protection laws at both the state and federal levels have been enacted to safeguard individuals from surprise medical bills.

The No Surprises Act (NSA), passed by Congress in 2020 and effective as of January 1, 2022, is a federal law that protects consumers from surprise medical bills. It prohibits surprise billing for emergency and non-emergency care provided by out-of-network providers working at in-network hospitals. The Act also mandates that patients are only liable for in-network cost-sharing amounts, meaning they cannot be charged more than their in-network rate for certain non-emergency out-of-network services.

Additionally, the NSA provides protections for uninsured individuals. Under this law, uninsured patients are entitled to receive a "good faith estimate" of charges before receiving care. If the final bill exceeds the estimate by at least $400, patients have the right to dispute the charges through a patient-provider dispute resolution process within 120 days of receiving the bill.

The NSA also establishes an independent dispute resolution process for payment disagreements between insurers and providers, keeping patients out of these disputes. This process is known as "baseball arbitration," where the provider and insurer present their proposed reimbursement amounts to an arbitrator, who then selects one of the proposals.

At the state level, laws such as the Georgia Surprise Billing Consumer Protection Act and Virginia's balance billing law provide similar protections against surprise medical bills. These laws aim to prevent unexpected billing and ensure fair and transparent billing practices.

Understanding Term Insurance Compatibility with Islamic Principles

You may want to see also

Explore related products

![]()

High cost of surgical procedures

Surgical procedures are expensive due to a variety of factors, and the cost of surgery can vary widely depending on the type of procedure and the patient's individual circumstances. Here are some key reasons why surgical procedures are often costly:

- Complexity and Precision Required: Certain surgical procedures, such as brain surgery or organ transplants, require extreme precision and a high level of expertise. The involvement of multiple highly skilled physicians, nurses, and support staff drives up the cost.

- Operating Room and Equipment Costs: The use of state-of-the-art equipment and facilities contributes to the high cost of surgery. Operating rooms are billed in increments, and the fees include sterilization, use of instruments, anesthesia machinery, and post-surgery cleaning.

- Implants and Medical Devices: Surgical procedures that involve implants, such as artificial hips or cardiac stents, incur additional costs. These devices are typically expensive due to the research and development required, as well as the need for sterilization and long-term performance.

- Medication and Anesthesia: The cost of medication and anesthesia used during and after surgery can be significant. This includes not only the drugs administered during the procedure but also any medications required for pain management or to prevent infection post-surgery.

- Pre- and Post-Surgical Care: The cost of surgery is not limited to the procedure itself. Pre-surgical consultations, tests, and treatments add to the overall expense. Additionally, post-surgical care, including inpatient stays, ICU care, and physical therapy, can significantly increase the final bill.

- Insurance Coverage and Negotiation: Insurance coverage can vary widely, and patients may be responsible for deductibles, copays, and coinsurance. Insurance companies often negotiate discounts with healthcare providers, but the final amount covered may still leave patients with substantial out-of-pocket expenses.

- Geographic Location and Competition: The cost of surgery can vary based on geographic location. In areas with limited competition among healthcare providers, prices tend to be higher. This lack of competition allows hospitals and doctors to charge higher rates.

- Consolidation of Hospital Systems: The consolidation of hospital systems through mergers and acquisitions has contributed to rising surgery costs. Larger hospital systems have greater negotiating power and can charge higher rates to insurance companies and patients.

**Primary Protocols: Navigating the Billing Hierarchy of Insurance**

You may want to see also

Explore related products

![]()

Rising doctors' fees

The cost of healthcare in the US is soaring, and rising doctors' fees are a significant factor. From 2003 to 2016, the price of a doctor's office visit rose from $60 to $101, and since then, it has risen further to between $150 and $350. This increase is influenced by several factors, including the complexity of the medical decision-making, the location of care, and the necessary tests conducted.

One of the primary drivers of rising doctors' fees is the fee-for-service system, where medical providers are reimbursed for each test, procedure, or office visit. This system incentivizes a high volume of redundant testing and overprescribing, particularly when patients have low potential for improved health outcomes. Additionally, the lack of an integrated approach in the US healthcare system leads to uncoordinated care, resulting in patients receiving duplicate tests and paying for more procedures than necessary.

The aging population is another factor contributing to rising doctors' fees. Older individuals tend to require more expensive procedures, such as knee replacements and heart bypass surgery. As the number of older Americans increases, the demand for these costly procedures rises, driving up doctors' fees.

The increase in chronic illnesses is also a significant factor. Conditions such as diabetes, high blood pressure, high cholesterol, depression, and osteoarthritis have led to increased spending on medications and treatments, with the cost of diabetes medications alone accounting for a significant portion of the rise.

Furthermore, ambulatory care costs, including outpatient hospital services and emergency room care, have increased significantly. This shift from inpatient to outpatient care was accelerated during the COVID-19 pandemic, as healthcare providers moved towards virtual services.

Another factor is the fear of malpractice lawsuits, leading to "defensive medicine" where doctors prescribe unnecessary tests or treatments to avoid potential lawsuits. This practice adds to the overall cost of healthcare and contributes to rising doctors' fees.

Lastly, the impact of inflation on the economy cannot be overlooked. Inflation affects the costs of operations, supplies, administration, and facilities. While healthcare inflation has not outpaced general inflation, specific services and items within the healthcare sector have experienced increased costs.

Understanding VA Healthcare and Insurance Billing: A Guide for Veterans

You may want to see also

Explore related products

$18.99 $19.99

![]()

Lack of competition between insurers and hospitals

The high cost of hospital bills in the US is partly due to a lack of competition between insurers and hospitals. This is a significant issue, as Americans spend more on medical care than those in other wealthy countries, and healthcare costs are increasing faster than the economy. The lack of competition in the healthcare industry has led to higher prices, with private payers often having to negotiate with each hospital and doctor, while Medicare sets the rates it will pay based on hospital costs.

One of the main reasons for the lack of competition is the consolidation of hospitals and insurance companies. Hospital systems have been consolidating rapidly, merging with other hospitals and buying up physician practices. This has resulted in higher prices, as hospitals can charge private payers more since Medicare pays less. Additionally, insurers may not be motivated to lower costs for large, self-insured company plans as they earn a percentage of the bill.

The lack of competition between insurers and hospitals has also been exacerbated by anti-competitive practices. Hospitals often write contracts that prevent insurers from informing patients about less expensive or higher-quality competitors. Similarly, dominant insurers may insist that contracting hospitals not offer their services to other payers at lower prices. These practices reduce competition and keep prices high.

To address these issues, policymakers have proposed measures such as enforcing antitrust laws and reducing barriers to entry for new competitors. However, these solutions may not be sufficient, as the underlying geography of healthcare and changes in medical technology have limited the opportunities for markets to support more competitors.

To promote competition and lower healthcare costs, policymakers should consider expanding the regulatory tools used to promote competition. For example, regulators could require hospitals to provide all insurers access to selected high-complexity services at regulated prices, while insurers could compete to win the rights to provide coverage in a given area for a specified time period. By combining regulation and competition, policymakers can help improve market efficiency and lower prices for consumers.

Maximizing Insurance Reimbursement for Vivitrol Injection: A Guide for Medical Billing Professionals

You may want to see also

Frequently asked questions

The cost of healthcare in the US is soaring due to surprise medical bills, administrative costs, rising doctors' fees, the high cost of surgical procedures and diagnostic tests, and soaring drug costs.

Pricing factors vary between hospitals and are determined by individual health, the cost of surgical procedures, operating room and post-surgical costs, X-rays and diagnostic tests, and doctor bills.

Insurance plans are a cost-sharing agreement between you and your insurance company. Many insurance companies cover the costs for preventive care throughout the year, such as check-ups and vaccinations. For other services, you may have to cover all costs until you reach a specified amount (deductible), after which the insurance company starts paying for covered services.

High deductibles and copays are a major cause of medical debt for insured individuals. Additionally, the cost of healthcare has risen significantly in recent years, leading to larger unpaid bills.

There are several strategies to lower medical bills, including negotiating with providers, seeking financial assistance, comparing costs, and choosing the right insurance plan for your needs.

![Chucks MAX Hospital Bed Pads Disposable Adult 36 x 36 Breathable Incontinence Pads - XXX-Large Pee Pads for Adults - Heavy Duty Absorbency Underpads - 400 Lbs. Patient Repositioning [20 Count]](https://m.media-amazon.com/images/I/81q9DQQ6TAL._AC_UL320_.jpg)

![White Classic Fitted Hospital Bed Sheets Set, Soft Jersey Knitted T-Shirt Quality [2 Pack]](https://m.media-amazon.com/images/I/71EMmFVj0wL._AC_UL320_.jpg)