South Carolina's insurance rates are high compared to the national average. The average cost of full coverage car insurance in the state is $118 per month, which is 39% higher than the national average. There are several reasons for this, including the state's strict requirements for minimum liability coverage, high rates of accidents, severe weather, and dense traffic in urban areas. Additionally, insurance companies in South Carolina use personal information such as age, gender, and driving record to determine premiums, with younger and male drivers often facing higher rates.

Explore related products

What You'll Learn

![]()

High accident rates

South Carolina's car insurance rates are high due to various factors, including high accident rates, strict state requirements, dense traffic, and the presence of specific insurance carriers.

South Carolina experiences a high rate of accidents, which contributes to expensive auto insurance premiums. North Charleston, for instance, has a high rate of fatal traffic accidents, with an average of 20.31 fatal car accidents per 100,000 people. Residents of North Charleston pay an average of $1,658 per year for full coverage insurance, which is significantly higher than the state average of $1,139. Similarly, Columbia, the state's capital, has a high rate of fatal car accidents, with 11.24 out of 100,000 people, resulting in higher insurance premiums for its residents.

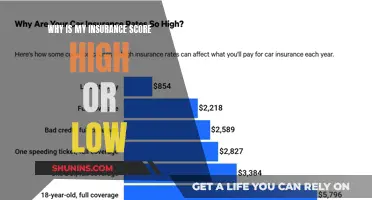

The state's frequent bumper-to-bumper traffic also increases the likelihood of crashes and subsequent insurance claims, leading to higher premiums over time. Additionally, younger and less experienced drivers contribute to the high accident rates, with 18-year-old males having the highest average premium due to their increased risk of accidents.

The probability of accidents occurring in specific areas, such as those with higher traffic congestion, is also considered by insurance companies when determining rates. As a result, drivers in these locations may experience higher insurance costs due to the increased chance of accidents.

The Impact of Claims: Navigating the Auto Insurance Landscape

You may want to see also

Explore related products

![]()

Strict minimum liability coverage requirements

South Carolina's insurance requirements are strict regarding the minimum liability coverage a driver must carry. This is a significant factor in the high cost of insurance in the state.

The state's minimum liability coverage requirements are as follows:

- Bodily injury liability coverage per person: $25,000

- Bodily injury liability coverage per accident: $50,000

- Uninsured/underinsured motorist coverage: $25,000 per person and $50,000 per accident

These requirements are relatively high compared to other states, and they contribute to the overall cost of insurance in South Carolina. The mandatory uninsured/underinsured motorist coverage is especially notable, as it is designed to protect drivers in the event of an accident with an uninsured or underinsured driver. This type of coverage is typically not required in many other states.

While these strict minimum liability coverage requirements play a role in the high insurance costs in South Carolina, it is important to remember that insurance rates are also influenced by various other factors, including an individual's driving record, age, gender, location, and credit history. Additionally, the frequency of accidents, traffic congestion, and the likelihood of severe weather events in South Carolina all contribute to higher insurance premiums.

Self-Insured Vehicles: Who Pays?

You may want to see also

Explore related products

![]()

Higher-than-average crime rates

South Carolina's insurance rates are influenced by various factors, including higher-than-average crime rates. Crime rates impact insurance costs, and South Carolina experiences higher-than-average theft and vandalism rates. For instance, Richland County's motor vehicle theft rate reached 58 thefts per 10,000 residents in 2019, significantly higher than the state average of 30.6. Consequently, drivers in Columbia, located within Richland County, pay an average of $1,144 per year for auto insurance, exceeding the state average.

Insurance companies consider theft and vandalism rates when determining premiums, as these crimes can result in costly claims. Areas with higher crime rates, particularly vehicle-related crimes, will likely face higher insurance rates. This correlation between crime rates and insurance costs is evident in South Carolina, where certain zip codes are associated with elevated premiums due to their higher incidence of theft and vandalism.

Furthermore, South Carolina's insurance costs are influenced by its stringent requirements for minimum liability coverage. The state mandates relatively high minimum liability limits, which contribute to higher insurance prices. The mandatory uninsured/underinsured motorist coverage further increases rates, as these coverages must match the liability limits. As a result, drivers in South Carolina are required to carry more extensive coverage, driving up insurance prices.

In addition to theft and vandalism, South Carolina's higher-than-average crime rates encompass accidents and traffic violations. The state experiences a high rate of fatal traffic accidents, with North Charleston averaging 20.31 fatal crashes per 100,000 people. This elevated accident rate contributes to higher insurance costs, as insurers react to frequent claims by raising premiums.

Young drivers, particularly males, face higher insurance costs in South Carolina due to their increased risk of accidents. The presence of inexperienced and young drivers on the road contributes to the state's higher-than-average accident and claim rates, influencing insurance premiums for all residents. Additionally, insurance companies consider individual factors such as age and gender when determining premiums, resulting in higher rates for specific demographics.

State Farm Auto Insurance: Maximizing Your Discounts

You may want to see also

Explore related products

![]()

Severe weather

South Carolina is no stranger to severe weather events, including windstorms, hail, and hurricanes. These weather events can cause significant damage to property, including vehicles, roofs, and windows. As a result, homeowners in South Carolina may need to purchase additional coverage to protect themselves from these risks.

Windstorm and hail coverage may not be included in standard homeowners' insurance policies in South Carolina and may need to be purchased separately. Windstorms can cause damage to roofs, siding, and windows, while hail can also cause substantial damage to property. Hailstorms are most common in South Carolina during the spring and summer months, so it is crucial for homeowners to have adequate coverage during this time.

South Carolina is also susceptible to tropical storms and hurricanes, which can result in downed trees, power outages, flooding, and property damage. The state's Department of Natural Resources data reveals that homes in South Carolina have an 86% chance of being impacted by tropical storms, leading to a higher risk of storm surges, coastal flooding, and water damage. These factors contribute to higher insurance rates in the state.

Climate change is expected to increase the severity of weather conditions, leading to more intense and frequent weather-related events. This will likely result in higher home insurance premiums in states prone to extreme weather, including South Carolina. With climate experts predicting a devastating hurricane season, home insurance costs are forecasted to surge even higher.

Digital Auto Insurance: The Future of Driving?

You may want to see also

Explore related products

![]()

Urbanization

Secondly, the cost of living is generally higher in urban areas, which also affects insurance costs. The cost of repairs, medical expenses, and vehicle replacement is typically more expensive in cities, and insurance companies factor this into their calculations when setting premiums. The higher cost of living in urban centres, such as Columbia, contributes to higher insurance rates.

Additionally, urban areas often have higher rates of theft and vandalism, which impact insurance rates. For instance, Richland County, which includes the city of Columbia, experienced a motor vehicle theft rate of 58 thefts per 10,000 residents in 2019, significantly higher than the state average. As a result, drivers in Columbia pay more for auto insurance to account for the increased risk of theft.

The concentration of people and vehicles in urban areas of South Carolina contributes to higher insurance rates. The risk of accidents, the cost of claims, and the prevalence of theft and vandalism are all factors that insurance companies consider when setting premiums. These factors collectively drive up the cost of insurance in urban centres across the state.

Door Ding: GEICO Auto Insurance Increase Explained

You may want to see also

Frequently asked questions

South Carolina car insurance rates are higher than the national average due to a variety of factors, including the high rate of accidents, the presence of insurance companies with higher premiums, and the increased cost of repairs and parts replacements. The rate of fatal car accidents in North Charleston, for example, is 20.31 per 100,000 people, which is one of the highest in the state.

Urban areas in South Carolina tend to have higher insurance rates due to the increased number of vehicles on the road, leading to a higher chance of accidents. Additionally, the cost of living and claims is typically higher in these populated cities, which further increases insurance rates.

Age is a significant factor in determining car insurance rates, with younger individuals paying more than older people. Teen drivers are considered high-risk due to their lack of driving experience, resulting in higher insurance costs. Insurance rates become more affordable once drivers reach their 20s and even more so in their 30s.

Gender plays a role in insurance costs in South Carolina, with men typically paying higher premiums than women. Statistically, men are more likely to be involved in at-fault accidents, which contributes to the higher insurance rates for males.