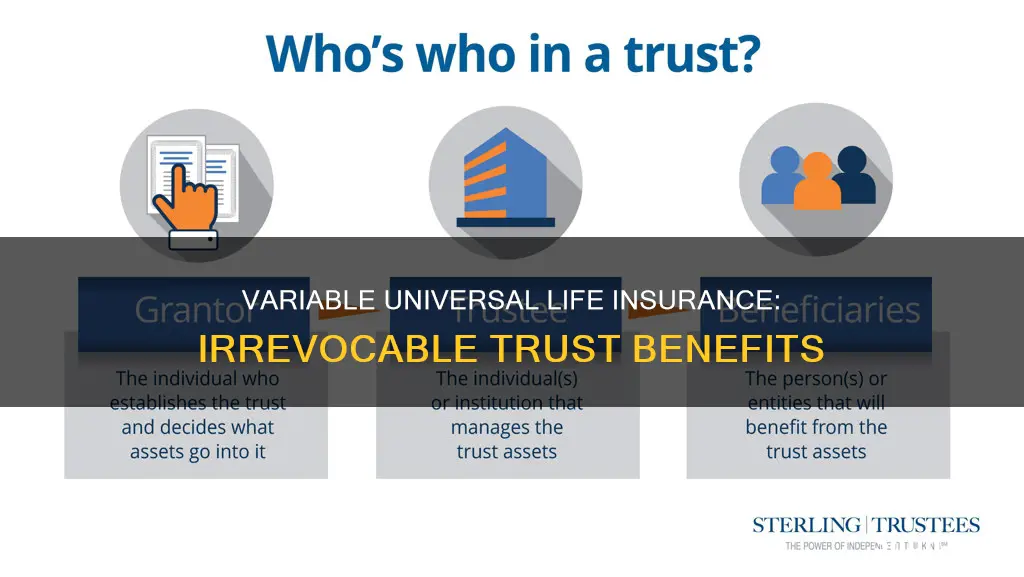

Life insurance is a crucial financial planning tool that provides heirs with assets upon the policyholder's death. One way to manage the financial complexities of passing on assets is to place a life insurance policy in an irrevocable trust. An irrevocable life insurance trust (ILIT) is a legal entity that can hold other assets and manage the distribution of proceeds to beneficiaries. It is irrevocable, meaning it cannot be altered or undone once created. By placing a life insurance policy in an ILIT, the policy is removed from the grantor's personal assets, and the payout goes directly to the trust, excluding it from the estate and reducing estate taxes. This can lead to significant tax savings when passing on assets to heirs and ensures the grantor's wishes are followed.

Explore related products

$24.95 $24.95

$8.99

What You'll Learn

![]()

Minimize estate tax

An Irrevocable Life Insurance Trust (ILIT) is a powerful tool for wealth management and estate planning. It is a legal entity that can hold assets and life insurance policies, providing several financial and legal advantages. One of its key benefits is the ability to minimize or reduce estate tax liability.

When a life insurance policy is placed within an irrevocable trust, it is effectively removed from the grantor's personal assets and becomes the property of the trust. This means that the death benefit and cash value of the policy are excluded from the grantor's estate, and thus, not subject to federal estate taxes. This can result in significant tax savings when passing on assets to heirs, as the proceeds from the death benefit are also excluded from the grantor's estate. As a result, multiple generations of the family can benefit from the trust's assets without incurring additional estate and GST taxes.

The ILIT also offers flexibility in managing and distributing the proceeds from the life insurance policy. The grantor can specify how the death benefit should be paid out and under what circumstances the beneficiaries may access their share. This allows for greater control over how the beneficiaries receive the assets and ensures that the grantor's wishes are followed. Additionally, the trustee can teach beneficiaries to use their inheritance responsibly, further enhancing the long-term financial benefits of the trust.

By utilizing annual exclusion gifting and Crummey powers of withdrawal, the grantor can gift cash to the ILIT, which can then be used to pay the premiums on the life insurance policy. This gradual reduction in the grantor's estate further minimizes potential estate tax liability. It is important to note that while the ILIT offers significant tax advantages, there may be additional tax challenges for existing policies with a large cash value.

In summary, placing variable universal life insurance in an irrevocable trust can be an effective strategy for minimizing estate taxes. It allows for the removal of the policy from the grantor's estate, provides flexibility in managing and distributing proceeds, and enables a gradual reduction in the estate through gifting strategies. However, it is essential to carefully consider the potential tax challenges and the irreversible nature of the trust before establishing an ILIT.

Life Insurance Cash Value: Is It Protected in Virginia?

You may want to see also

Explore related products

![]()

Avoid probate

An irrevocable life insurance trust (ILIT) is a powerful tool for estate planning. It is a legal entity that can hold assets, including life insurance policies, and has its own tax ID number. The main purpose of an ILIT is to reduce the tax burden on an individual's estate and ensure that their assets are distributed according to their wishes.

When an individual owns a life insurance policy, the payout to the beneficiaries is typically income tax-free. However, the payout may be subject to estate tax. By placing a life insurance policy inside an ILIT, the payout is made to the trust, thus reducing the value of the individual's estate and the associated estate tax liability. This can result in significant tax savings when passing on assets to heirs.

In addition to tax benefits, an ILIT provides control over how the proceeds are distributed. For example, if the beneficiary is incapacitated at the time of the individual's death, a court may appoint a guardian to manage the proceeds. With an ILIT, the trustee can directly provide for the beneficiary without court interference. An ILIT also adds privacy to the estate settlement process, as trusts do not require public probate approval by a judge.

It is important to note that an ILIT is generally irreversible. Once established, the grantor cannot amend or cancel it, and they lose control over the underlying insurance policy. Therefore, it is recommended to consult a professional before creating an ILIT to fully understand the legal and tax implications.

Life Insurance Proceeds: Criminal Restitution Entanglement

You may want to see also

Explore related products

![]()

Protect assets

Life insurance is an important financial planning tool that can protect loved ones and bring peace of mind and financial benefits. An irrevocable life insurance trust (ILIT) is a powerful estate planning vehicle that can be used in tandem with a life insurance policy to manage financial issues around life insurance assets and benefits.

An ILIT is its own legal entity with a separate tax ID number and can hold other assets, such as cash, stocks, bonds, and other investments. The main purpose of an ILIT is to reduce the value of an individual's estate, thereby minimising estate tax liability. By placing a life insurance policy in an ILIT, the policy is removed from the grantor's personal assets, and the payout goes to the trust, excluding it from the estate. This can lead to major tax savings when passing on assets to heirs, as the proceeds from the death benefit are excluded from the grantor's estate.

In addition to tax benefits, an ILIT can provide privacy and control over how the proceeds are distributed. The grantor can specify how the death benefit should be paid out and under what circumstances the beneficiaries may access their share of the proceeds. This can help ensure that young heirs do not squander their inheritance and that the grantor's wishes are followed. An ILIT can also protect assets from creditors and legal action, and it bypasses the often lengthy and burdensome probate process that ordinary wills are subjected to.

It is important to consider the drawbacks of an ILIT. Establishing an ILIT requires the grantor to give up all rights to the property in the trust, including who the beneficiaries are and how they receive the assets. This means that the grantor may not have access to the cash value of a whole life policy, which could otherwise be used for retirement or other expenses. Additionally, setting up and maintaining an ILIT may incur professional fees and filing a gift tax return.

Life Insurance: Deciding Your Dollar Amount Coverage

You may want to see also

Explore related products

![]()

Control distribution

ILITs can also be used to control distribution in the case of a beneficiary who is incapacitated or receiving government aid. If a beneficiary is incapacitated, the court may require the appointment of a guardian or conservator to manage the proceeds on their behalf. However, if an ILIT is the beneficiary of the policy, the trustee can use the proceeds to provide for the beneficiary directly, without court interference. If a beneficiary is receiving government aid, such as Social Security Disability Income or Medicaid, the trustee can carefully control how distributions from the trust are used so as not to interfere with the beneficiary's eligibility to receive government benefits.

ILITs can also be used to control distribution to multiple generations of the family. Since the proceeds from the death benefit are excluded from the grantor's estate, multiple generations of the family—children, grandchildren, and great-grandchildren—may benefit from the trust's assets free of estate and generation-skipping transfer (GST) tax.

Understanding Life Insurance: Payor Benefit Rider

You may want to see also

Explore related products

![]()

Provide for heirs

Life insurance is one of the most important long-term financial planning tools. It can be a great way to provide financial support for loved ones after you're gone. One solution is to purchase a life insurance policy that provides your heirs with assets upon your death.

Variable universal life insurance is a form of permanent life insurance that carries a cash value. It offers more flexibility on when premiums are paid and how the cash value accumulates. The biggest differentiator is that the cash value can be invested in a variety of subaccounts, similar to mutual funds, allowing you to invest in different areas of the market.

An irrevocable life insurance trust (ILIT) is a powerful estate planning vehicle that can be used in tandem with a life insurance policy to manage financial issues and provide for your heirs. It is a trust created during the insured's lifetime that owns and controls a term or permanent life insurance policy. The trust can also manage and distribute the proceeds that are paid out upon the insured’s death, according to the insured's wishes.

One of the main benefits of an ILIT is that it can help minimize estate taxes. By placing a life insurance policy in an irrevocable trust, you can remove it from your personal assets. This means that if you pass away and the policy pays out a substantial amount, the payout goes to the trust, excluding it from your estate. This can result in significant tax savings when passing on assets to heirs. Additionally, the trust can ensure that a young heir doesn't squander their inheritance, as the trustee is responsible for managing payouts and ensuring the grantor's wishes are followed.

Another advantage of an ILIT is that it provides privacy. Unlike a traditional will, trusts do not have to be approved through the public probate process by a judge. This can add an extra layer of privacy to your estate settlement.

While an ILIT can be a powerful tool, it's important to consider the downsides. Once the trust is finalized, it generally cannot be altered or undone. This means that if you put assets into the trust for your heirs and later need those assets yourself, you will not be able to access them.

Overall, an irrevocable life insurance trust can be an effective way to provide for your heirs, minimize taxes, and ensure your wishes are carried out. However, it's important to carefully consider your options and seek professional advice before making any decisions.

Life Insurance: Sensible or Not?

You may want to see also

Frequently asked questions

Variable universal life insurance can be placed in an irrevocable trust to avoid the probate process and reduce the size of your estate, thereby minimising any estate tax liability.

An irrevocable trust is a legal entity that owns and controls a term or permanent life insurance policy. It is created by a grantor during their lifetime and cannot be amended or cancelled once established.

An irrevocable trust owns the insurance policy, so it can be excluded from your taxable estate and therefore not subject to federal estate taxes. The trust can also manage and distribute the proceeds that are paid out according to the insured's wishes.