In health insurance, a dependent is someone who is eligible to be added to a policyholder's insurance coverage. The policyholder is the individual who has primary eligibility for coverage, such as an employee whose employer offers health insurance benefits. Dependents can receive the benefits of the policyholder's health insurance plan and use it in much the same way. Typically, dependents include the policyholder's spouse, children, and sometimes other relatives.

| Characteristics | Values |

|---|---|

| Definition | A dependent is a person who is eligible to be added to a policyholder’s health insurance coverage |

| Who can be a dependent? | Biological, adopted, and stepchildren; in some cases, a grandchild, an adult child with a disability, a foster child or someone for whom the policyholder is the legal guardian; a spouse, domestic partner, or other relative |

| Age limit | Children can be covered up to the age of 26; if the child is disabled, they may be covered beyond this age |

| Relationship to policyholder | The dependent must have a defined relationship with the policyholder, who must provide over half of their financial support |

| Residency requirements | A child must have lived with the policyholder for at least six months to qualify as a dependent |

| Income contribution | A child's income must be less than half of the cost of their support expenses to qualify as a dependent |

| Tax filing | A child cannot be claimed as a dependent if they file a joint tax return |

| Other claims | A child cannot be claimed as a dependent by more than one household |

| Additional considerations | The dependent must meet the qualifications set out by the healthcare provider, state law, and federal law; in most states, parents cannot be added as dependents, but this is allowed in California |

Explore related products

What You'll Learn

![]()

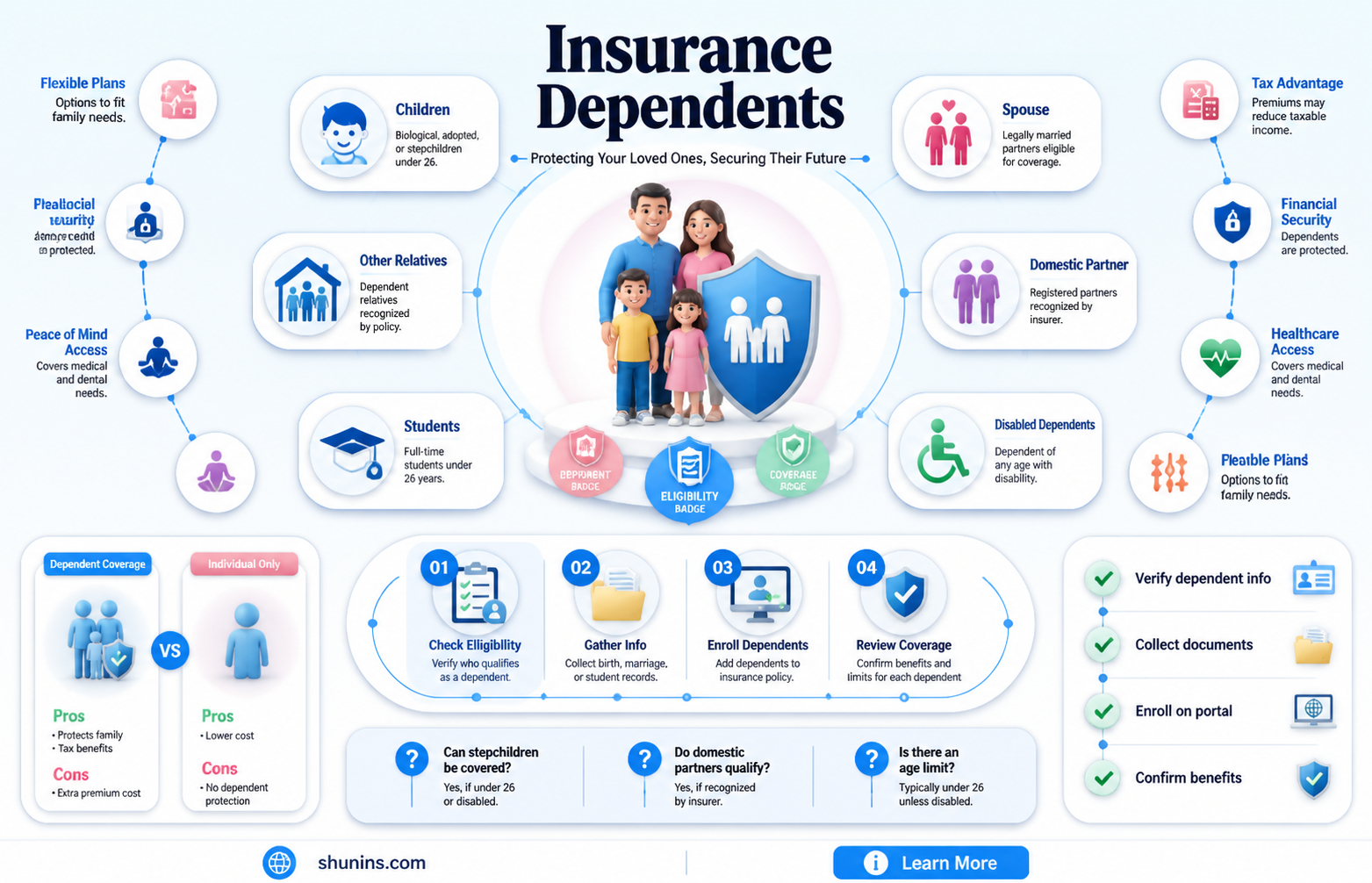

Who can be added as a dependent?

When you purchase a health insurance plan, you can extend coverage to your dependents. A dependent is a person who is eligible to be added to a policyholder's health insurance coverage. The policyholder is the individual who has primary eligibility for coverage, such as an employee whose employer offers health insurance benefits.

The people you can add as a dependent will depend on the terms of your policy and the type of policy you have. However, in general, the following people can be added as dependents:

- Spouse: Your current spouse is often eligible to be added as a dependent. This includes same-sex spouses. However, once a marriage is legally ended through divorce, the ex-spouse is no longer considered a dependent.

- Children: Biological children, stepchildren, adoptive children, and foster children are all normally considered dependents, as long as they meet age and other eligibility criteria. Generally, insurance coverage for dependent children extends until they reach the age of 26, or until they no longer financially depend on you.

- Domestic partners: Certain health insurance policies provide coverage for domestic partners or same-sex partners, acknowledging them as eligible dependents.

- Parents: In most instances, you won’t be allowed to add your parents to your health insurance. However, there are exceptions. For example, if you can claim your parents as your tax dependents, or if you have legal guardianship of your parents, some providers may allow you to add them as dependents.

- Siblings: You ordinarily won't be able to claim your siblings as dependents. However, if you have legal guardianship of your minor sibling, or if your sibling has a medical condition that makes them reliant on you, some providers may let you add them as a dependent.

- Non-family members: Non-family members cannot usually be added to your health insurance plan. However, some states recognize civil unions as a legal relationship, permitting partners in these unions to be added as dependents. Additionally, insurance providers might make special exceptions for well-documented and compelling circumstances, such as if you have legal guardianship of a non-family member.

To add a dependent to your health insurance plan, you will typically need to provide the following information:

- Proof of relationship: This could include a birth certificate for biological children, a marriage certificate for a spouse, or an adoption certificate for legally adopted children.

- Enrollment or change form: The insurance company typically requires you to complete this form to add a dependent.

- Social Security card and birth certificate: When adding a dependent, you may need to provide a copy of their Social Security card and their birth certificate.

- Affidavit: Some carriers may require you to sign and submit an affidavit confirming your relationship to the person you’re adding to your plan.

Name Change: Navigating the Insurance Paperwork

You may want to see also

Explore related products

![]()

What is the eligibility criteria for a dependent?

To be eligible for dependent health insurance, an individual must meet the criteria set by the insurance provider and the terms of the policy. While the criteria vary across providers, there are some general guidelines that determine eligibility for dependent health insurance. Here are the key factors to consider:

Spouse

A current spouse is often eligible for dependent health insurance. However, this typically does not include ex-spouses. Once a marriage is legally terminated through divorce, the ex-spouse is no longer considered a dependent. In most cases, you have up to 60 days after getting married to add your spouse as a dependent. It is important to note that if you or your spouse have access to employer-sponsored health insurance but choose to buy your own family plan, you may not qualify for certain subsidies.

Children

Biological children, adoptive children, stepchildren, and foster children are generally considered eligible dependents. The coverage for dependent children usually extends until they reach the age of 26, unless they are disabled, in which case coverage may continue beyond that age. The length of residency is also a factor, with a child typically needing to have lived with the policyholder for at least six months to qualify as a dependent. Additionally, the child's income contribution should be considered. Their income must not exceed half of their support expenses to qualify as a dependent.

Domestic Partners

Certain health insurance policies provide coverage for domestic partners or same-sex partners, recognising them as eligible dependents. This may include common-law spouses if the marriage is legally recognised by the jurisdiction. However, it is important to note that if your plan does not cover other adult dependents, a domestic partner may not be considered a dependent.

Other Adult Dependents

Adult dependents, such as elderly parents or other relatives, may be eligible for dependent health insurance in certain circumstances. They typically need to live with the policyholder, be financially dependent on them, and be unmarried. Additionally, they should not be named as a dependent by anyone else, and their gross annual income should fall below a certain threshold, such as $3,000.

Special Circumstances

There may be exceptions to the general eligibility criteria for dependents. For example, if you have legal guardianship of a parent, sibling, or non-family member due to incapacitation or other reasons, they may be considered a dependent. Additionally, if your sibling or parent has a medical condition or other extenuating circumstances that render them financially or medically reliant on you, some insurance providers may allow them to be added as dependents.

It is important to carefully review the specific criteria and requirements outlined by your insurance provider and consult with them or your employer's human resources department to determine eligibility for dependent health insurance coverage.

Unraveling the Complexities of Insurer Annual Billing: Maximum Charges and Their Implications

You may want to see also

Explore related products

![]()

What is the cost of adding a dependent?

The cost of adding a dependent to your health insurance plan will depend on the insurance provider and the type of plan you have. Typically, adding a dependent will increase your monthly premium costs.

If you were the only person covered by your insurance plan, you will likely have to switch from an individual plan to a family plan. A family plan covers you and other individuals, including your spouse, your dependents, or both.

The cost of adding a dependent to your health insurance plan can also be understood in terms of copays, coinsurance, and deductibles. Copays and coinsurance may apply to each covered service or medication received by a covered individual. Many family plans have both an individual deductible and a family deductible. Family deductibles are often twice the amount of individual deductibles.

When a covered person pays a deductible, the amount is applied to both their individual and family deductible amount. If an individual meets their deductible but the family deductible has not been met, the policy begins to pay for that individual's healthcare expenses. Once the family deductible is met, the policy pays benefits for each family member, even if they have not met their individual deductibles. Annual out-of-pocket maximums typically work in the same way.

In addition to the cost of adding a dependent to your health insurance plan, it is important to consider the potential costs of not having insurance for your dependent. An emergency room visit can cost more than $1,500, and this does not include the cost of any necessary follow-up treatments. While there is an additional cost to cover additional people, the benefits may be well worth it.

It is also important to note that while health insurance is no longer federally mandatory for yourself and your dependents, some states still have their own health coverage requirements for residents.

Understanding Insurance Billing: A Look at the Timing of Your Premium Payments

You may want to see also

![]()

Can parents be added as dependents?

Yes, it is possible to claim your parents as dependents on your tax return. This is particularly relevant for those who are caring for an elderly parent or paying for their care.

There are several criteria that must be met in order to claim a parent as a dependent. These include:

- The parent must be a relative (this includes in-laws and stepparents).

- The parent must be a citizen, national, or resident alien of the United States, or a resident of Canada or Mexico.

- The parent must not have filed a joint tax return (unless it is solely for a refund).

- The parent's gross income must not be above a certain threshold (for 2023, this amount was $4,700, and for 2024, it is $5,050). Social Security payments are usually not counted towards this, but there are exceptions.

- You must provide over half of their support during the tax year. This includes food, lodging, clothing, education, medical and dental care, and transportation.

- You cannot be a dependent of another taxpayer.

- The parent cannot be a qualifying child of another taxpayer.

If you are not able to claim your parent as a dependent, you may still be able to deduct any medical expenses you paid for them from your taxes.

Claiming a parent as a dependent can provide tax benefits, such as tax credits and deductions, which can reduce your taxable income. However, it is important to note that your parents may not be eligible for certain tax benefits or assistance programs if they are claimed as dependents.

Warby Parker's Insurance Billing: Understanding the Process and Its Benefits

You may want to see also

![]()

What is the impact of divorce on dependent coverage?

Divorce can have significant implications for dependent coverage, and it's important to understand the options available to ensure continuous health coverage for those involved. Here's a detailed overview:

Impact on Spousal Coverage

In the event of a divorce, an ex-spouse generally loses their eligibility to be covered as a dependent under their partner's health insurance plan. They will need to obtain their own coverage, potentially through options like COBRA, the health insurance marketplace, or an individual policy with their previous carrier. This change in coverage typically occurs once the divorce is finalised, though there may be a brief extension of coverage, as seen in federal employee plans.

Impact on Children's Coverage

The impact of divorce on dependent coverage for children is a crucial aspect. Both federal and state laws require parents to provide healthcare coverage for their dependent children. While divorce may alter the specifics of this coverage, children can still be covered as dependents by either parent's plan, regardless of the divorce. The custody agreement or divorce decree may outline the specifics of this arrangement.

Court Orders and Financial Support

Family law courts play a significant role in determining how healthcare costs are managed post-divorce. Courts may require non-custodial parents who are employed to maintain their children on their employer-provided health insurance plan. If private insurance is unaffordable, state programs like Medicaid or CHIP may provide coverage for the children. Courts can also order the division of out-of-pocket costs, including co-pays, deductibles, and non-covered expenses, based on each parent's financial situation.

Impact of the Affordable Care Act (ACA)

The ACA has brought about notable changes that impact dependent coverage in the context of divorce. Firstly, it allows young adults to remain on their parents' health insurance plans until the age of 26, providing essential healthcare services during transitional periods. Secondly, the ACA prohibits plans from denying coverage or charging higher premiums for pre-existing conditions, ensuring that dependents cannot be discriminated against when seeking coverage under a family plan.

Special Enrollment Periods (SEP)

While divorce typically doesn't trigger an SEP unless there's an associated loss of coverage, some state-run exchanges have implemented an SEP for situations involving divorce. This allows individuals to make changes to their health insurance plans, such as enrolling in a different plan or changing coverage options. It's important to note that the availability of this option varies by state and specific requirements and timeframes may apply.

In summary, divorce can significantly impact dependent coverage for both spouses and children. It's crucial for individuals going through a divorce to understand their options, rights, and responsibilities regarding health insurance to ensure continuous coverage for themselves and their dependents.

Maximizing Orthotics Reimbursement: Navigating the Insurance Billing Maze

You may want to see also

Frequently asked questions

A dependent is a person who is eligible to be added to a policyholder's insurance coverage. This typically includes a spouse, domestic partner, and children. Children can be biological, adopted, stepchildren, or foster children. In some cases, you may also be able to cover a grandchild, an adult child with a disability, or someone for whom you are the legal guardian.

Yes, generally, insurance coverage for dependent children extends until they reach the age of 26, or until they are no longer financially dependent on the policyholder.

In most cases, you won't be allowed to add your parents as dependents. Typically, health plans consider only spouses and children as dependents. However, there may be exceptions, such as if you have legal guardianship of your parents or if they have special needs or disabilities that make them reliant on you.