Accidental Death and Dismemberment (AD&D) insurance is a supplemental insurance policy that provides financial protection in the event of accidental death or serious injury. It is often offered as an employee benefit and can be extended to cover spouses and dependent children. In the case of accidental death, the beneficiary, typically the spouse, receives a payout, while the insured individual receives compensation for serious injuries such as loss of limb or paralysis. This insurance is not a substitute for comprehensive life insurance but offers additional financial security in the event of unforeseen accidents.

| Characteristics | Values |

|---|---|

| What is AD&D insurance? | Accidental Death and Dismemberment insurance that combines two types of coverage: an accidental death policy and a dismemberment policy. |

| Who is the beneficiary? | The beneficiary of your AD&D policy (such as your spouse) collects the money in the event of your accidental death. |

| What does AD&D insurance cover? | AD&D insurance covers incidents that cannot be foreseen, such as falls, traffic accidents, homicides, drowning, and accidents involving heavy equipment. |

| What are the payouts? | If you die in an accident, your beneficiary will receive a full payout of the face value of your AD&D policy. For injuries, covered dismemberments vary between insurers and payouts are linked to the severity of the injury. |

| How much does it cost? | The cost of AD&D insurance depends on the amount of coverage you select and is usually paid on an after-tax basis. If offered through an employer, it may cost less than 10 cents a month for every $1,000 of coverage. |

| Where can I get AD&D insurance? | You can get AD&D insurance through your employer as part of their benefits package, or you can buy standalone policies directly from insurers, banks, or credit unions. |

| Can I add my spouse to my AD&D insurance? | Yes, you can add your spouse or dependent children to your AD&D insurance policy. |

Explore related products

What You'll Learn

- AD&D insurance covers accidental death and dismemberment

- Dismemberment includes loss of limbs, sight, speech, or hearing

- The beneficiary receives a payout if the policyholder dies accidentally

- AD&D insurance is supplemental and not a substitute for life insurance

- Employers may offer AD&D insurance as part of their benefits package

![]()

AD&D insurance covers accidental death and dismemberment

AD&D insurance, or Accidental Death and Dismemberment insurance, is a supplemental insurance policy that covers accidental death and dismemberment. It is typically added as a rider to a health or life insurance plan, but it can also be purchased as a standalone policy. This type of insurance provides financial protection in the event of an accidental death or serious injury, such as the loss of a limb or the loss of function in a body part.

Accidental death and dismemberment insurance is designed to help cover the financial strain that can result from an accident, including treatment, rehabilitation, and end-of-life expenses. It is important to note that AD&D insurance only covers accidental deaths and injuries, and not all causes of death or dismemberment may be included. For example, natural causes, illnesses, and certain specific causes of death, such as overdoses, may be excluded.

The beneficiary of an AD&D policy, such as a spouse, will receive a payout in the case of an accidental death. The policyholder will receive a payout if they suffer a covered injury. Payouts for injuries are typically linked to the severity of the injury, with higher payouts for more severe losses. AD&D insurance can be obtained through an employer as a workplace benefit or purchased individually through an insurer, bank, or credit union. It is also worth noting that AD&D insurance does not replace life insurance, as it does not cover deaths from natural causes or illnesses.

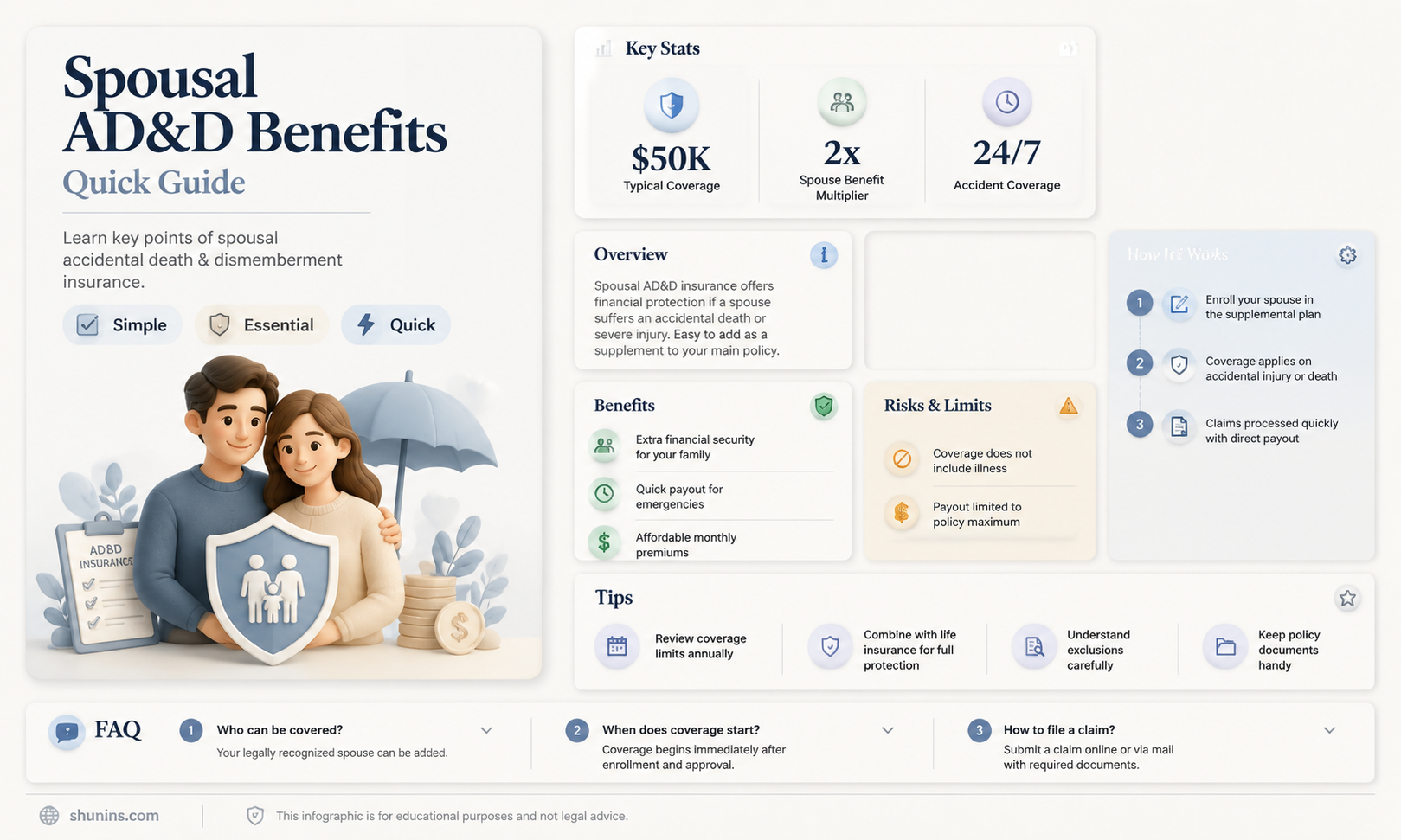

In terms of spousal benefits, AD&D insurance can provide coverage for a spouse if the employee or policyholder has also enrolled in AD&D insurance. In some cases, there may be maximum coverage amounts for spousal AD&D insurance, such as a percentage of the employee's coverage amount. Additionally, there may be requirements for the employee to be actively at work to apply for or increase coverage. It is important to carefully review the specific terms and conditions of the AD&D insurance policy to understand the spousal benefits and any applicable limitations.

Banner Life Insurance: Is It Worth the Hype?

You may want to see also

Explore related products

![]()

Dismemberment includes loss of limbs, sight, speech, or hearing

Accidental death and dismemberment (AD&D) insurance is a category of life insurance that pays out a death benefit when the insured dies in a covered accident or suffers specific serious injuries, such as dismemberment. Dismemberment includes the loss or loss of use of body parts or functions, such as limbs, speech, eyesight, and hearing.

AD&D insurance is typically purchased by those in high-risk occupations or hobbies where physical injury is a possibility. It is often added as a rider to a life insurance policy to provide additional coverage for accidents. The extent of injuries covered varies by insurer and policy, so it is important to carefully read the terms of the policy.

In the case of dismemberment, AD&D insurance generally pays the beneficiary a percentage of the value of the policy for each covered injury. For example, losing one body part, such as a finger, hand, foot, limb, or sight in one eye, may result in a 25% to 50% payout. Losing two body parts typically leads to a full payout. For paralysis, most insurers offer a full payout for quadriplegia and a 50% payout for paraplegia.

Spouses are often eligible to be beneficiaries of AD&D insurance policies and can also be enrolled in their own AD&D coverage, depending on the insurer. It is important to note that AD&D insurance does not cover natural causes or illnesses and is not a substitute for full life insurance.

Understanding Life Insurance Agents: Are They Fiduciaries?

You may want to see also

Explore related products

![]()

The beneficiary receives a payout if the policyholder dies accidentally

Accidental Death and Dismemberment (AD&D) insurance is a type of insurance that combines two types of coverage: an accidental death policy and a dismemberment policy. The beneficiary of an AD&D policy will receive a payout if the policyholder dies accidentally. The death must be the direct result of an accident, and natural causes or terminal illnesses are not covered. For example, if the policyholder has a heart attack while driving and gets into a fatal car crash, the beneficiary will not receive any money.

AD&D insurance is often offered as part of an employee benefits package, and employees may have the option to add their spouse or children to the policy. It can also be purchased as a standalone policy directly from insurers or through financial institutions. If offered by an employer at no charge, it is generally recommended to opt into this benefit. Otherwise, purchasing a standalone policy may be worth considering for individuals with risky jobs or hobbies.

The beneficiary of an AD&D policy is typically the spouse or adult child of the policyholder. However, it is the policyholder's responsibility to choose their beneficiary, and they may also select a charity or other entity as the beneficiary. It is important to note that the beneficiary should be aware of the policy and understand what is needed to receive the payout. In the case of the policyholder's accidental death, the beneficiary will need to contact the insurer and initiate the claims process by providing a death certificate and any other necessary documentation.

The payout from an AD&D policy is typically a lump sum, but some policies may offer alternative options such as installment payments or an annuity. The amount of the payout depends on the coverage amount selected by the policyholder. In the case of partial or full dismemberment, such as the loss of a limb or finger, the policyholder themselves may receive a partial or full payout, depending on the severity of the injury.

Get an A-Max Insurance Quote Today

You may want to see also

Explore related products

![]()

AD&D insurance is supplemental and not a substitute for life insurance

Accidental Death and Dismemberment (AD&D) insurance is supplemental life insurance and not an acceptable substitute for a full life insurance policy. AD&D insurance is limited and generally covers unlikely events. It only pays out in the event of accidental death or dismemberment, whereas standard life insurance has an all-cause death benefit.

AD&D insurance is designed to pay benefits for accidental deaths and dismemberments only. It covers death and injuries resulting from accidents. The exact circumstances under which your AD&D coverage applies are specified in your policy, but you're generally covered for accidental death and murder. However, there are many causes of death and injury that may not be covered, including death from natural causes or terminal illness.

Standard life insurance, on the other hand, pays out upon the insured's death no matter the cause, except for certain exclusions noted in the policy. This is known as an "all-cause" death benefit. It covers most causes of death but does not cover non-fatal injuries.

If you already have life insurance and are concerned about covering the costs of a serious accidental injury, it can make sense to supplement your life insurance with an AD&D standalone policy. Adding an AD&D rider to a standard life insurance policy can increase the payout loved ones receive in the event of accidental death. This rider typically doubles the payout of your life insurance policy if you die in an accident and is also known as a "double indemnity" rider.

Therefore, AD&D insurance is supplemental and not a substitute for life insurance. If you're concerned about accidents, it can be a valuable addition to your standard life insurance policy.

Life Insurance and Debt: Can Garnishments Be Withheld?

You may want to see also

Explore related products

![]()

Employers may offer AD&D insurance as part of their benefits package

AD&D insurance is a combination of accidental death and dismemberment insurance. It pays out in the event of death due to an accident and also in the event of serious injuries such as losing a limb, becoming paralysed, or losing your sight, speech or hearing.

Many employers offer AD&D insurance as part of their benefits package. This is sometimes referred to as voluntary insurance. The insurance is often inexpensive for employers to provide, and can be offered at no charge to employees. It is worth noting that AD&D insurance is not a replacement for life insurance, as it does not cover death by natural causes or terminal illness. It is also important to be aware that if you get AD&D insurance through your employer, you may lose the insurance if you change jobs.

If your employer offers AD&D insurance, they may give you the option to add your spouse or children to the policy. This is known as Dependent Supplemental AD&D insurance coverage. To enrol your dependents, you must also elect AD&D coverage for yourself. Your employer may also allow you to add an AD&D rider to your individual life insurance policy for an additional premium. This would mean that your beneficiaries would receive an additional lump-sum payout if you died in an accident.

If you are considering enrolling in your employer's AD&D insurance, it is important to understand the details of the policy. AD&D insurance policies differ from company to company, and it is important to know what is and isn't included. For example, some policies do not cover risky activities such as skydiving, and medical events like heart attacks and strokes are often not covered.

Statutory Life Insurance: Understanding the Basics of This Fund

You may want to see also

Frequently asked questions

Accidental Death and Dismemberment insurance combines two types of coverage: an accidental death policy and a dismemberment policy.

AD&D insurance covers death only in certain circumstances, such as exposure to the elements, traffic accidents, homicide, falls, drowning, and accidents involving heavy equipment. It also covers loss of limb(s), sight or hearing, or a combination of more than one loss.

The beneficiary of your AD&D policy, such as your spouse, collects the money in the case of your accidental death. You can also have more than one beneficiary at a time.

Yes, you can purchase AD&D insurance for your spouse or registered domestic partner. To enroll your dependents, you must also elect AD&D coverage for yourself.

No, you may not elect coverage as an employee and receive coverage as another employee's dependent.