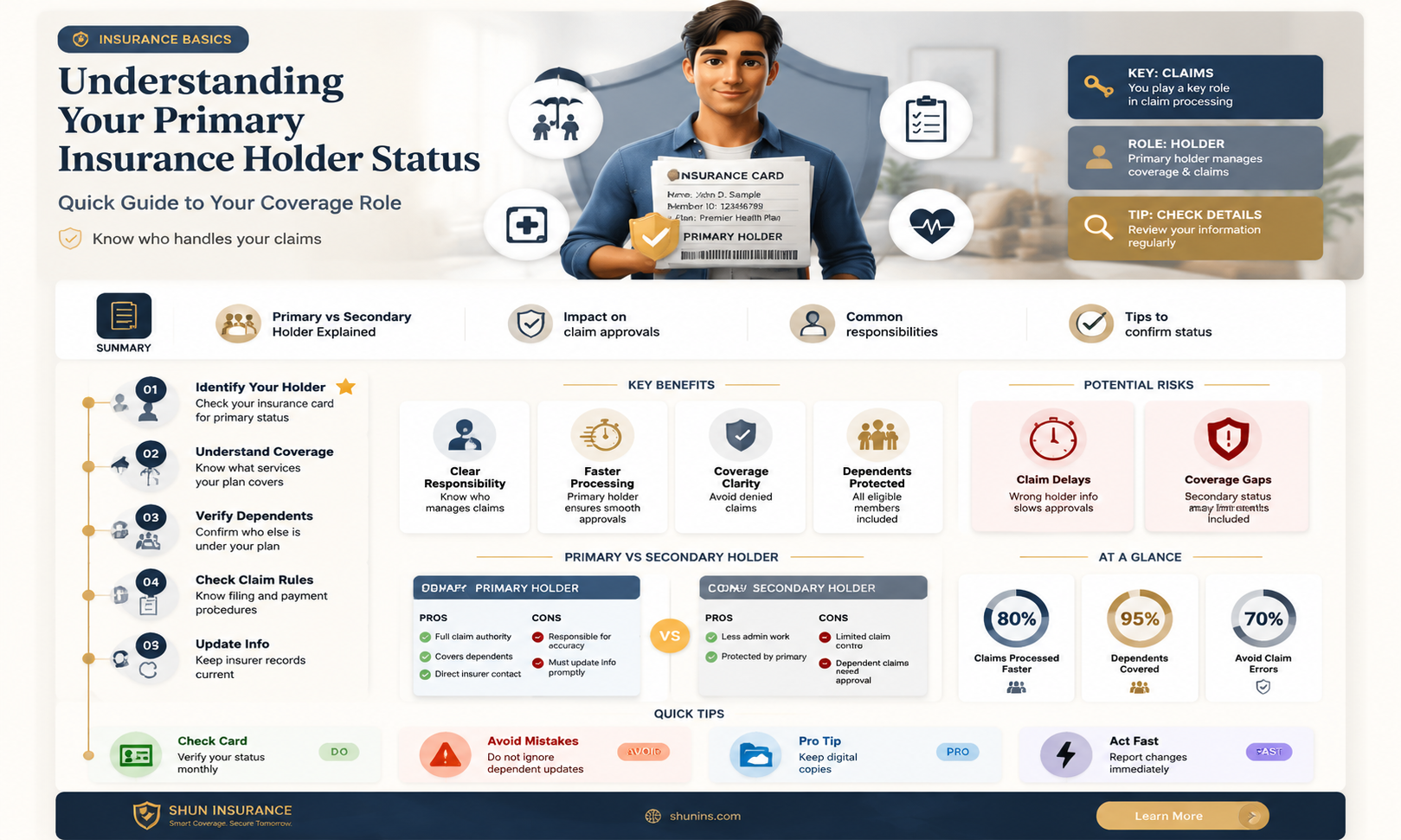

The primary insured is the main person on an insurance policy. This person is responsible for paying the premium, which is the monthly cost charged by the insurance provider. They are also the only ones who can alter the policy, such as by changing the beneficiaries or adding insured individuals. The primary insured can be the policyholder, subscriber, or member. The policyholder is the person who has purchased and owns the insurance policy, while the subscriber is the one who pays the premiums. In the case of employer-sponsored insurance, the employer is usually the policyholder, and the employee is the subscriber. The primary insured has the flexibility to make choices, such as adding secondary insured individuals, changing their plan, or keeping their login information private.

| Characteristics | Values |

|---|---|

| Definition | A primary insurance holder is the person who has purchased and owns an insurance policy. |

| Other names | Policyholder, subscriber |

| Who can be a primary insurance holder? | An individual, a spouse, an employer |

| Who is covered? | The primary insurance holder is also often the insured. Immediate family members are often covered by default under auto insurance, renters insurance, and homeowners insurance. |

| What does a primary insurance holder do? | The primary insurance holder is responsible for paying the premium, altering the policy, and adding insured individuals. |

| Primary insurance vs. secondary insurance | Primary insurance is billed first when receiving healthcare. Secondary insurance is a health insurance plan that covers you on top of your primary insurance plan. |

Explore related products

![ESSENTIAL Car Auto Insurance Registration BLACK Document Wallet Holders 2 Pack - [BUNDLE, 2pcs] - Automobile, Motorcycle, Truck, Trailer Vinyl ID Holder & Visor Storage - Strong Closure On Each -](https://m.media-amazon.com/images/I/61px7jy3NmL._AC_UL320_.jpg)

What You'll Learn

- The primary insured is the main person on the policy

- The primary insurance holder is responsible for paying the premium

- The primary insurance holder can add people to the policy

- Secondary insurance takes effect when primary insurance is exhausted

- The primary insurance holder can change the beneficiaries

![]()

The primary insured is the main person on the policy

The primary insured person is the main individual on an insurance policy. They are responsible for paying the premium, which is the monthly cost charged by the insurance provider. The primary insured has control over the policy and can make changes such as adding insured individuals or changing beneficiaries. This means that the primary insured can decide if they want to include family members on their insurance account. For example, under auto insurance, renters insurance, and homeowners insurance, spouses, children, and parents are often covered by default. However, in the case of renters insurance, roommates are not considered insured and would need to be added to the policy for a fee or purchase their own plans.

In the context of life insurance, the policyholder is often the insured, but they may also purchase a policy for a loved one, such as a spouse. In this case, the policyholder retains control over the policy and can add beneficiaries. With employer-provided insurance, the employer may be considered the ultimate policyholder, while the employee is the insured or subscriber.

It is important to distinguish between primary and secondary insurance, especially when it comes to health insurance. Most people have a primary insurance plan, but not everyone needs a secondary plan. Primary insurance is typically billed first when receiving healthcare, and it covers an individual as an employee, subscriber, or member. On the other hand, secondary insurance takes effect when the primary insurance is exhausted and helps cover additional healthcare costs. For instance, if an individual already has insurance through their employer and enrols in their spouse's insurance plan, the latter becomes their secondary insurance.

Life Insurance and Suicide: What Families Need to Know

You may want to see also

Explore related products

![]()

The primary insurance holder is responsible for paying the premium

A policyholder is the person who has purchased and owns an insurance policy. If you purchased a policy from an insurance provider, that makes you the policyholder. As the policyholder, you're responsible for paying the premium—the monthly cost the provider charges for their insurance policies. Your name is on the account, so you'll be the one receiving the bill.

With many types of coverage, "insured" can refer to the policyholder and their immediate family members. For example, spouses, children, and parents are often covered by default under auto insurance, renters insurance, and homeowners insurance. In the case of life insurance, the policyholder is often also the insured. However, many people take out a life insurance policy to cover a loved one. For example, a person may purchase a life insurance policy for their spouse, who would be listed as the insured. In this case, the policyholder retains control over the policy and is responsible for paying the premium.

Similarly, auto insurance often covers the policyholder and their passengers while they are driving. Additional drivers can be added to the policy for a fee, but the policyholder is still responsible for paying the premium. Renters insurance typically covers only the policyholder and their immediate family living under the same roof. Roommates are not considered "insured" and would need to be added to the policy or purchase their own plans.

In some cases, an employer may be the policyholder for insurance provided as a benefit to employees. In this case, the employer is responsible for paying the premiums. However, when an individual enrols in insurance through their employer, they become the "insured" and have certain rights and benefits associated with the policy.

Life Insurance and Divorce: What's the Verdict?

You may want to see also

Explore related products

![]()

The primary insurance holder can add people to the policy

A policyholder is the person who has purchased and owns an insurance policy. If you purchased a policy from an insurance provider, you are the policyholder. This means you are responsible for paying the premium, which is the monthly cost charged by the provider. Your name is on the account, so you will receive the bill. Being the policyholder also means that you have control over the policy. You are the only one who can make changes to the policy, such as adding or removing people.

The primary insured, or primary insurance holder, is the main person on the policy. As the primary insured, you can add people to the policy as secondary insured individuals. This allows you to include family members or loved ones on your insurance policy. It is a simple process of adding them to the policy, after which they can start using your insurance. As the primary insured, you have flexibility and can make choices, such as deciding who to add as a secondary insured or keeping your login information private.

In some cases, the policyholder may not be the same as the primary insured. For example, in life insurance, the policyholder may purchase a policy for a loved one, such as a spouse. In this case, the policyholder retains control over the policy, but the insured person is the primary beneficiary. Similarly, with renters' insurance, only the policyholder and their immediate family living in the same residence are typically covered. Roommates would need to be added to the policy or purchase their own insurance plans.

It is important to understand the distinction between the policyholder and the insured, as well as the different types of insurance and their coverage. As the primary insured or policyholder, you have the flexibility to make changes and add people to your policy to ensure that your loved ones are covered. By staying in contact with your insurance provider and asking questions, you can feel confident about your insurance choices and coverage.

Huntington's Disease: Life Insurance Coverage and Exclusions

You may want to see also

Explore related products

![]()

Secondary insurance takes effect when primary insurance is exhausted

The policyholder is the person who has purchased and owns an insurance policy. This person is responsible for paying the premium, which is the monthly cost charged by the provider. The policyholder's name is on the account, and they have control over the policy. They can alter it by changing the beneficiaries or adding insured individuals. The insured refers to anyone covered under an insurance policy, and the policyholder is almost always included in this group. In some cases, immediate family members such as spouses, children, and parents are also covered by default under certain types of insurance.

Now, let's discuss the concept of primary and secondary insurance. Many people have access to healthcare coverage through both primary and secondary insurance plans. The primary insurance is the first policy responsible for covering medical expenses and typically serves as the main source of financial protection. It is billed first and pays according to its coverage limits and rules. Once the primary insurance has paid up to its limits, the secondary insurance takes effect. This means that the secondary insurance plan covers additional health care costs or fills in any gaps left by the primary insurance.

Secondary insurance is especially beneficial for individuals with high medical expenses or those who require specialized treatments not fully covered by the primary insurance. It is an additional policy that acts as a supplement to the primary coverage. While it is not the main source of coverage, it can help cover deductibles, copays, and unexpected medical needs, such as critical care for injuries or cancer treatment.

The coordination of benefits between primary and secondary insurance ensures that individuals receive maximum coverage. It is important to note that the order of payment is predetermined, and the primary insurance is always billed first. This means that individuals cannot choose which insurance to use when scheduling healthcare services. Therefore, it is advisable to ensure that healthcare providers are in-network with the primary insurance plan.

Life Insurance: Eligibility Requirements and Their Impact

You may want to see also

Explore related products

![]()

The primary insurance holder can change the beneficiaries

A policyholder is the person who has purchased and owns an insurance policy. They are responsible for paying the premium, which is the monthly cost charged by the provider for their insurance policies. The policyholder's name is on the account, so they receive the bill. Being the policyholder also means having control over the policy.

The policyholder is often the insured, meaning they are covered by the insurance policy. However, in some cases, the policyholder may purchase a policy to cover a loved one, such as a spouse or child. For example, Alex may purchase a life insurance policy for his husband, Greg, who would be listed as the insured, while Alex remains the policyholder.

As the policyholder, you have the authority to make changes to the policy. This includes altering beneficiaries or adding insured individuals. A beneficiary is an individual who receives the death benefit of a life insurance policy. They may or may not be the policyholder. A single policy can have multiple beneficiaries, and the policyholder can decide what portions of the payout go to each beneficiary.

It is important to review and update your beneficiaries whenever your life situation changes. You can often do this online or by contacting your insurance company or benefits department if your insurance is provided by your employer. By understanding your role as the primary insurance holder and the options available to you, you can ensure that your insurance policy aligns with your wishes and protects your loved ones.

Life Insurance: Group Benefits and Your Options

You may want to see also

Frequently asked questions

The primary insurance holder is the main person on the policy. They are responsible for paying the premium, which is the monthly cost charged by the provider. The primary insurance holder is billed first when receiving healthcare.

Primary insurance is typically insurance that covers a person as an employee, subscriber, or member. Secondary insurance is a health insurance plan that covers you in addition to your primary insurance plan. It is usually billed when the primary insurance plan is exhausted and may help cover additional healthcare costs.

Yes, it is possible to be covered by both your parent's and your spouse's insurance. In this case, the insurance provided by your parents would be your primary insurance, and the insurance provided by your spouse would be your secondary insurance.

Yes, as the primary insured, you can add people to the policy as secondary insured individuals. This allows family members to benefit from your insurance policy.