Life insurance is a contract where a policyholder pays monthly or yearly premiums, and, in exchange, the insurer promises to pay a death benefit to the policyholder's beneficiaries. This death benefit can be used for many purposes, such as replacing lost income, paying off debts, funding children's college, and saving for emergencies. A beneficiary can be a member of your family, a close friend, or a charity. While the policyholder usually informs the beneficiary ahead of time, they may sometimes forget to do so. If you think you might be a beneficiary but haven't been informed, there are ways to find out, such as by contacting the insurance company or using a life insurance policy locator service.

| Characteristics | Values |

|---|---|

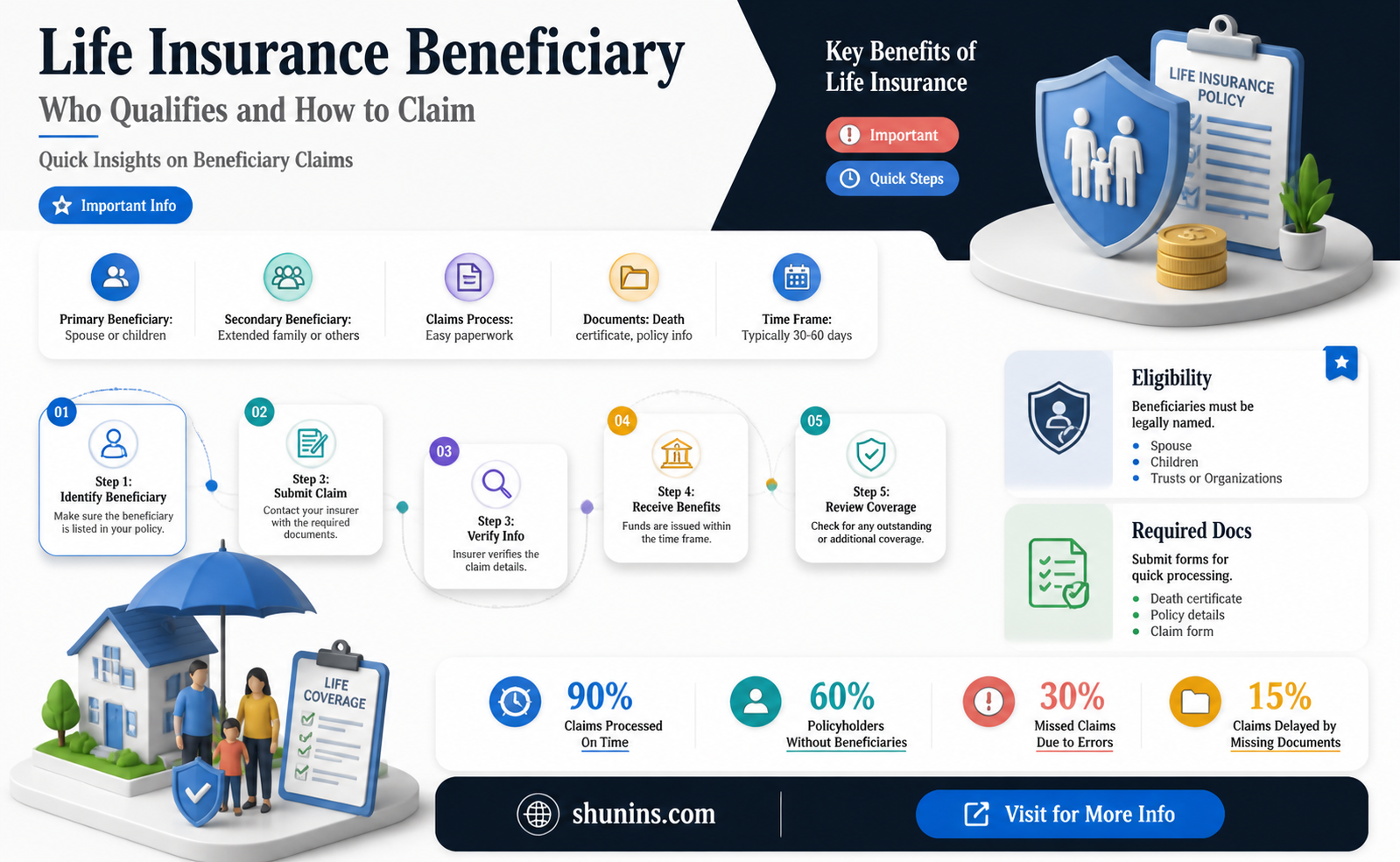

| Who is a life insurance beneficiary? | A person or entity designated by the policyholder to receive the policy's death benefit when they pass away. |

| Who can be a life insurance beneficiary? | Family members, charitable organizations, legal entities, etc. |

| How many life insurance beneficiaries can be chosen? | One or multiple beneficiaries can be chosen. |

| Who is usually chosen as a life insurance beneficiary? | Spouse, child, charity, or multiple beneficiaries. |

| What if no beneficiary is chosen? | The death benefit might be paid to the policyholder's estate, which can delay payment to any heirs. |

| What are the different types of life insurance beneficiaries? | Primary and contingent beneficiaries. |

| What is a primary life insurance beneficiary? | The person or entity entitled to the death benefit. |

| What is a contingent life insurance beneficiary? | The person or entity that receives the payout if the primary beneficiary passes away or cannot be located. |

| What is a revocable beneficiary? | A beneficiary that can be removed or have their portion of the death benefit changed without their consent. |

| What is an irrevocable beneficiary? | A beneficiary that cannot be removed or have their portion of the death benefit altered without their consent. |

| Who can change the beneficiary on a life insurance policy? | Only the policyholder or someone with durable power of attorney for the policyholder can change the beneficiary. |

| How to find out if you are a life insurance beneficiary? | Check with family members, look through documents, contact the claim department, or search for unclaimed policies. |

Explore related products

What You'll Learn

![]()

How to find out if you're a life insurance beneficiary

If you believe you may be a life insurance beneficiary, there are several steps you can take to find out. Firstly, it is important to note that beneficiaries are usually informed by the policyholder before the policyholder's death. This is the ideal situation, as the beneficiary is made aware of their status ahead of time and can locate the policy and contact the insurance company when the time comes. However, if you suspect that you may be a beneficiary but have not been informed, there are ways to confirm your status.

One way to find out is to ask other family members who may have knowledge of the policy. If possible, look through the policyholder's personal papers, including digital storage on computers and mobile phones, for the insurance policy itself or any life insurance receipts or evidence of payments. If you believe the policyholder may have been covered through their employer, you can contact their former employer or labour union. If you are able to locate the name of the insurance company, you can start the claim process or contact them directly to confirm your status as a beneficiary.

If you are unable to find any information through the above methods, there are still options available. You can contact the National Association of Insurance Commissioners (NAIC) and use their free Life Insurance Policy Locator Service, which searches the databases of many insurance companies. Alternatively, you can try contacting your state's Department of Insurance (DOI), as some states have websites where you can input information about the deceased and find out if they had insurance policies.

The Ultimate No-Lapse Guarantee Life Insurance Guide

You may want to see also

Explore related products

![A treatise on the law of benefit societies and life insurance: voluntary associations regular life beneficiary and accident insurance. By Frederick H. Bacon ... v.1. Volume v.1 1904 [Leather Bound]](https://m.media-amazon.com/images/I/416JPiaex-L._AC_UY218_.jpg)

![A Treatise on the Law of Benefit Societies and Life Insurance : Voluntary Associations, Regular Life, Beneficiary and Accident Insurance 1904 [Leather Bound]](https://m.media-amazon.com/images/I/617DLHXyzlL._AC_UY218_.jpg)

![]()

What to do if you're a life insurance beneficiary

If you're a life insurance beneficiary, there are several steps you can take to ensure you receive the death benefit. Here's what to do:

Confirm your beneficiary status:

Talk to your loved one while they're still alive. This is the easiest way to confirm if you are a beneficiary and to obtain necessary information for claiming the death benefit later. If your loved one has passed away, you may need to look through their financial documents for policy information.

Contact the insurance company:

Reach out to the insurer and inform them of the policyholder's passing. They will guide you through the process of filing a claim and provide you with a list of required documents. Having the policy number and insurance company's name will be helpful at this stage.

Gather required documentation:

Follow the insurance company's instructions regarding the documentation needed to file a claim. This may include a copy of the death certificate and other information to confirm your identity and your relationship to the policyholder.

File the claim:

Submit your claim to the insurer along with the required documentation. Be sure to follow all instructions carefully to minimize the risk of errors or claim denial.

Receive the death benefit:

If your claim is approved, the insurer will pay out the death benefit. The amount and method of payment (lump sum or installments) may vary depending on the policy type and coverage amount. Death benefits are generally tax-free regarding income taxes, but it's always a good idea to consult a financial advisor when receiving a windfall.

Remember, it's important to be proactive in these situations. Don't assume that the insurance company will automatically contact you, and don't rely solely on the policyholder to inform you of your beneficiary status. By taking the necessary steps, you can ensure that you receive the financial protection that the policyholder intended for you.

Life Insurance: Does Being Overweight Affect Eligibility?

You may want to see also

Explore related products

![]()

What to do if you're unsure if you're a beneficiary

If you are unsure whether you are a beneficiary, there are several steps you can take to find out. Firstly, it is important to note that you will not be automatically contacted by the insurance company, so you will need to take the initiative to find out.

Begin by asking other family members, as the policyholder may have informed someone else. If possible, look through the policyholder's personal papers, including digital documents, for the insurance policy or any evidence of payments to an insurance company. Contact the policyholder's former employer, as they may have been covered through their work. If you discover the name of the insurance company, you can start the claim process and ask them for more information.

If you are still unsure, you can try contacting the National Association of Insurance Commissioners (NAIC) and using their free Life Insurance Policy Locator Service. This searches the databases of many insurance companies to find policies. You can also try contacting your state's Department of Insurance, as some states have websites where you can search for policies using the details of the deceased.

Transamerica Life Insurance: Understanding the Cash Value Component

You may want to see also

Explore related products

$28.66 $42

![]()

What to do if you're the beneficiary of an unclaimed policy

If you're the beneficiary of an unclaimed life insurance policy, there are several steps you can take to claim the benefits. Here's a guide to help you through the process:

Locate the Policy

Firstly, try to find out if a policy exists. Check if you have any information about the insurance company and the policy. Look for financial documents, such as tax returns, bank statements, or insurance receipts. Go through the deceased's paperwork, including filing cabinets, safes, and digital storage. Contact the deceased's financial advisor or accountant, as they may have information about the policy.

Use Online Tools

If you don't have any information about the policy, there are online tools that can help. The National Association of Insurance Commissioners (NAIC) has a Life Insurance Policy Locator Service that searches the records of participating insurance companies. You will need the deceased's legal name, Social Security number, and dates of birth and death. This process can take several months, but it has helped beneficiaries claim over $6.7 billion in benefits since 2016.

You can also try the National Association of Unclaimed Property Administrators (NAUPA)'s Missing Money site, which allows you to search multiple state databases simultaneously for unclaimed funds, including insurance payouts. Additionally, some states have DOI websites where you can search for insurance policies using information about the deceased.

Contact Employers

Many companies offer life insurance as part of their employee benefits packages. Contact the deceased's most recent employer, especially if they passed away while employed, to see if they had any group life insurance or supplemental insurance.

Contact State Departments

If you still can't find the policy, contact your state's insurance department. Unclaimed life insurance policies are eventually passed on to the state insurance department if the insurer is aware of the policyholder's death but hasn't received a claim. The NAIC can provide you with the contact details for the relevant department.

File a Claim

Once you've located the policy, you'll need to file a claim to receive the benefits. You can work with an insurance agent or contact the insurer directly. You'll need several copies of the death certificate, as well as your identification and personal details to complete the claim form. You'll also need to choose how you want to receive the benefits, such as a lump sum or annuity.

It's important to act promptly when filing a claim, as the longer you wait, the longer it may take to receive the payout. However, there is no deadline or expiration date for claiming benefits from an active life insurance policy.

Login Credentials for SBI Life Insurance: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

How to select a contingent beneficiary

A contingent beneficiary, or secondary beneficiary, is a backup to the primary beneficiaries named on a life insurance policy. While it is not mandatory to designate a contingent beneficiary, it is advisable to do so to ensure that your death benefit goes to the right person or organisation in case your primary beneficiaries are no longer alive or able to receive the benefit.

- Understand the role: A contingent beneficiary inherits your assets only if your primary beneficiary has died, cannot be located, or refuses the inheritance. They are second in line to inherit your assets, and only inherit if all primary beneficiaries have passed away before the original account owner.

- Choose the type of contingent beneficiary: Contingent beneficiaries can be individuals, such as a spouse, adult children, siblings, or nieces and nephews. They can also be organisations, institutions, charities, or trusts. You can choose multiple contingent beneficiaries and allocate a percentage of your payout for each.

- Review and update: Just like primary beneficiaries, contingent beneficiaries should be reviewed and updated after major life changes, such as marriage, divorce, birth, or death.

- Notify your beneficiaries: While it is not mandatory to inform your contingent beneficiaries, it is advisable to do so. Let them know that they are named in your life insurance policy and provide them with the name of the insurance company.

- Keep your policy safe and accessible: Store your policy in a safe place and inform your beneficiaries or trusted advisors, such as accountants or attorneys, of its location.

Remember, there is no right or wrong way to select a contingent beneficiary. The important thing is to ensure that your assets go to the people or organisations you intend after your passing.

Health and Life Insurance Exam: Challenging or Easy?

You may want to see also

Frequently asked questions

If the policyholder is still alive, you can ask them. If not, you may need to look through their financial documents for information on the insurance company and policy. You can then contact the insurance company, who may be able to tell you if you are a beneficiary.

You will need to provide the policyholder's name and date of birth, the date of their passing, and your full name and relationship to the policyholder.

You can use a life insurance policy locator service, such as the National Association of Insurance Commissioners (NAIC) Life Insurance Policy Locator, to help track down lost policies.

If there is no named beneficiary, the death benefit will usually be awarded to the policyholder's immediate heirs, such as their spouse, children, or parents.

Many states require insurance companies to check the Social Security "Master Death File" for deceased policyholders and to try to notify their beneficiaries. However, this can take time, and it is not a requirement in every state. It is important to be proactive and contact the insurance company yourself if you believe you are a beneficiary.