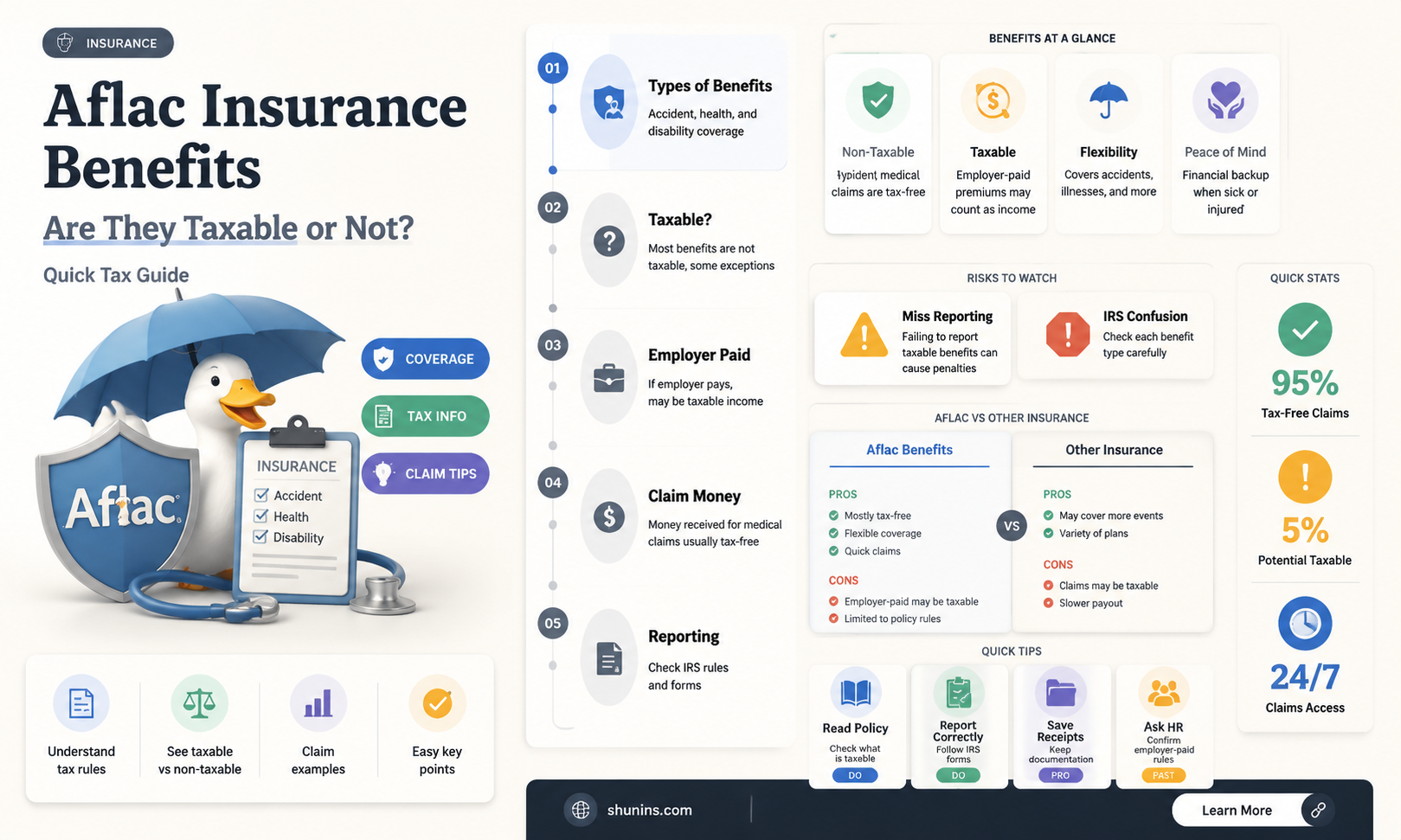

Aflac provides supplemental insurance to help pay for expenses that major medical insurance does not cover. The company offers a range of insurance plans, including life insurance, short-term disability insurance, critical illness insurance, and fixed-indemnity health plans. When considering Aflac insurance, it is essential to understand the tax implications of the benefits received. In general, the taxability of benefits depends on various factors, such as the type of insurance, the structure of premium payments, and the individual's specific circumstances.

| Characteristics | Values |

|---|---|

| Life insurance premiums | Not tax deductible |

| Life insurance proceeds | Not usually taxable |

| Tax benefits of life insurance | Deductions for business owners with business-paid premiums |

| Tax benefits of life insurance | Tax-deferred cash growth |

| When life insurance proceeds are taxable | When they have accumulated some interest |

| When life insurance proceeds are taxable | When the beneficiary isn't named in the policy |

| When life insurance proceeds are taxable | When the cash value is higher than the gift tax exemption |

| Short-term disability benefits | Not taxable if you pay for the premiums yourself with after-tax dollars |

| Short-term disability benefits | Taxable if your employer pays 100% of the premiums |

| Short-term disability benefits | Taxable if the premiums are automatically deducted from your paycheck |

| Critical illness insurance | Tax-deductible |

| Critical illness insurance | Tax-free if you pay the premiums with after-tax dollars |

| Fixed-indemnity benefits | Not taxable if the amount paid under the policy does not exceed the individual's unreimbursed medical expenses |

Explore related products

What You'll Learn

- Life insurance premiums are not tax-deductible but offer tax benefits

- Taxing depends on the individual's unreimbursed medical expenses

- Critical illness insurance cash benefits are not taxable if premiums are paid with after-tax dollars

- Short-term disability benefits are taxable if the employer pays 100% of the premiums

- Fixed-indemnity health plans are fully taxable

![]()

Life insurance premiums are not tax-deductible but offer tax benefits

Life insurance premiums are generally not tax-deductible for most individuals. However, life insurance policies may offer other tax benefits, such as tax-deferred growth, access to cash value, and tax advantages for business owners.

In the context of tax deductions, it's important to distinguish between tax-deductible expenses and tax-free benefits. While life insurance premiums themselves are typically not tax-deductible, the death benefit paid out to beneficiaries is usually tax-free. This means that while you cannot reduce your taxable income by claiming premiums as a deduction, the proceeds received by your beneficiaries are generally not subject to income tax.

One exception to the non-deductibility of life insurance premiums is for business owners. If you own a business and provide group term life insurance for your employees, the premiums may be deductible as a business expense. Additionally, if you have a business-paid premium, such as through an executive bonus plan or alimony arrangement, these premiums may also be deductible.

Another tax advantage of life insurance is the tax-deferred growth of the policy's cash value. The cash value of your life insurance plan is not subject to taxation while it is growing. This allows for higher interest rates and the accumulation of tax-free wealth within the policy.

It's worth noting that while life insurance proceeds are typically not taxable, there are some exceptions. For example, if the proceeds have accumulated interest, taxes are usually due on the interest earned. Additionally, if the policy is included in the insured's taxable estate, it may increase the estate's value and trigger estate taxes. In some cases, transferring ownership of the policy to another person or entity can help avoid taxation.

While life insurance premiums are generally not tax-deductible, the tax benefits of life insurance policies lie in the tax-free death benefit and the tax-deferred growth of the policy's cash value. These advantages can provide significant financial protection and stability to beneficiaries. However, it's always recommended to consult with a tax professional or financial advisor to understand the specific tax implications of your life insurance policy.

Life Insurance Simplified: Understanding Term Coverage

You may want to see also

Explore related products

![]()

Taxing depends on the individual's unreimbursed medical expenses

According to the IRS, if premiums are paid on a pre-tax basis through employer contributions or employee pre-tax salary reduction through a cafeteria plan, then whether the benefits are taxable depends on the individual’s unreimbursed medical expenses. If the amount paid under the policy does not exceed the individual’s unreimbursed medical expenses, then the amount received is not included in the employee’s income. However, if the amount received under the fixed-indemnity policy is more than the individual’s unreimbursed medical expenses, then the excess is taxable.

For example, if a covered individual’s unreimbursed medical costs as a result of a medical office visit were $30, then $30 would be excluded from the employee’s income and the excess amount would be taxable. This is in reference to a traditional fixed-indemnity health plan that pays fixed amounts on the occurrence of health events such as a medical office visit or a hospital stay.

In the context of Aflac insurance, it is important to note that they provide supplemental insurance to help pay for benefits that major medical insurance does not cover. This means that Aflac insurance benefits may be used to cover unreimbursed medical expenses, which could impact the taxability of the benefits received.

It is also worth mentioning that unreimbursed medical expenses that can be deducted must exceed 7.5% of an individual's adjusted gross income (AGI). This means that only the portion of unreimbursed medical expenses that exceeds this threshold can be considered for tax deductions.

Additionally, it is important to keep in mind that different rules may apply depending on the specific type of insurance and the individual's circumstances. For example, life insurance proceeds are generally not taxable, but there may be exceptions, such as when the beneficiary is a third party or if the policy is sold for a profit. Consulting a tax professional is always recommended to ensure compliance with tax regulations.

Ameritas Life Insurance: What You Need to Know

You may want to see also

![]()

Critical illness insurance cash benefits are not taxable if premiums are paid with after-tax dollars

Critical illness insurance provides a financial safety net in the event of a life-threatening illness, helping to cover medical expenses and other costs. It typically pays out a lump sum benefit, which can be used to cover surgery, medications, therapies, and everyday expenses.

When it comes to the tax implications of critical illness insurance benefits, it depends on how the premiums are paid. If the premiums are paid with after-tax dollars, then the cash benefits received are generally not taxable. This means that if you have been paying for your critical illness insurance policy with after-tax money, you can receive the payout tax-free. This is because the benefits are considered a return of your own money, rather than additional income.

On the other hand, if the premiums are paid on a pre-tax basis, such as through employer contributions or employee pre-tax salary reductions, then the benefits may be taxable. In this case, the amount received under the policy that exceeds the individual's unreimbursed medical expenses is typically considered taxable income. It's important to note that tax laws can be complex and vary by location, so it's always advisable to consult with a tax professional to understand the specific tax implications for your situation.

Regarding Aflac insurance benefits, it is important to note that the tax implications may depend on the specific type of insurance product and the circumstances of the policyholder. Aflac offers supplemental insurance for individuals and groups to help pay for expenses that major medical insurance may not cover. While Aflac does not provide explicit information about the tax status of their critical illness insurance benefits, they do emphasize the importance of understanding the tax implications of insurance benefits and recommend consulting with a tax professional for the most accurate information.

In summary, critical illness insurance cash benefits are generally not taxable if the premiums are paid with after-tax dollars. However, if the premiums are paid with pre-tax dollars, some or all of the benefits may be subject to taxation. The specific tax implications can vary based on individual circumstances and the type of insurance product, so it is important to seek professional tax advice to ensure compliance with applicable tax laws.

Term Life Insurance: Cash Value or Not?

You may want to see also

![]()

Short-term disability benefits are taxable if the employer pays 100% of the premiums

If your employer pays 100% of your short-term disability insurance premiums, then your short-term disability benefits are taxable. This is because the premiums are considered paid by your employer, and the disability benefits are fully taxable. This is true even if the premiums are paid on a pre-tax basis through employer contributions. In this case, the taxability of the benefits depends on the individual's unreimbursed medical expenses. If the amount received under the policy is more than the individual's unreimbursed medical expenses, then the excess is taxable.

It's important to note that there are some exemptions to this rule. For example, reimbursements for medical care are not taxable, but they may reduce the amount of any medical cost deduction. Additionally, benefits received for loss of income under a no-fault car insurance policy and payments received for loss of a limb or permanent disfigurement are not taxable.

If you pay the premiums yourself with after-tax dollars, your short-term disability benefits are generally not taxable. However, if you decide to split premium payments with your employer, there are a few possible outcomes. If the premiums are automatically deducted from your paycheck, you may have to pay taxes on your portion of the short-term disability benefits. On the other hand, if you pay your share of the premiums with after-tax dollars, only half of the benefits would be taxed.

Aflac, a supplemental insurance company, provides coverage for individuals and groups to help pay for benefits that major medical insurance may not cover. This includes short-term disability insurance, which can provide cash benefits to help with out-of-pocket expenses. While Aflac does not specify the tax implications of its short-term disability benefits, it is likely that the same rules apply as with other short-term disability insurance plans.

Best Value Life Insurance: Maximum Coverage, Minimum Dollars

You may want to see also

![]()

Fixed-indemnity health plans are fully taxable

There has been some confusion regarding the taxability of fixed-indemnity health plans. This confusion arose from a memorandum issued by the IRS in December 2016, which used overly broad language to describe abusive tax shelter arrangements. The language implied that benefits under any fixed indemnity health plan were always fully taxable. However, this statement was specific to abusive tax arrangements and did not reflect the taxation of traditional, fully insured fixed-indemnity benefits.

To clarify, the IRS issued a revised memorandum in April 2017, reconfirming that nothing had changed regarding the taxation of traditional, fully insured fixed-indemnity arrangements. The memo included an example of a traditional fixed-indemnity health plan that pays fixed amounts for health events like medical office visits or hospital stays. In this example, if the premiums are paid on a pre-tax basis, the benefits are taxable only if they exceed the individual's unreimbursed medical expenses. Specifically, only the excess amount above these unreimbursed medical expenses is taxable.

It's important to note that the taxation of benefits under fixed indemnity health policies is governed by IRS Code section 105(b). This code section was the subject of an important ruling in 1969, known as Revenue Ruling 69-154. This ruling concluded that when a fixed indemnity health policy is paid for on a pre-tax basis, benefits are taxable only to the extent that they exceed unreimbursed medical expenses. The ruling considered various factors, including other fixed indemnity policies held by the individual and the total amount of medical and reimbursed expenses.

In summary, while there was initial confusion due to broad language in an IRS memorandum, the IRS has clarified that fixed-indemnity health plans are not always fully taxable. The tax treatment depends on whether the benefits exceed the individual's unreimbursed medical expenses, with only the excess amount being subject to taxation. This clarification provides assurance to agents, brokers, employers, and individuals regarding the tax treatment of benefits received under pretax-paid health indemnity policies.

Spendthrift Clause: Protecting Life Insurance Beneficiaries' Interests

You may want to see also

Frequently asked questions

Whether or not your short-term disability benefits are taxable depends on how you structured your premium payments. If you pay the premiums yourself with after-tax dollars, your short-term disability benefits are not taxable. However, if your employer pays 100% of the premiums, your short-term disability income is taxable.

Critical illness insurance benefits are generally not taxable if you pay the premiums with after-tax dollars. However, it is recommended that you consult with a tax professional for the most accurate information regarding tax-deductible benefits for critical illness insurance.

Life insurance benefits are typically not taxable if the policy owner and the insured person are the same. However, if a third party is involved, the beneficiary of the life insurance policy may be taxed. Additionally, if you sell your life insurance policy, the payout may be subject to income tax if the profits exceed what you have paid so far.

If the premiums are paid on a pretax basis through employer contributions or employee pretax salary reduction, then the taxability of the benefits depends on the individual's unreimbursed medical expenses. If the amount paid under the policy does not exceed these expenses, the benefit is not taxable. However, if the amount received is more than the unreimbursed medical expenses, the excess is taxable.