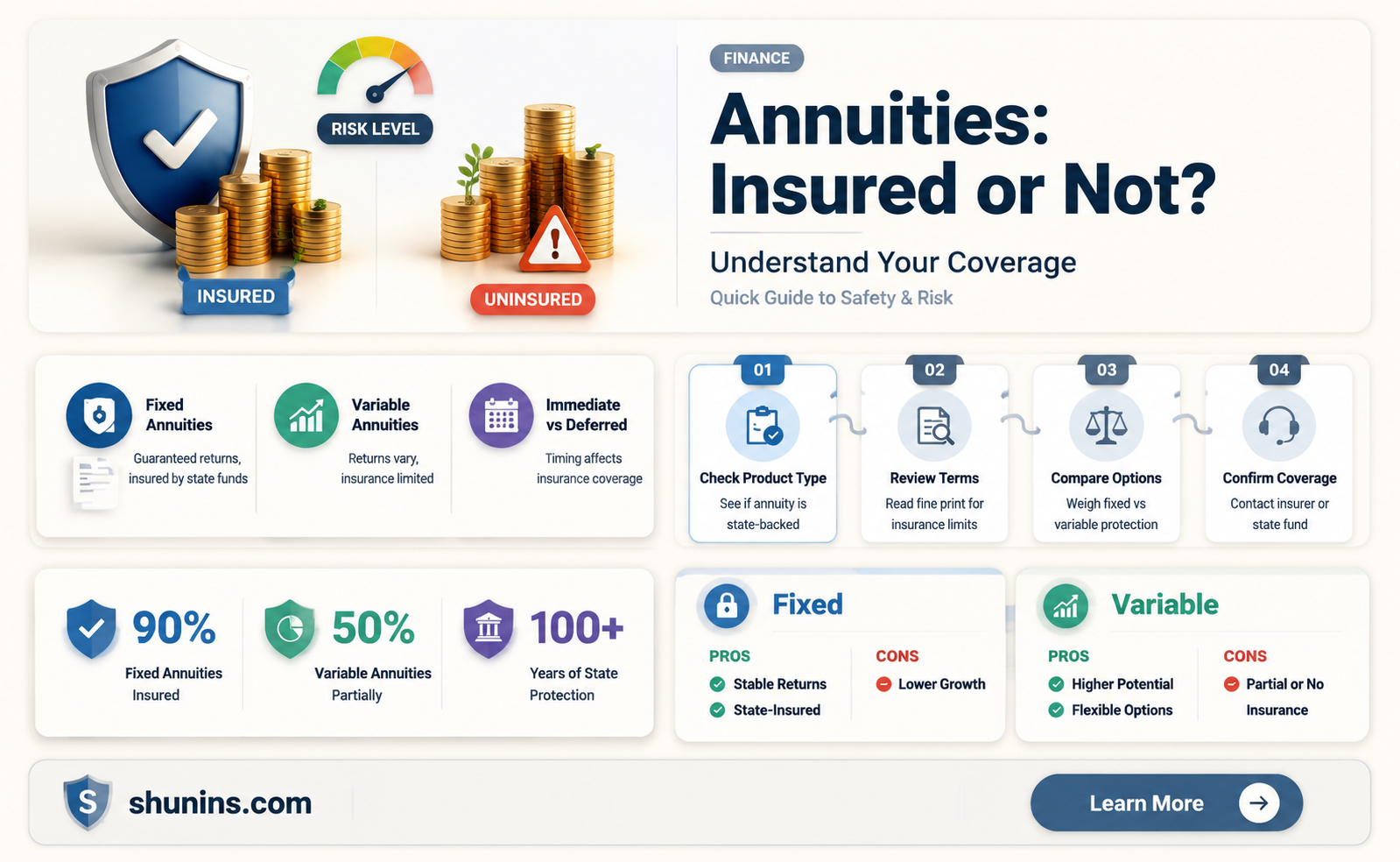

Annuities are insurance contracts that provide a guaranteed stream of income, making them a popular choice for retirees. They are typically considered safe investments, with fixed annuities offering a guaranteed rate of return over a specific period. While annuities are not FDIC-insured, they are backed by the financial strength of insurance companies and regulated primarily at the state level. State guaranty associations offer additional protection in the event of an insurer's failure, and certain protections are in place to safeguard investments. Annuities are generally seen as low-risk assets, but they are not entirely risk-free, and fees may impact overall returns.

| Characteristics | Values |

|---|---|

| Definition | An annuity is an insurance contract designed to provide a guaranteed stream of income, making it a popular choice among retirees. |

| Purchase | While only insurance companies can issue annuities, they are often available for purchase through banks, brokerage firms, and financial advisors. |

| Types | Fixed, variable, and indexed annuities. |

| Safety | Annuities are generally considered safe investments, but they are not entirely risk-free. Fees could diminish returns, and your money is not insured by the Federal Deposit Insurance Corporation (FDIC). |

| Regulation | Annuities are regulated at the state level by state insurance commissioners. Variable annuities and registered index-linked annuities (RILAs) are also regulated by the SEC and FINRA. |

| Protection | In the event of an insurance company's failure, certain protections are in place to safeguard your investment. State guaranty associations offer additional protection, typically up to $250,000. |

| Evaluation | When considering buying an annuity, it is essential to evaluate the insurer's stability using independent rating agencies, financial reports, and online information. |

Explore related products

What You'll Learn

![]()

Annuities are not FDIC-insured

Annuities are not insured by the Federal Deposit Insurance Corporation (FDIC). While annuities are typically considered safe investments, they are not without risk. Fees, for example, can eat into overall returns.

Annuities are insurance products, not banking products. While the FDIC protects bank deposits, annuities are protected through different mechanisms designed specifically for insurance products. These include state guaranty associations and insurance company safeguards.

State guaranty associations provide protection ranging from $100,000 to $500,000 per person, depending on the state. These associations work similarly to FDIC insurance but are state-based rather than federal. Before state guaranty associations come into play, annuities are protected by the insurance company's own financial strength. Insurance companies maintain several safeguards, including substantial reserves to ensure they can meet their obligations. These reserves are strictly regulated and regularly audited.

In addition to state guaranty associations and insurance company safeguards, annuities are regulated by state insurance commissioners. Variable annuities and registered index-linked annuities (RILAs) are also regulated by the SEC and FINRA. While annuities are not insured by the FDIC, these alternative protection mechanisms often provide comparable or even superior security for investors.

Insurance Tests: Multiple Choice Questions Examined

You may want to see also

Explore related products

![]()

Annuities are a form of insurance

Annuities are typically considered safe investments, but they are not entirely risk-free. While fees and charges can reduce returns, annuities are backed by the financial strength of insurance companies. In the event that an insurer fails, certain protections are in place to safeguard investments. State guaranty associations, present in all 50 states, offer additional protection, typically up to $250,000. However, it is important to note that annuities are not insured by the Federal Deposit Insurance Corporation (FDIC) or the Securities Investor Protection Corporation (SIPC).

There are three main types of annuities: fixed, variable, and indexed. Fixed annuities provide a guaranteed rate of return and payout, offering stability. Variable annuities are securities regulated by the SEC and FINRA, while indexed annuities, such as registered index-linked annuities (RILAs), offer both upside limits and downside protection. When considering purchasing an annuity, it is essential to evaluate the insurer's stability using independent rating agencies, financial reports, and online information.

While annuities can be purchased through banks, brokerage firms, and financial advisors, they can only be issued by insurance companies. Annuities are regulated primarily at the state level by state insurance commissioners, and coverage levels can vary across states. Therefore, it is crucial to understand the specific protections and guarantees provided by the state in which the annuity is purchased.

Borrowing from Life Insurance: Genworth's Policy Loan Option

You may want to see also

Explore related products

![]()

State guaranty associations offer protection

Annuities are typically considered safe investments, but they are not without risk. While they are not insured by the Federal Deposit Insurance Corporation (FDIC), Securities Investor Protection Corporation (SIPC), or any other federal agency, state guaranty associations do offer protection for annuity owners.

State guaranty associations act as a safety net to protect annuity owners if the issuing insurance company becomes insolvent or cannot meet its financial obligations. These associations are nonprofit organizations that operate at the state level, and all 50 states, the District of Columbia, and Puerto Rico have their own guaranty associations. The state's insurance commissioner and an appointed board of directors typically govern these associations. Coverage levels can vary from state to state, with most states offering annuity coverage limits of up to $250,000 per owner.

The purpose of state guaranty associations is to protect consumers in the event of an insurance company's failure. This protection is similar to how the FDIC protects bank funds up to a maximum amount in the event of insolvency. However, unlike the FDIC, state guaranty associations are not federally regulated. Instead, they are governed by the individual states, which regulate insurance companies.

While state guaranty associations offer protection, it is important to note that they prohibit insurance agents from mentioning their coverage to promote the sale of annuities or insurance. Additionally, annuity owners may consider diversifying their investments across multiple carriers to stay under the benefit threshold and reduce their risk. By spreading their investments, annuity owners can ensure that they do not put all their eggs in one basket and potentially lose out on the added "peace of mind" that comes with diversification.

Mortgage Life Insurance: Protecting Your Home and Family

You may want to see also

Explore related products

![]()

Variable annuities are protected by SIPC

Annuities are a safe addition to your retirement plan, but they are not entirely risk-free. They are a contract between you and an insurance company, which promises to make periodic payments to you, either immediately or in the future. While annuities are typically considered safe, it is always possible to lose money when investing. Fees could diminish your returns, and your money is not insured by the Federal Deposit Insurance Corporation (FDIC).

Variable annuities are a type of annuity that allows your premiums to be invested in assets like stocks, bonds, money market funds, and mutual funds. They are hybrid investment vehicles that contain the features of both securities and insurance. Variable annuities are generally designed for retirement purposes after individuals have maxed out their 401(k)s and/or IRAs. As the invested capital appreciates, the annuity provides regular income up to the policy's set limits, which are rarely changeable after entering the contract.

Variable annuities are protected by the Securities Investor Protection Corporation (SIPC) in the event that the brokerage firm fails financially and assets are missing from customer accounts. However, SIPC protection is limited with respect to claims for variable annuity contracts. SIPC does not protect against the risk of default by the issuer of a variable annuity contract, typically an insurance company, and does not protect the value of the annuity contract. Additionally, SIPC protection is not available if the variable annuity contract is held in custody by the contract owner rather than the brokerage firm for the customer.

It is important to note that annuities, including variable annuities, are also protected by state guaranty associations, and coverage levels can vary from state to state. These protections safeguard your investment in the event that the issuing insurance company goes out of business. While annuities are regulated by state insurance commissioners, variable annuities are also considered securities and are regulated by the SEC and FINRA.

Voluntary Life Insurance: Pre-Tax Benefits for Employees

You may want to see also

Explore related products

![]()

Annuities are regulated by state insurance commissioners

Annuities are regulated at the state level by state insurance commissioners, leading to differences in annuity regulations between states. Each state's insurance commissioner is responsible for licensing and regulating annuity-issuing companies. Before being granted a license to sell annuities, insurance companies must comply with strict requirements regarding capital, surplus, and finances. State insurance commissioners also investigate and monitor company management to ensure that the company will protect the interests of its consumers.

State insurance commissioners monitor the finances of insurance companies and ensure that they follow requirements designed to protect customers from negligent practices. They also handle customer complaints and produce public information about relevant rule changes, state guarantee limits, and consumer notices.

State guaranty associations, governed by the state's insurance commissioner, provide protection for annuity owners in the event that an insurance company becomes insolvent and cannot pay. These guaranty associations work in tandem with state insurance departments to ensure the solvency of licensed insurers. They collect funds from participating insurance companies and use these funds to pay out claims and continue insurance coverage if an insurer fails. Coverage levels vary by state, with the typical statutory limit being $250,000 of an annuity contract.

While all annuities are regulated by state insurance commissioners, only a select few annuities, such as variable annuities and registered index-linked annuities (RILAs), are regulated at the federal level by the SEC and FINRA.

Quitting Tobacco: Better Life Insurance and a Healthier You

You may want to see also

Frequently asked questions

An annuity is an insurance contract designed to provide a guaranteed stream of income, making it a popular choice for retirees.

Annuities are not FDIC-insured but are backed by the financial strength of insurance companies. If an insurer fails, state guaranty associations offer additional protection, usually up to $250,000.

There are three types of annuities: fixed, variable, and indexed. With a fixed annuity, the insurance company guarantees the rate of return (the interest rate) and the payout to the investor. Variable annuities and registered index-linked annuities (RILAs) are considered securities and are regulated by the SEC and FINRA.

Annuities are typically considered safe investments that can provide guaranteed income in retirement. However, it's important to thoroughly evaluate the insurer's stability and consider the fees associated with annuities, as these can eat into your overall returns.

Annuities can be purchased through insurance companies, banks, brokerage firms, and financial advisors.