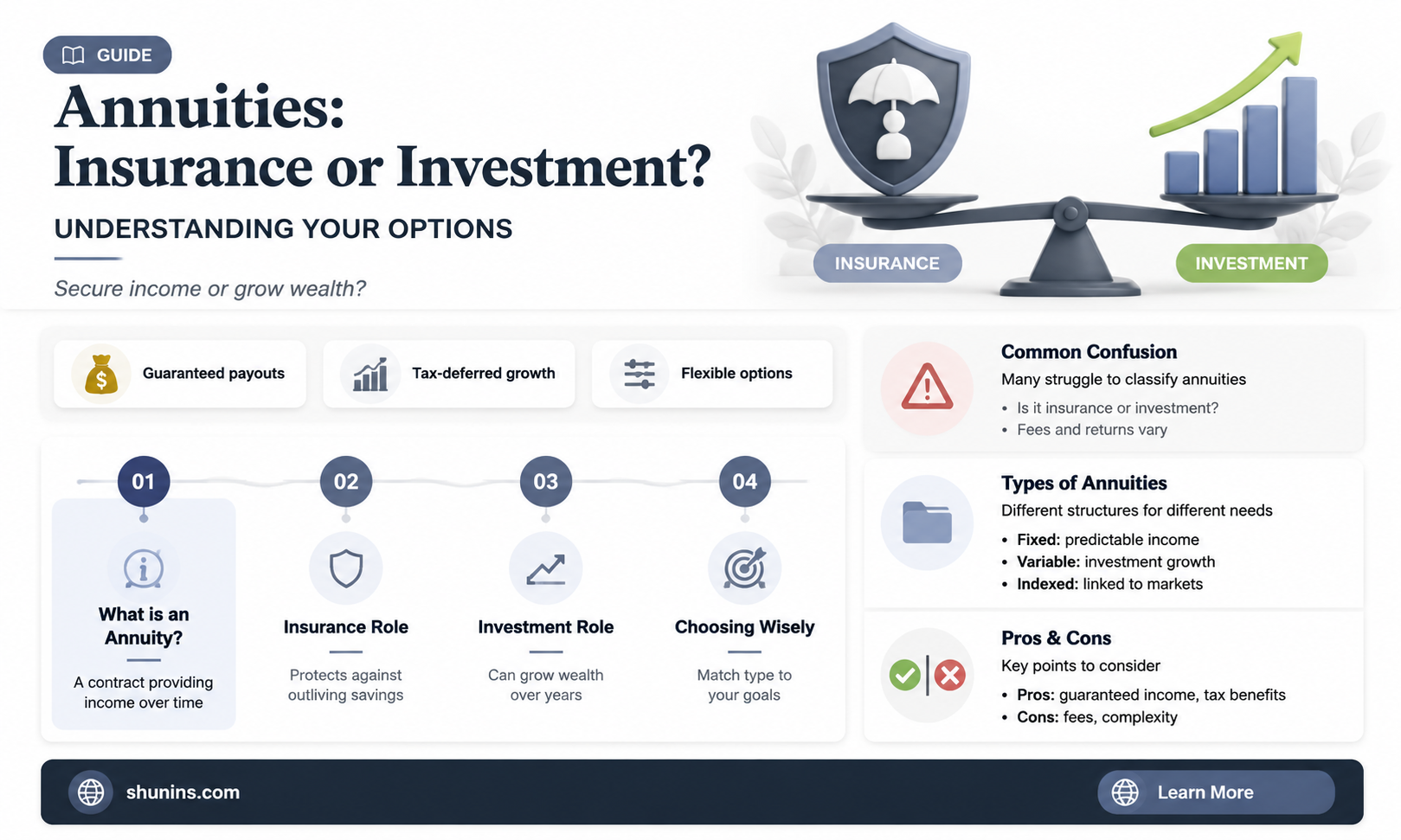

An annuity is a type of insurance contract that provides a guaranteed income stream, making it a common investment for retirees. Individuals purchase annuities through insurance companies, banks, brokerage firms, and financial advisors. In exchange for a lump sum or a series of payments, the insurance company guarantees returns. Annuities are regulated and protected at the state level, with each state having a guaranty organisation that insures annuities in the event that the issuing company fails. While annuities don't have federal government insurance, they are considered a form of insurance that helps individuals manage their income in retirement.

Explore related products

What You'll Learn

- Annuities are insurance contracts issued by financial institutions and bought by individuals

- Annuities are mainly used for retirement income purposes

- Annuities can be immediate or deferred, fixed, variable, or indexed

- Annuities are protected by state-level regulations and guaranty associations

- Annuities can be purchased through banks, brokerage firms, or financial advisors

![]()

Annuities are insurance contracts issued by financial institutions and bought by individuals

Annuities are often used to address the risk of outliving one's savings and to provide stable, guaranteed retirement income. They can be structured in different ways, such as immediate or deferred, fixed, variable, or indexed. Immediate annuities provide payouts immediately after the purchase of the plan, while deferred annuities allow for tax-deferred growth and payouts at a later date. Fixed annuities offer a guaranteed minimum interest rate and fixed periodic payments, while variable annuities are linked to the performance of investments.

It's important to note that annuities are complex financial products with various fees, charges, and potential penalties for early withdrawal. Individuals considering annuities should carefully research and understand the costs and risks involved before purchasing.

Annuities are protected by state-level regulations and guaranty associations. In the event that an insurance company issuing annuities goes out of business, customers are protected by their state's guaranty organization, which ensures that their claims will be covered.

Chiropractic Care and Out-of-Network Insurance: Navigating the Billing Process

You may want to see also

Explore related products

![The Doctrine of Interest and Annuities Analytically Investigated and Explained; Together with Several Useful Tables Connected with the Subject. By Francis Baily 1808 [Leather Bound]](https://m.media-amazon.com/images/I/617DLHXyzlL._AC_UY218_.jpg)

![]()

Annuities are mainly used for retirement income purposes

Annuities are financial products that offer a guaranteed income stream and are typically used by retirees to ensure a stable income during their retirement years. They are insurance contracts issued by financial institutions and bought by individuals, requiring the issuer to pay out a fixed or variable income stream to the purchaser. This income stream can be structured as a series of payments over time or as a lump-sum payment.

Annuities are designed to address the risk of retirees outliving their savings and provide a steady cash flow to sustain their standard of living. They can be purchased by making monthly premium payments or a lump-sum payment, and the income stream can begin immediately or at a specified future date. Annuities can be categorised as immediate or deferred, fixed, variable, or indexed.

Immediate annuities provide income right after purchase, often chosen by retirees to ensure a regular income stream. Deferred annuities, on the other hand, are more suitable for long-term planning, allowing the purchaser to specify an age when they wish to start receiving payments.

Fixed annuities offer a guaranteed minimum rate of interest and fixed periodic payments, while variable annuities provide the potential for higher returns based on the performance of underlying investments but carry more risk. Indexed annuities combine features of securities and insurance products, with returns based on a stock market index.

Annuities offer tax-deferred growth, allowing retirees to defer taxes on their income until withdrawals are made. They also provide death benefits, ensuring that beneficiaries receive a specific payment if the purchaser dies before receiving payments.

While annuities can provide a stable income stream for retirees, it is important to consider the associated fees, complexities, and potential early withdrawal penalties.

Term Insurance Comparison: Unraveling the Fine Print for Smart Choices

You may want to see also

Explore related products

![]()

Annuities can be immediate or deferred, fixed, variable, or indexed

Annuities are a type of insurance contract that offers a guaranteed income stream, making them a common investment for retirees. They are contracts sold by insurance companies that promise the buyer a future payout in regular instalments, usually monthly and often for life. Annuities can be immediate or deferred, fixed, variable, or indexed.

Immediate or Deferred

Annuities can be immediate or deferred in terms of when they begin to make payments. The basic question buyers need to consider is whether they want regular income now or at some future date.

An immediate annuity begins paying out as soon as the buyer makes a lump-sum payment to the insurer. An immediate annuity offers you an income right after purchasing the annuity plan. You make a lump sum payment to the insurance company, and the insurer gives you regular income payments, either for a specific period or for the rest of your life, shortly after purchasing the plan.

A deferred annuity, on the other hand, allows you to purchase an annuity plan and start receiving the payments at a later date in the future. Deferred annuity plans accumulate funds over a period. This is known as the accumulation phase of the plan. At the chosen date, you start receiving income payments from your accumulated capital. Deferred annuities should be considered long-term investments because they are less liquid than other types of investments.

Fixed, Variable, or Indexed

Annuities can also be either fixed, variable, or indexed, which determines how their rates of return are computed.

A fixed annuity guarantees payment of a set amount for the term of the agreement. It can't go up or down. Fixed annuities are regulated by state insurance commissioners. Fixed-rate annuities, also known as multi-year guarantee annuities (MYGA), describe insurance-based contracts typically funded with a lump sum premium payment. In exchange for the payment you make, insurance companies will credit your contract with an interest rate that is guaranteed for a pre-determined period of time, typically 2 to 10 years.

A variable annuity fluctuates based on the returns on the mutual funds it is invested in. Its value can go up or down. Variable annuities are regulated at the national level by the U.S. Securities and Exchange Commission (SEC) and FINRA. With a variable annuity, the insurer invests in a portfolio of mutual funds chosen by the buyer. The performance of those funds will determine how the account grows and how large a payout the buyer will eventually receive.

An indexed annuity is a hybrid of fixed and variable annuities. It combines features of securities and insurance products. The insurance company credits you with a return that is based on a stock market index, such as the Standard & Poor's 500 Index. Indexed annuities are regulated by state insurance commissioners.

Maximizing Insurance Reimbursement for Massage Therapy: A Guide to Efficient Billing

You may want to see also

Explore related products

![]()

Annuities are protected by state-level regulations and guaranty associations

Annuities are protected by guaranty associations at the state level. These are non-profit insurance organisations that protect annuity customers in the event that the insurance company becomes insolvent and cannot pay. All 50 states, as well as the District of Columbia and Puerto Rico, have their own guaranty associations.

Each state has its own limits on the maximum amount of coverage, but the typical statutory limit is $250,000 of an annuity contract. For example, California's guaranty association will cover only 80% of an annuity, up to a limit of $250,000, while Connecticut will cover up to $500,000 for annuities.

State guaranty associations work in tandem with state insurance departments to ensure the solvency of licensed insurers and provide protection if an insurer fails. They are funded by assessments of their member insurance companies.

In the event that an insurance company becomes insolvent, the state guaranty association will coordinate with other member agencies to transfer the insolvent agency's policies to a financially healthy insurance carrier.

Minimizing the Cost of Nylon-Term Insurance: Strategies for Savvy Consumers

You may want to see also

Explore related products

![]()

Annuities can be purchased through banks, brokerage firms, or financial advisors

Annuities are insurance products issued by insurance companies and sold by insurance agents, financial institutions, and financial advisors. While insurance companies are the only entities that can issue annuities, individuals can purchase them through banks, brokerage firms, and financial advisors.

Annuities are a type of insurance contract that can offer a guaranteed income stream, making them a common investment for retirees. In exchange for a lump sum or a series of payments, an insurance company provides guaranteed returns.

When buying an annuity, you can choose the type of annuity you want, compare offerings from different companies, and complete an application with your chosen annuity provider. A licensed insurance agent must handle the final submission of your contract.

- Assess your financial situation and establish goals: Understand your present and future financial situation and how an annuity can help you achieve your goals.

- Choose an annuity product: Select an annuity product that meets your needs and aligns with your goals. Annuities are highly customizable and can be tailored to provide income, growth, a death benefit, and more.

- Research annuity providers with strong credit ratings: Look for companies that specialize in the type of annuity you want and have strong credit ratings from financial rating agencies.

- Apply for the annuity and sign the contract: Work with the annuity provider and your financial advisor to apply for and sign the annuity contract. Remember that you can customize the contract to meet your needs.

- Fund your annuity with a premium payment: After signing the contract, transfer the money for the annuity premium payment. You can use cash, retirement funds, or money from a brokerage account.

It is important to note that annuities are complex financial products, and it is recommended to explore the purchase over time and consult with an unbiased third-party advisor.

Understanding General Aggregate Limits: The Cap on Insurance Claims

You may want to see also

Frequently asked questions

An annuity is a contract between an individual and an insurance company, where the individual makes either a single payment or a series of payments. In return, the insurance company agrees to make payments to the individual, either immediately or in the future. Annuities are typically used to provide a guaranteed income stream during retirement.

There are three basic types of annuities: fixed, variable, and indexed. Fixed annuities offer a guaranteed minimum interest rate and fixed periodic payments. Variable annuities allow individuals to direct their payments towards different investment options, and payouts vary based on the performance of those investments. Indexed annuities combine features of securities and insurance products, with returns based on the performance of a stock market index.

Annuities can be purchased directly from insurance companies, as well as through banks, brokerage firms, and financial advisors. It is important to understand the fees, charges, and risks associated with annuities before purchasing one.

Annuities are protected at the state level in the US. Each state has a guaranty organization that insurance companies must join, and these organizations provide protection for annuity customers in the event that the issuing insurance company goes out of business. The level of protection varies by state, but all 50 states provide coverage of at least $250,000 per customer, per company.