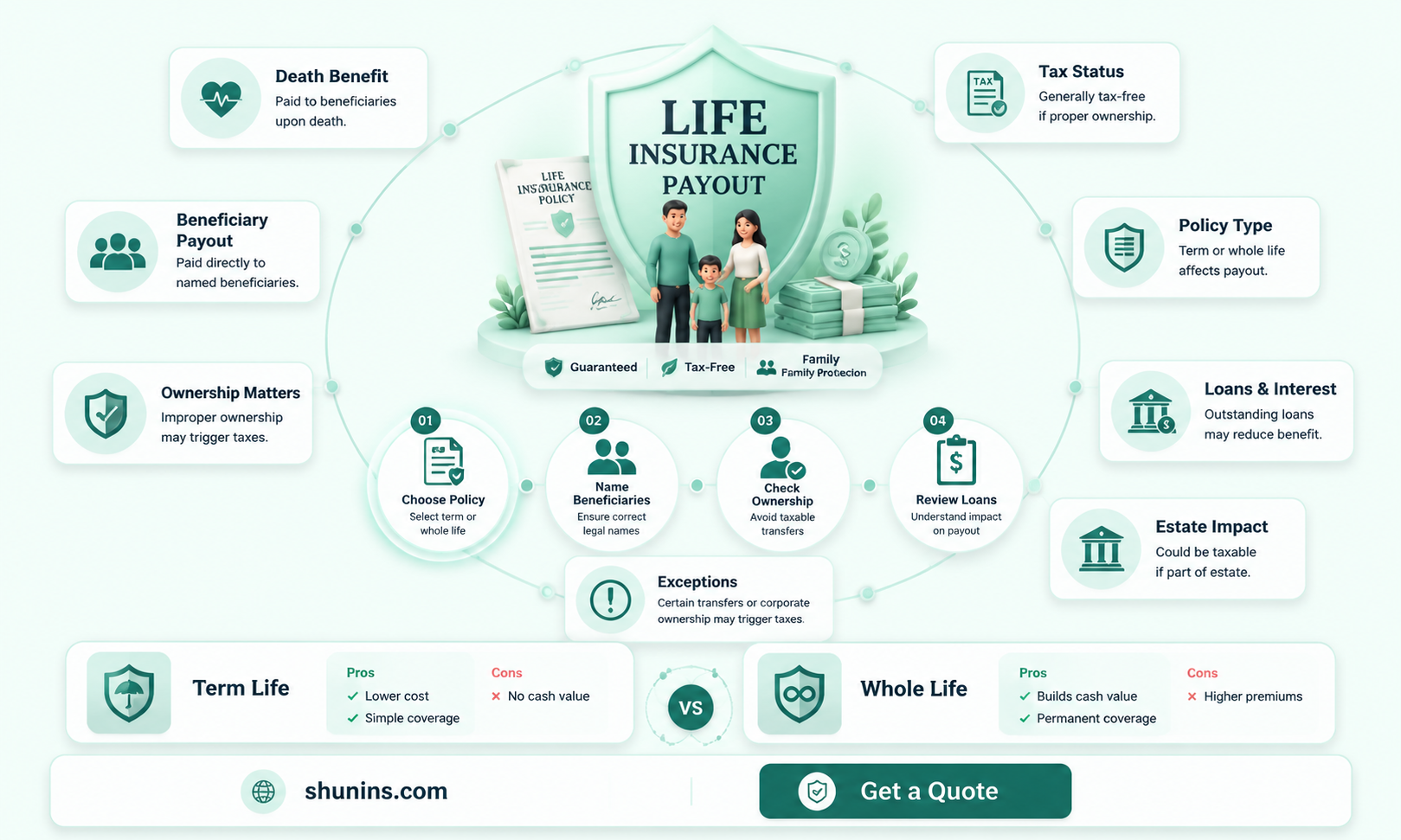

Auto insurance death benefits are typically not taxable, and beneficiaries will usually receive the payout without any tax liabilities. However, there are certain situations where exceptions apply, and understanding these circumstances is crucial for beneficiaries to navigate the tax implications effectively.

Explore related products

$63.99

What You'll Learn

![]()

Interest on death benefits is taxable

While auto insurance death benefits are generally not taxable, there are some exceptions. If the death benefit is paid out in installments, any interest accrued will be subject to tax.

If the death benefit is paid out in installments, the remaining portion of the benefit may earn interest. This interest is taxable and should be reported as such. The interest will be taxed, rather than the entire death benefit. This is the case for both life insurance and annuities.

For example, if a beneficiary chooses to receive their payout as an annuity (a series of payments over several years), any interest accrued by the annuity account may be subject to taxes. This is also the case for specific income payouts, where the insurance company places the benefit proceeds into an interest-bearing account and then uses those funds to make regular payments to the beneficiary.

When Death Benefits May Be Taxed

In addition to interest on death benefits, there are a few other circumstances in which death benefits may be taxed:

- The policyholder names their estate as a beneficiary: If the policyholder chooses their estate as a life insurance beneficiary, taxes may apply depending on the estate's value.

- The insured and the policy owner are different individuals: If a different person holds each role, there may be taxes involved.

- The death benefit and the total value of the deceased's estate exceed limits: If life insurance proceeds are included as part of the deceased's estate and together exceed the federal estate tax threshold, estate taxes must be paid on the proceeds over the allowed limit. As of 2024, this threshold was $13.61 million, and in 2023, it was $12.92 million.

Gap Insurance: Money-Back Guarantee?

You may want to see also

Explore related products

![]()

Naming your estate as beneficiary may result in taxes

Naming your estate as the beneficiary of your insurance policy may result in higher taxes. This is because the timeline for distributing the funds is shorter when paid to an estate than when paid to a named individual. The shorter timeline means more money is withdrawn each year, which increases the potential for higher taxes.

For example, most beneficiaries will have to withdraw funds from an IRA by the end of the 10th year following the year of death. However, if the beneficiary is an estate, the funds must be distributed within five years. The shorter timeline for estates may result in higher taxes for your loved ones.

Additionally, if the money is paid to your estate rather than a particular beneficiary, it could be taxable. In 2024, estates over $13.61 million owe estate tax.

Furthermore, naming your estate as a beneficiary may result in higher Medicare charges and increased potential for a "challenge" from a disgruntled heir. Challenges to a will could be more likely to be successful if the estate is named as the beneficiary.

Finally, assets left to a named beneficiary are generally protected from the claims of creditors. However, assets in your estate are not protected and may be subject to creditor invasion.

Add Your Vehicle to Direct Auto Insurance

You may want to see also

Explore related products

![]()

The death benefit may be a taxable gift in certain situations

The death benefit from a life insurance policy is typically not taxed. However, if the owner of the policy is not the same as the insured, the payout to the beneficiary could be considered a taxable gift. In other words, if three different people serve three distinct roles in connection with the policy, the IRS may consider the death benefit a gift from the policy owner to the beneficiary.

The three roles are:

- The policy owner: This is the person who purchased the policy and is responsible for paying the premiums.

- The insured: This is the person whose life is covered by the policy.

- The beneficiary: This is the person who receives the death benefit when the insured person dies.

For example, if a husband purchases a life insurance policy for his wife, and their son is listed as the beneficiary, the death benefit will be considered a gift from the husband to the son by the IRS. To avoid this, it is recommended to limit insurance policy involvement to only two people: a policyholder who is also the insured and the beneficiary.

Estimating Auto Insurance: A Quick Guide

You may want to see also

Explore related products

![]()

Death benefits are not subject to ordinary income tax

Death benefits from life insurance policies are not subject to ordinary income tax. This means that beneficiaries will receive the money without a tax burden hanging over their heads. However, there are certain situations where a life insurance death benefit may be taxable.

One such situation is when the beneficiary receives interest on the death benefit. While the death benefit payout itself is not taxable, any interest accrued on the payout will be taxed. This typically occurs when a beneficiary chooses to delay the payout or take the payout in installments, allowing interest to accumulate. In this case, the beneficiary will need to pay taxes on the interest earned.

Another situation where a life insurance death benefit may be taxable is when the payout goes into a taxable estate. If a beneficiary is not named or is deceased, the death benefit will go into the estate of the insured person. This can create a significant tax bill, especially when considering both federal and state estate taxes. It is important to name both primary and contingent beneficiaries to avoid this scenario.

Additionally, if the insured, policy owner, and beneficiary are three different people, the death benefit may be considered a taxable gift. In this case, the policy owner may have to pay gift tax if the payout exceeds the federal gift tax exemption limits. To avoid tax implications, it is recommended to limit the involvement of only two people: the policyholder, who is also the insured, and the beneficiary.

While death benefits from life insurance policies are generally not subject to ordinary income tax, it is important to be aware of these specific situations where taxation may apply.

Wells Fargo: Gap Insurance Options

You may want to see also

Explore related products

![]()

Death benefits are usually paid as a lump sum

In the context of auto insurance, death benefits refer to the payout that beneficiaries receive in the event of the insured person's death. While auto insurance death benefits are typically paid as a lump sum, beneficiaries may have the option to choose other payment alternatives. It is important to review the specific terms of the auto insurance policy to understand the available options and their tax implications.

Lump-sum death benefits are often preferred by beneficiaries for several reasons. Firstly, they provide immediate access to the entire benefit amount, allowing beneficiaries to address any urgent financial needs or settle outstanding debts. Secondly, lump-sum payments simplify the financial planning process for beneficiaries, as they do not have to worry about ongoing payments or interest accumulation. Finally, receiving the death benefit as a lump sum enables beneficiaries to make significant purchases or investments, such as paying off a mortgage, funding education, or starting a business.

However, it is worth noting that there are certain circumstances in which a lump-sum death benefit may be subject to taxation. For instance, if the policy accrued interest, taxes are typically owed on the interest accrued, rather than on the entire death benefit. Additionally, if the policy owner names their estate as the beneficiary, taxes may apply depending on the value of the estate.

Usaa: Gap Insurance Coverage

You may want to see also

Frequently asked questions

Death benefits from auto insurance are not usually taxed. However, if the beneficiary chooses to delay the payout or take the payout in installments, interest may accrue, and the interest paid to the beneficiary may be taxed.

A beneficiary is a person or entity that you can name in a life insurance policy to receive your death benefit upon your passing. You may choose one beneficiary or multiple beneficiaries, such as your spouse, adult children, a charity you believe in, a trust, or even a business.

There are a few strategies that beneficiaries can use to avoid paying taxes on a life insurance payout, such as transferring ownership of the policy to another person or entity, or setting up an irrevocable life insurance trust (ILIT).