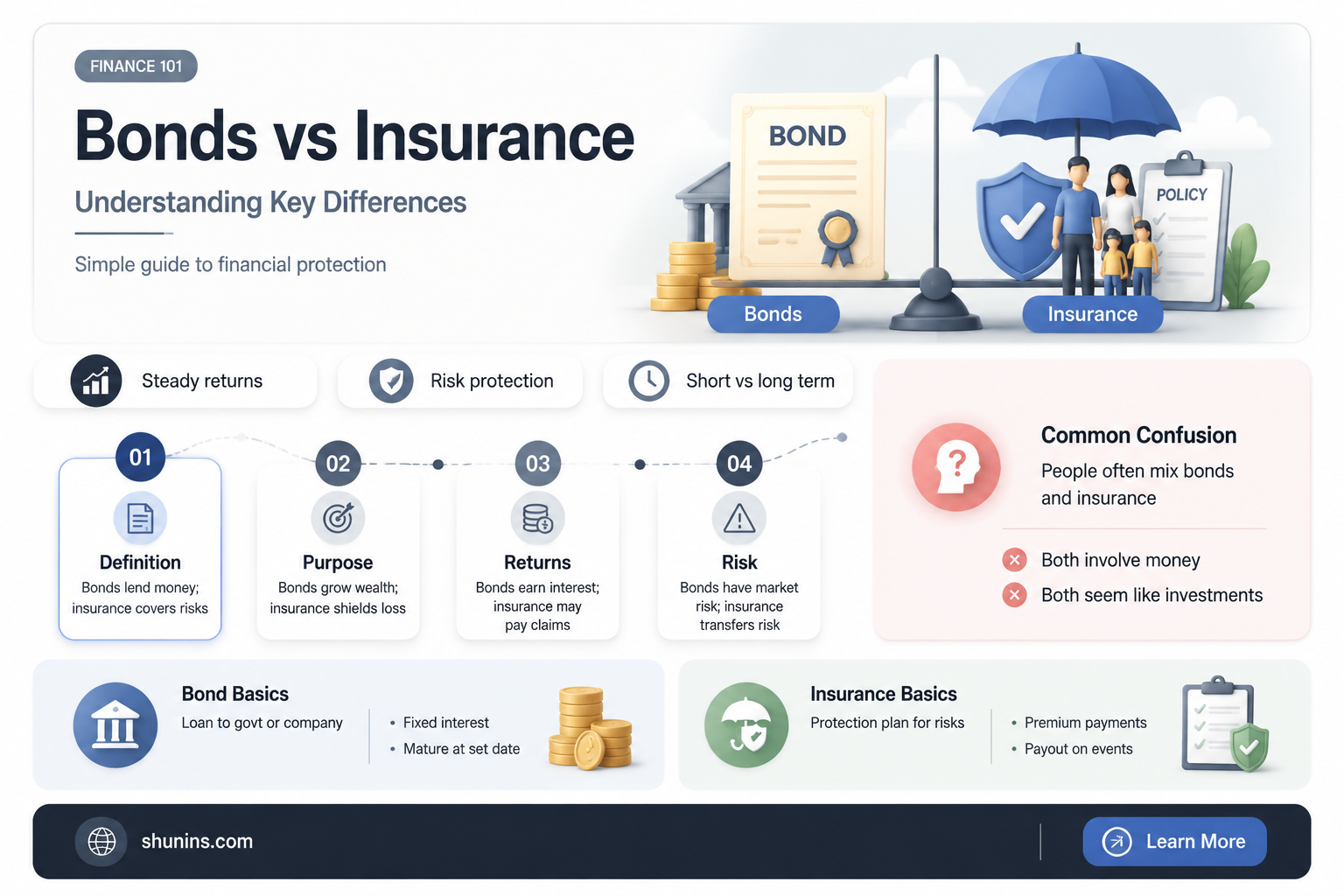

Bonds and insurance are both tools used to reduce financial risks and provide protection against financial loss. While they have similar intentions, they are two different products serving different purposes. Insurance is often a mandatory part of property ownership and covers unforeseen and/or accidental losses. On the other hand, bonds involve a three-party contract and cover acts that are done knowingly. This article will further explore the differences and similarities between bonds and insurance, providing insight into how these financial tools work and when they are used.

| Characteristics | Values |

|---|---|

| Number of parties involved | Insurance contracts are between two parties, while bonds are between three. |

| Purpose | Insurance covers unforeseen and/or accidental loss, while bonds cover acts that are done knowingly. |

| Applicability | Insurance is often a mandatory part of property ownership, while bonds are required by law in certain industries. |

| Protection | Insurance protects businesses from financial loss, while bonds protect a third party, often the public, from financial loss or damage due to non-compliance, wrongdoing, or misconduct. |

| Claims | Insurance companies are liable for paying claims using pooled premium funds, while the bonded principal is liable for reimbursing the surety for claims payments. |

| Premium payments | Insurance premiums are paid monthly and pooled to cover future claims, while bond premiums are a single, upfront purchase for a one-year term and do not cover future claims. |

| Risk | Insurance is a high-risk product, while bonds have historically had low loss ratios. |

| Liquidity | Insured bonds exhibit greater price stability and are more frequently traded than uninsured bonds. |

Explore related products

What You'll Learn

![]()

Surety bonds are a type of insurance

On the other hand, insurance policies are usually tailored to cover the operations of a business, and damages must occur for an insurance policy to pay out. An insurance policy will cover unforeseen and/or accidental loss, while bonds cover acts that you (or an employee) did knowingly. For instance, if your construction site was destroyed by a hurricane, you would have to turn to your insurance policy over your damaged equipment, not your contract surety bond.

While insurance claims are often out of one's control, surety bond claims should be avoided as they indicate a failure to uphold your end of a bargain. Insurance premiums cover potential business losses, while surety bond premiums act as a line of credit to ensure the principal fulfils the bond obligations.

Verisure Alarms: Are They Worth the Insurance Approval?

You may want to see also

Explore related products

![]()

Bonds and insurance serve different purposes

While bonds and insurance are both tools used to reduce risks and provide protection from financial loss, they serve different purposes. Insurance is a contract between two parties—the insurer and the insured—and covers unforeseen and/or accidental losses. Common types of insurance include home insurance, life insurance, and business insurance. For example, if your construction site was destroyed by a hurricane, you would turn to your insurance policy to cover the damage.

On the other hand, bonds are contracts between three parties: the principal (a business or professional that purchases the bond), the surety (the bonding company), and the obligee (the party protected by the bond, often the public). Bonds cover specific areas and are often required by law. They guarantee the quality of work or services provided by the principal and protect the obligee from financial loss or damage due to non-compliance, wrongdoing, or misconduct. For instance, a contractor might be required to provide a bond to protect against their work not being up to code or unfinished. In such a case, the surety company will hire another contractor to finish the job, and the principal will be responsible for reimbursing the surety for any claims payments.

While insurance policies are usually tailored to cover the operations of a business, bonds are very specific in nature. Insurance policies typically cover a range of unforeseen events, such as property damage, accidents, and injuries. In contrast, bonds do not require damage to trigger payment; they are triggered by the principal's inability to meet their financial obligations as specified in the bond.

Additionally, the process of obtaining insurance and bonds differs. Insurance policies are typically purchased from insurance companies, with monthly premium funds pooled to cover future claims. In contrast, bonds are purchased upfront for a specific term, acting as a line of credit to ensure the principal fulfills their obligations. If a claim is made against a bond, the surety company pays out and then seeks reimbursement from the principal.

Santa Rosa Hilton: Was the Fire Insurance Prepared For?

You may want to see also

Explore related products

![Surety Bonds: Nature, Functions, Underwriting Requirements [ 1922 ]](https://m.media-amazon.com/images/I/61bxACoaAyL._AC_UY218_.jpg)

![]()

Insurance is often mandatory

Insurance is often a mandatory part of property ownership. For example, in Florida, certain forms of auto insurance are required for everyone on the road. Similarly, many states require small businesses to carry certain types of business insurance, such as workers' compensation.

In the case of bonds, while they are not the same as insurance, they are also often required by law. Surety bonds are mandated in specific scenarios, such as when a business owner needs to guarantee the payment of state sales taxes or when a contractor bids on a public project. The requirement for surety bonds can vary based on state, industry, and business activities. For instance, in Oregon, contractors are mandated by law to obtain a surety bond as part of the licensing process.

The mandatory nature of insurance and bonds stems from their role in providing financial security and protection. Insurance acts as a safeguard against unforeseen and accidental losses, such as damage, theft, or financial ruin. It offers peace of mind by reimbursing covered losses through a contract between the policyholder and the insurance company. On the other hand, bonds, including contract and commercial surety bonds, serve as a guarantee of quality and financial assurance. They protect consumers and third parties from improper business conduct, financial loss, or damage due to non-compliance or misconduct.

While insurance and bonds have distinct purposes, they are both essential tools for managing risk and ensuring compliance in various industries. By understanding the mandatory nature of these financial products, individuals and businesses can make informed decisions to protect themselves and their assets.

Grow Your Career as a Bajaj Life Insurance Agent

You may want to see also

Explore related products

![]()

Bond insurance is a guarantee of repayment

While bonds and insurance are both tools used to reduce risks and provide protection from financial loss, they are two different products serving different purposes. Insurance covers unforeseen and/or accidental losses, while bonds cover acts that are done knowingly.

Bonds are like insurance in the sense that they both provide financial security in the event that something goes wrong. However, unlike insurance, bonds involve three parties: the principal, who is a professional or business that purchases the bond; the obligee, who is usually a government agency; and the surety company, which ensures the principal fulfils their obligations.

Now, bond insurance is a type of insurance policy that a bond issuer purchases to guarantee the repayment of the principal and all associated interest payments to the bondholders in the event of default. Bond issuers will buy this type of insurance to enhance their credit rating in order to reduce the amount of interest they need to pay and make the bonds more attractive to potential investors.

In summary, bond insurance is a guarantee of repayment in the event of default by the issuer. It protects bondholders from financial loss and provides them with peace of mind. By purchasing bond insurance, issuers can enhance their credit rating, making their bonds more attractive to investors.

Child Life Insurance: Protecting Your Child's Future

You may want to see also

Explore related products

![]()

Bond insurance improves market liquidity

While insurance and bonds are both tools used to reduce financial risk, they are two different products. Insurance covers unforeseen or accidental losses, while bonds cover acts that are done knowingly.

Bonds are often purchased by licensed professionals such as contractors, notary publics, and liquor license holders to guarantee the quality of their work. For example, a contractor may be required to provide a bond to protect against subpar work. If their work isn't up to code, the surety company will hire another contractor to finish the job.

The liquidity premium in the bond market can be substantial, especially for bonds with high default risk. Insurance companies can reduce this liquidity premium by improving the overall liquidity of the market. Market makers, or dealers, can also significantly improve the liquidity of a market by acting as intermediaries who buy or sell securities to match traders' needs.

Military Life Insurance: Eligibility for Surviving Spouses

You may want to see also

Frequently asked questions

Insurance is a contract between two parties, you and the insurance company, and covers unforeseen or accidental loss. Bonds, on the other hand, involve a third party and cover acts that are done knowingly. Bonds are a guarantee of quality and provide a line of credit to ensure the principal fulfils their obligations.

Insurance is often a mandatory part of ownership and is required by law in many cases. It protects you from financial loss and offers peace of mind.

Bonds are often required by law and are necessary to reassure customers that they are dealing with a reputable business. They provide a financial guarantee that you will meet your contractual obligations.

The process for obtaining a surety bond is similar to getting a loan from a bank. You will need to provide business and personal information, including financial statements and references. For insurance, you will work with an agent to identify the type of business insurance you need, such as general liability or commercial property coverage.