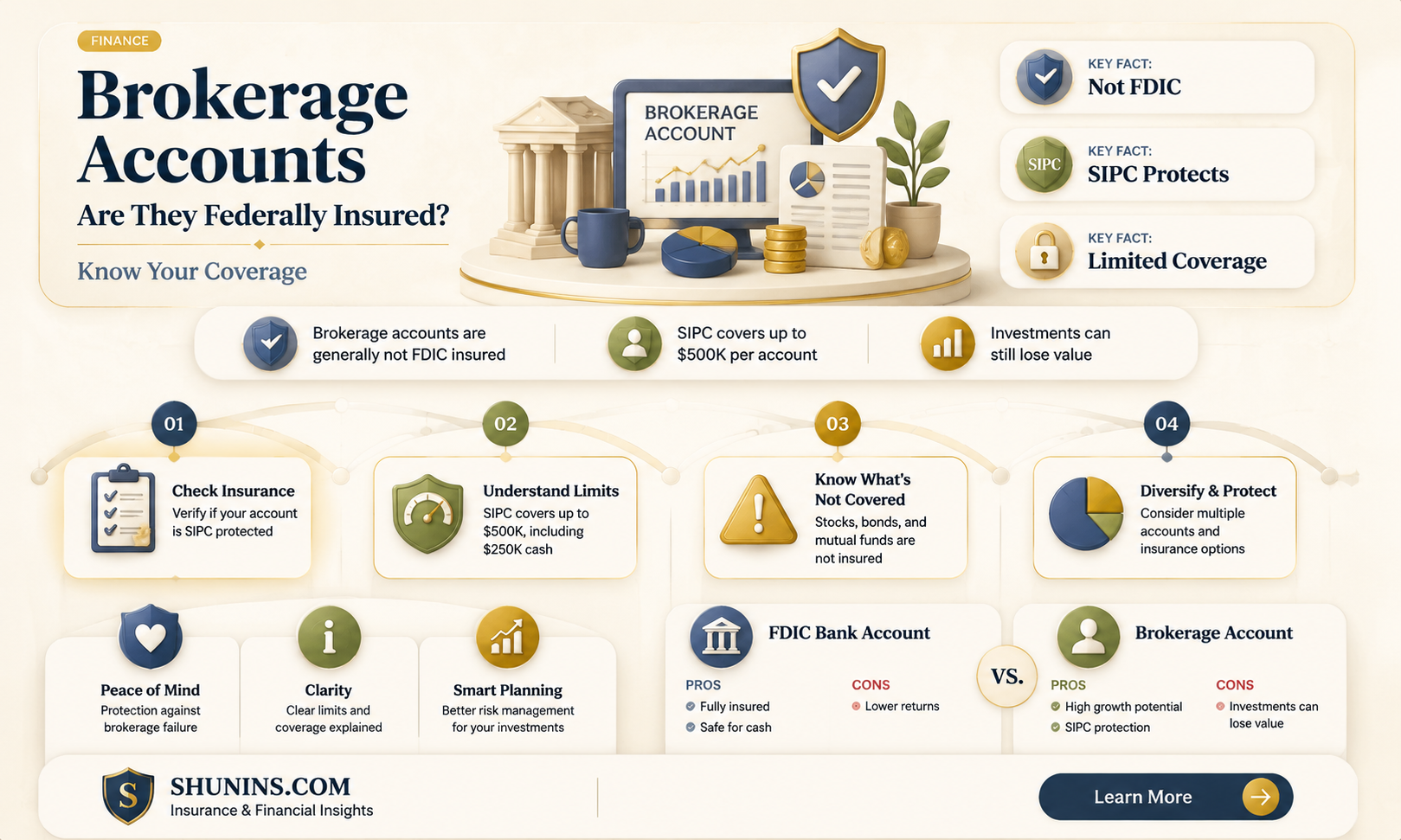

While brokerage accounts are not insured by the federal government, they are covered by the Securities Investor Protection Corporation (SIPC). The SIPC is a federally mandated, non-profit organisation that insures up to $500,000 in cash and securities per ownership capacity, including up to $250,000 in cash. This limit may increase depending on the number of accounts and the types of accounts held. The SIPC protects investors in the unlikely event that their brokerage firm fails and certain rules and conditions apply.

| Characteristics | Values |

|---|---|

| Are brokerage accounts insured by the federal government? | No, but they are insured by the Securities Investor Protection Corporation (SIPC) |

| Who does SIPC protect? | Investment account owners |

| Who does the Federal Deposit Insurance Corporation (FDIC) protect? | Deposit account owners |

| How much does SIPC insurance cover? | Up to $500,000 in securities, of which up to $250,000 can be cash balances per account |

| Are there circumstances where investors are covered for more than $500,000? | Yes, if investors have multiple accounts of different types, e.g. a traditional individual retirement account (IRA) and a Roth IRA at the same brokerage, the SIPC will insure them separately, providing up to $1 million coverage across the two accounts |

| Are there other types of protection? | Yes, some brokerages provide additional "excess of SIPC" coverage, which would be used when SIPC coverage is exhausted. |

| What does "excess of SIPC" coverage include? | There is no per-customer dollar limit on the coverage of securities, but there is a per-customer limit of $1.9 million on the coverage of cash awaiting investment |

| What does SIPC insurance not cover? | Regular investment losses, commodity futures contracts (unless held in a special portfolio margining account), foreign exchange trades, investment contracts (such as limited partnerships), fixed annuity contracts that are not registered with the U.S., and investment earnings |

Explore related products

What You'll Learn

![]()

SIPC insurance covers up to \$500,000 in securities and cash per account

The Securities Investor Protection Corporation (SIPC) is a federally mandated, non-profit organisation that insures investors for up to $500,000 in securities and cash per account. This includes up to $250,000 in uninvested cash. It is important to note that SIPC insurance does not protect against regular investment losses, such as a decline in the value of securities or losses due to a broker's bad investment advice. It also does not cover commodity futures contracts unless they are held in a special portfolio margining account.

SIPC insurance is designed to protect investors in the unlikely event that their brokerage firm fails. If a brokerage firm goes bankrupt or becomes insolvent, SIPC insurance will step in to make investors whole by recovering missing funds and returning them to customers. This process is supervised by the SIPC, which works with a court-appointed trustee to gather customer information and set up a process for claims to be filed.

Most brokerage firms are insured by the SIPC, and it is important for consumers to check if their brokerage is an SIPC member. SIPC membership provides reassurance that investments are protected up to the $500,000 limit in the event of brokerage failure. While SIPC insurance offers some peace of mind, it is important to understand its limitations and the specific types of assets that are covered and excluded from coverage.

It is worth noting that there are circumstances in which investors can be covered for more than $500,000. This typically occurs when investors have multiple accounts of different types, such as a traditional individual retirement account (IRA) and a Roth IRA at the same brokerage. In this case, the SIPC will insure each account separately, providing up to $1 million in total coverage.

Commercial Truck Insurance: What You Need to Know

You may want to see also

Explore related products

![]()

FDIC insurance covers up to \$250,000 per account

While brokerage accounts are not insured by the FDIC, the FDIC does insure bank deposits up to $250,000 per depositor, per FDIC-insured bank, for each account ownership category. This means that if you have a single ownership account in one FDIC-insured bank, and another single ownership account in a different FDIC-insured bank, you will be insured for up to $250,000 for each account. If you have multiple accounts in different ownership categories, you may qualify for more than $250,000 in insurance coverage. For example, if you have a single ownership account at an FDIC-insured bank, and you also have a joint ownership account with one or more people at the same bank, you will be insured for up to $250,000 for your single ownership account deposits and also insured separately for up to $250,000 for all of your joint ownership account deposits.

FDIC insurance covers the balance of each depositor's account, dollar-for-dollar, up to the insurance limit, including principal and any accrued interest through the date of the insured bank's failure. It's important to note that FDIC insurance does not cover investments, even if they were purchased at an insured bank.

In the unlikely event of a bank failure, the FDIC acts quickly to ensure that all depositors receive prompt access to their insured deposits. Since 1934, no depositor has lost any of their FDIC-insured funds. You can confirm that your bank is FDIC-insured by searching for it in the BankFind tool available on the FDIC website or by calling the FDIC.

It's worth noting that while brokerage accounts are not FDIC-insured, they may be SIPC-insured. The SIPC is a federally mandated, private non-profit organisation that insures up to $500,000 in cash and securities per ownership capacity, including up to $250,000 in cash. SIPC insurance protects investors in the unlikely event that their brokerage firm fails, but it does not cover investment losses. Most brokerage firms are insured by the SIPC, and you can check the SIPC database to confirm if your brokerage is a member.

The Art of Insurance Adjusting: Navigating the Complex World of Claims and Coverage

You may want to see also

![]()

Investment earnings are not insured

While brokerage accounts are insured by the Securities Investor Protection Corporation (SIPC), investment earnings are not insured. The SIPC is a federally mandated, private non-profit that insures up to $500,000 in cash and securities per ownership capacity, including up to $250,000 in cash. The SIPC steps in when a brokerage firm fails financially and assets are missing from customer accounts. It protects customer assets when a SIPC-member brokerage firm fails financially.

The SIPC does not protect against regular investment losses. If your securities decline in value, the SIPC will not bail you out. Similarly, if you purchase stocks or other securities that underperform, the SIPC will not cover your losses.

It is important to note that the SIPC is not the same as the Federal Deposit Insurance Corporation (FDIC). The FDIC is a U.S. government agency that insures cash deposits at FDIC-member banks, generally up to $250,000 per account. Unlike the FDIC, the SIPC does not provide blanket coverage. Instead, it protects customers of SIPC-member broker-dealers if the firm fails financially.

While brokerage accounts are SIPC-insured, it is essential to understand the limitations of this coverage. Investment earnings are not insured, and investors are responsible for any losses incurred due to market fluctuations or underperforming securities. Therefore, while SIPC insurance provides some peace of mind, it does not eliminate investment risk entirely.

Navigating the Claims Process: Hiring a National Insurance Adjuster

You may want to see also

![]()

SIPC protection does not cover investment losses

Brokerage accounts are insured by the Securities Investor Protection Corporation (SIPC), which is a federally mandated, private non-profit organisation. The SIPC protects investors if their brokerage firm fails, and the limit of SIPC protection is $500,000, which includes a $250,000 limit for cash.

However, SIPC protection does not cover investment losses. This means that if your securities decline in value, the SIPC will not bail you out. For example, if you purchased stocks that underperformed, the SIPC would not cover your losses. Similarly, if an advisor recommended stocks that lost value, the SIPC would not cover those losses.

SIPC protection also does not cover commodity futures contracts unless they are held in a special portfolio margining account. It also does not protect against foreign exchange trades or investment contracts that are not registered with the U.S. Securities and Exchange Commission.

It is important to note that SIPC insurance is not a substitute for careful research and due diligence when choosing a brokerage firm. While SIPC protection can provide some peace of mind, it does not eliminate all risk. Investors should be cautious and understand the limitations of SIPC protection before making any investment decisions.

In addition to SIPC protection, investors can also consider other layers of protection, such as working with a reputable brokerage firm that has robust risk management practices in place. Diversifying your investments across multiple institutions can also help minimise risk and ensure that your assets are protected.

The Art of Negotiation: Understanding Insurance Adjuster Tactics

You may want to see also

![]()

FDIC insurance covers deposit accounts, while SIPC covers investment accounts

The Federal Deposit Insurance Corporation (FDIC) and the Securities Investor Protection Corporation (SIPC) are two distinct types of insurance that protect your money in different ways. FDIC insurance covers deposit accounts, while SIPC covers investment accounts.

FDIC insurance protects your assets in a bank account, such as checking or savings accounts, at an insured bank. It covers depositors' accounts dollar-for-dollar, including principal and accrued interest, up to a limit of $250,000 per depositor, per insured bank, and per account ownership category. This means that an account holder could have multiple deposit accounts at different FDIC-insured banks, with each institution providing a separate $250,000 limit. FDIC insurance does not cover non-deposit investments or investment products, even if purchased at an insured bank.

On the other hand, SIPC insurance protects your assets in a brokerage account. It is a federally mandated, private non-profit corporation created by federal statute in 1970. SIPC steps in when a SIPC-member brokerage firm fails financially and assets are missing from customer accounts. It covers investors for up to $500,000 in securities, with up to $250,000 of that amount allowed to be cash balances. However, it's important to note that SIPC does not protect against regular investment losses or market losses. It also does not cover commodity futures contracts unless they are held in a special portfolio margining account.

While FDIC insurance covers deposit accounts, SIPC covers investment accounts, providing protection for investors in different scenarios. FDIC insurance offers peace of mind for deposit account owners, while SIPC provides a safety net for investment account owners in the unlikely event that their brokerage firm fails.

It is worth noting that there are instances where investors are SIPC-insured for more than $500,000, depending on how the accounts are held. For example, if an individual has a traditional IRA and a Roth IRA at the same brokerage, the SIPC will insure them separately, resulting in up to $1 million in coverage for both accounts.

Commercial Property Insurance: Understanding Grace Periods

You may want to see also

Frequently asked questions

No, brokerage accounts are not insured by the federal government. However, they are insured by the Securities Investor Protection Corporation (SIPC).

SIPC is a federally mandated, private, nonprofit corporation that was created by federal statute in 1970.

SIPC steps in when a brokerage firm fails financially and assets are missing from customer accounts. It protects customer assets when a SIPC-member brokerage firm fails financially.

SIPC insurance covers investors for up to $500,000 in securities, of which up to $250,000 can be cash balances. However, there are instances where investors are SIPC-insured for more than $500,000 depending on how the accounts are held.

SIPC does not cover regular investment losses, commodity futures contracts (unless held in a special portfolio margining account), foreign exchange trades, or investment contracts (such as limited partnerships) and fixed annuity contracts that are not registered with the U.S.