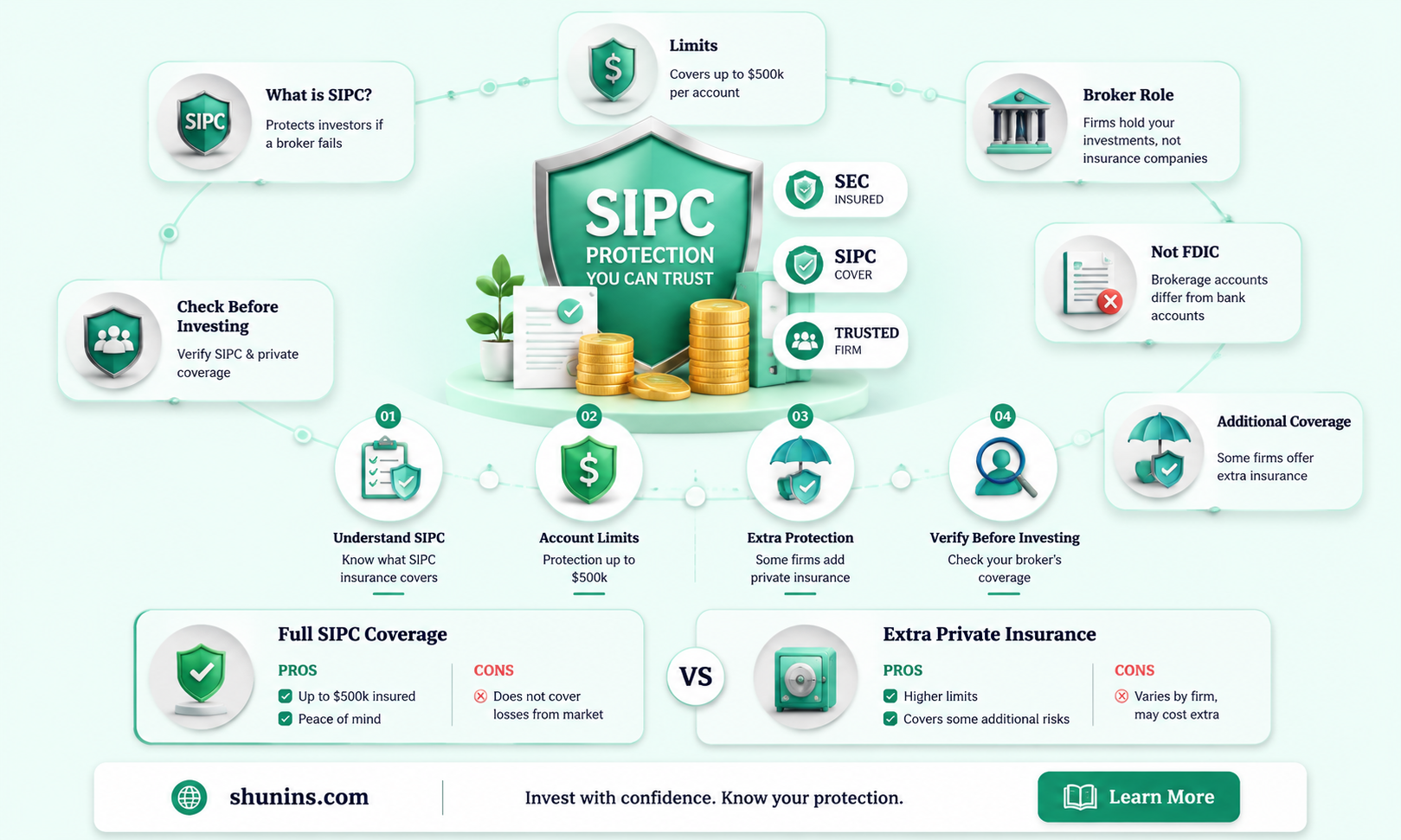

Brokerage firms are generally insured by the Securities Investor Protection Corporation (SIPC), which protects investors in the event that the firm fails. SIPC insurance covers up to \$500,000 in securities, with a \$250,000 limit on cash per account. It's important to note that SIPC insurance does not protect against regular investment losses or commodity futures contracts. FDIC insurance, on the other hand, protects your assets in a bank account, such as checking and savings accounts, but does not apply to brokerage accounts.

| Characteristics | Values |

|---|---|

| Type of insurance | SIPC insurance |

| Protection | Securities and cash in a brokerage account |

| Protection limit | $500,000 in securities, including a $250,000 limit on cash |

| Protection condition | If a brokerage firm fails financially |

| Protection condition | If a brokerage firm becomes insolvent |

| Protection condition | If assets are missing from customer accounts |

| Protection condition | If the firm is an SIPC member |

| Protection condition | If the customer files a claim |

| Exclusions | Regular investment losses |

| Exclusions | Commodity futures contracts (unless held in a special portfolio margining account) |

| Exclusions | Foreign exchange trades |

| Exclusions | Investment contracts (such as limited partnerships) |

| Exclusions | Fixed annuity contracts that are not registered with the U.S. |

Explore related products

What You'll Learn

![]()

SIPC insurance protects investors if a brokerage firm fails

Most brokerage firms are insured by the SIPC (Securities Investor Protection Corporation). This insurance protects investors in the event that a brokerage firm fails. The SIPC is a non-profit corporation that has been protecting investors for 50 years. It works to restore investors' cash and securities when their brokerage firm fails.

SIPC insurance covers investors for up to $500,000 in securities, with up to $250,000 of this amount being available to cover missing cash. It's important to note that SIPC insurance does not protect against regular investment losses. If the value of securities declines, the SIPC will not bail investors out. The SIPC also does not protect against losses due to a broker's bad investment advice or the recommendation of inappropriate investments.

To receive SIPC protection, investors must file a claim. SIPC protection is only available if a brokerage firm fails and the SIPC steps in. The SIPC has recovered billions of dollars for investors. It works to recover missing cash or securities if a brokerage firm has gone out of business.

SIPC insurance generally applies in the following situations:

- A brokerage firm goes bankrupt or becomes insolvent and is unable to return customer assets.

- A brokerage firm is in liquidation or in a direct payment procedure under the Securities Investor Protection Act.

Aflac Insurance Benefits: Are They Taxable or Not?

You may want to see also

Explore related products

![]()

FDIC insurance doesn't cover brokerage accounts

Brokerage firms are insured, but not by the Federal Deposit Insurance Corporation (FDIC). FDIC insurance covers depositors' accounts at each insured bank, including principal and any accrued interest, up to a limit of $250,000 per depositor, per insured bank, for each account ownership category. This means that an account holder with deposit accounts at two or more FDIC-insured banks could be covered at each institution by a separate $250,000 limit.

Instead, brokerage firms are insured by the Securities Investor Protection Corporation (SIPC). SIPC insurance covers investors for up to $500,000 in securities, with up to $250,000 of that amount covering cash balances. SIPC insurance is designed to protect investors in the event that their brokerage firm fails or becomes insolvent. It is important to note that SIPC insurance does not protect against regular investment losses or declines in the value of securities.

While FDIC insurance and SIPC insurance both aim to keep customers' money safe, they operate differently. FDIC insurance covers deposit accounts at insured banks, while SIPC insurance covers assets in brokerage accounts. FDIC insurance is provided by the US government, whereas SIPC is a non-profit membership corporation created by federal statute in 1970.

In summary, FDIC insurance does not cover brokerage accounts because it is designed to protect depositors' accounts at insured banks, while SIPC insurance is specifically designed to cover assets in brokerage accounts.

Globe Life Insurance: Contestability Clause Explained

You may want to see also

![]()

SIPC insurance doesn't cover regular investment losses

SIPC insurance, or the Securities Investor Protection Corporation, is a nonprofit membership corporation that was created by federal statute in 1970. It protects investors in the event that a SIPC-member brokerage firm fails financially. SIPC insurance covers investors for up to $500,000 in securities, with up to $250,000 of that amount covering cash.

However, SIPC insurance does not cover regular investment losses. This means that if your securities decline in value, SIPC will not compensate you for these losses. For example, SIPC does not protect against losses from market price changes or declines in the value of CDs (certificates of deposit). Similarly, SIPC does not protect against losses resulting from a broker's bad investment advice or inappropriate investment recommendations.

It is important to note that SIPC protection is different from the protection provided by the Federal Deposit Insurance Corporation (FDIC) for cash deposits at insured banks. FDIC insurance covers the failure of an insured bank, while SIPC insurance covers the failure of a brokerage firm.

Overall, while SIPC insurance provides valuable protection for investors, it is essential to understand that it does not cover all types of investment losses. Investors should carefully consider the limitations of SIPC insurance when making investment decisions and managing their financial portfolios.

Life Insurance Payments: Are They Considered Income?

You may want to see also

![]()

SIPC insurance covers up to $500,000 in securities

SIPC insurance covers investors for up to $500,000 in securities, with up to $250,000 of that amount covering cash balances. This means that if a brokerage firm fails financially and cannot return customer assets, SIPC insurance will step in to protect investors.

SIPC insurance is provided by the Securities Investor Protection Corporation (SIPC), a non-profit corporation created by federal statute in 1970. It is designed to protect investors in the event that their brokerage firm fails. SIPC insurance covers "securities" and cash in a brokerage account. Securities can include stocks, bonds, ETFs, mutual funds, and money market mutual funds.

It's important to note that SIPC insurance does not protect against regular investment losses. For example, if your securities decline in value or underperform, SIPC will not cover these losses. SIPC insurance also does not cover commodity futures contracts unless they are held in a special portfolio margining account.

SIPC insurance is similar to FDIC insurance, which protects your assets in a bank account. However, SIPC insurance is specifically designed for brokerage accounts, which are accounts for investing in securities. While FDIC insurance provides blanket coverage for each FDIC-insured bank, SIPC insurance covers each account with separate capacity held at a SIPC-member brokerage firm. This means that if you hold multiple accounts of the same type at the same firm, those accounts share the same overall limit.

Life Insurance Carrier: What You Need to Know

You may want to see also

![]()

Most brokerage firms are insured by the SIPC

Most brokerage firms are insured by the Securities Investor Protection Corporation (SIPC). The SIPC is a non-profit corporation that has been protecting investors for 50 years. It works to restore investors' cash and securities when their brokerage firm fails.

SIPC insurance generally applies when a brokerage firm goes bankrupt or becomes insolvent and is unable to return customer assets. It covers up to $500,000 in securities, with a $250,000 limit on cash per account with separate capacity held at a SIPC-member brokerage firm. Money market funds, often thought of as cash, are protected as securities by the SIPC.

It's important to note that SIPC insurance does not protect against regular investment losses or market price changes. It also does not cover commodity futures contracts unless they are held in a special portfolio margining account.

To benefit from SIPC protection, consumers need to file a claim with the SIPC to receive reimbursement. Most U.S. brokerage firms are required to be SIPC members, and non-members must disclose this information to their customers. You can check the SIPC database to see if your brokerage firm is a member.

Life Insurance and Legal Judgments: What's the Verdict?

You may want to see also

Frequently asked questions

Yes, most brokerage firms are insured by the SIPC (Securities Investor Protection Corporation).

SIPC insurance covers investors for up to $500,000 in securities, with a $250,000 limit on cash per account. It protects cash and securities in a brokerage account, including stocks, bonds, ETFs, and mutual funds.

SIPC insurance does not protect against regular investment losses. It also does not cover commodity futures contracts (unless held in a special portfolio-margining account), foreign exchange trades, investment contracts, or fixed annuity contracts that are not registered with the U.S. Securities and Exchange Commission.

Most U.S. brokerage firms are required to be SIPC members. You can check the SIPC database to see if your brokerage is a member. If they are a member, their website will likely indicate SIPC membership. Non-members are required to disclose that information to their customers.