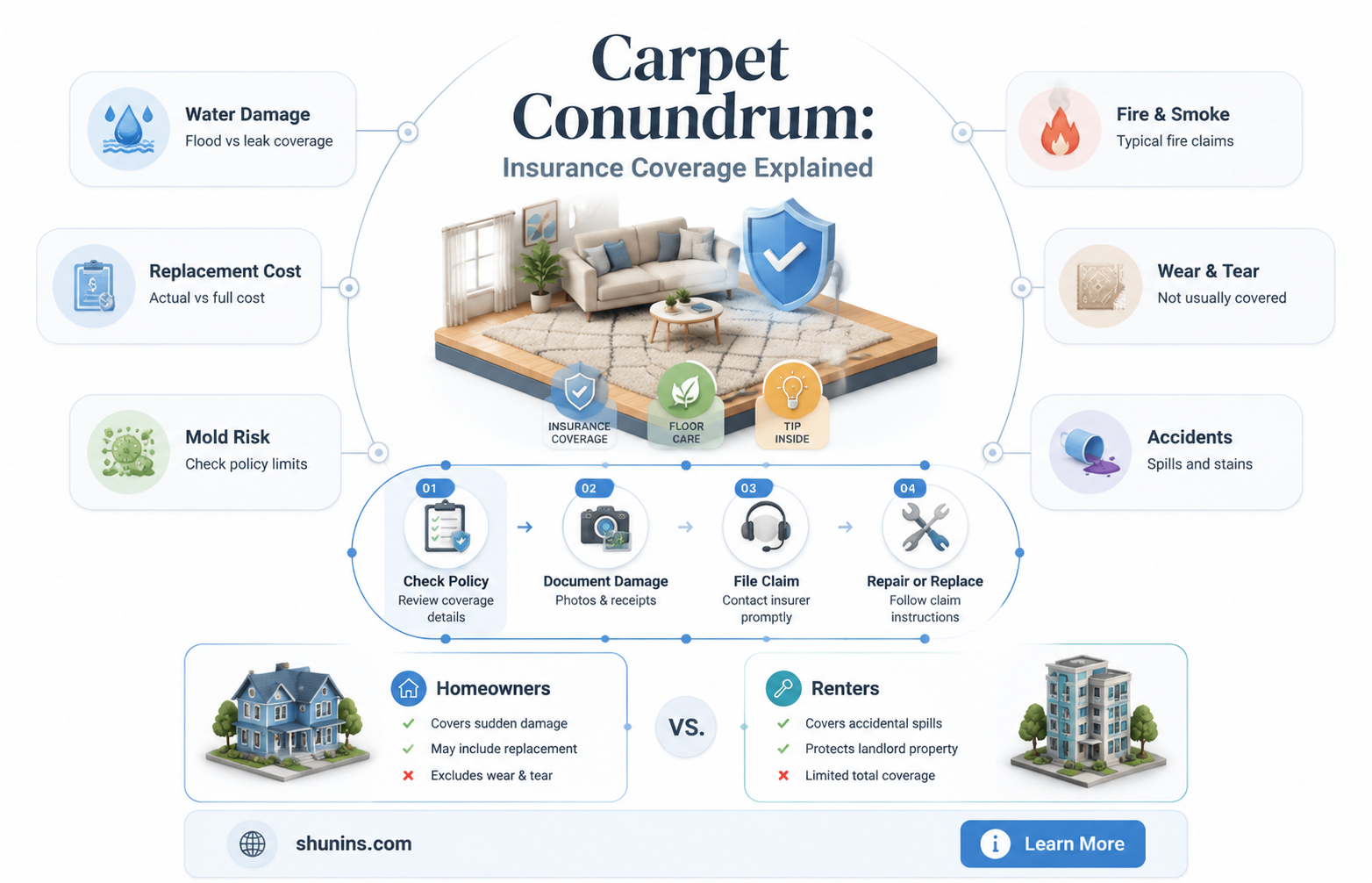

Carpets are usually covered by contents insurance, not buildings insurance. This is because they are not considered a permanent fixture and can be taken up and laid elsewhere. Contents insurance covers the financial cost of repairing or replacing household items such as furniture, appliances, clothing, and valuables. Buildings insurance, on the other hand, covers the physical structure of the property, including the walls, roof, floors, and permanent fixtures. While carpets are generally movable, other types of flooring like tiles, laminate, or vinyl that are glued or nailed down are usually covered by buildings insurance.

| Characteristics | Values |

|---|---|

| What does buildings insurance cover? | The physical structure of the property, including the walls, roof, floors, windows, and permanent fixtures like fitted kitchens and bathrooms. |

| What does contents insurance cover? | Items inside the property, including furniture, appliances, decorative items, clothing, and valuables. |

| Are carpets covered by buildings insurance? | Carpets are generally not covered by buildings insurance, as they are not considered a permanent fixture. However, if the carpet is glued to the floor, it may be considered part of the building and covered by buildings insurance. |

| Are carpets covered by contents insurance? | Carpets, including fitted carpets, are typically covered by contents insurance, as they can be rolled up and transported. Moveable rugs and mats are also usually covered. |

| What types of damage to carpets are covered by contents insurance? | Standard contents insurance typically covers carpet damage due to fire, flood, theft, and malicious scenarios. Accidental damage cover, including spills and DIY accidents, is often sold as an optional extra. |

| Are there any exclusions to carpet coverage under contents insurance? | Pet damage, including chewing, tearing, scratching, and fouling, is usually not covered by contents insurance. Antique or Persian rugs may require specialist cover. |

Explore related products

What You'll Learn

![]()

Carpets are usually covered by contents insurance

Contents insurance covers the cost of repairing or replacing household possessions and furnishings. This includes items such as furniture, appliances, clothing, and carpets. Carpets that are fitted but not glued in place are typically covered by contents insurance. Movable rugs and mats are also included in this category.

It is important to note that standard contents insurance may not cover accidental damage to carpets, such as spills or stains. To protect against these types of incidents, accidental damage cover can be purchased as an optional extra. This would cover damage caused by spills, stains, or DIY projects. However, it is important to take reasonable steps to protect carpets during DIY, such as using dust sheets, as negligence may result in a refused claim.

Additionally, most insurers do not cover carpet damage caused by pets or pest infestations. For tenants, any damage caused to a landlord's carpet is the tenant's responsibility to repair or replace. Tenants' liability insurance can cover these costs, and it is often included in renters' content cover. Landlords are responsible for replacing carpets if they pose a health or safety risk, such as in the case of damp, mould, or pest infestations.

Life Insurance for the Elderly: Options at 80 Years Old

You may want to see also

Explore related products

![]()

Buildings insurance covers the structure of your home

When purchasing buildings insurance, you will usually be asked how much it would cost to rebuild your home. This figure will determine the cover limit, which is the maximum amount an insurer will pay out. Some insurers offer unlimited cover, but these policies are usually more expensive. You can use the Building Cost Information Service online calculator on the Association of British Insurers' website to estimate the cost of rebuilding your home.

Buildings insurance will also usually cover external structures such as garages, sheds, fences, and outbuildings, as well as the cost of replacing items such as pipes, cables, and drains. The exact cover provided will vary between insurers and policies, so it is important to carefully read your policy and check what is included.

While buildings insurance covers the structure of your home, contents insurance covers the items inside your home, such as furniture, appliances, decorative items, and personal belongings. Carpets typically fall under contents insurance, even if they are fitted, as they can theoretically be rolled up and transported to another property. However, if a carpet is glued to the floor, it may be considered part of the building and covered under buildings insurance.

Disclaiming Life Insurance Benefits: What You Need to Know

You may want to see also

Explore related products

![]()

Contents insurance covers items inside the property

Contents insurance, also known as personal property insurance, provides financial protection for your belongings in the event of damage or theft. This includes items such as furniture, laptops, clothing, and other valuables. Most home insurance policies include contents insurance, typically covering 50-70% of the dwelling coverage amount listed on the policy.

The amount of contents insurance you need depends on the value of the personal property you want to protect. It's important to review your policy documents to understand the specific perils that are covered and excluded, as well as any additional coverage options available. For example, accidental damage cover is often sold as an optional extra and can protect against spills or stains on your carpet.

In the case of rented properties, landlords are responsible for repairing or replacing carpets if they pose a health or safety risk or if the damage is caused by external factors such as fire, theft, or pests. Tenants are generally responsible for any damage they directly cause to the carpet and can consider tenants' liability insurance or renters insurance to cover these instances.

Life Insurance: The Right Time to Sign Up

You may want to see also

Explore related products

![]()

Accidental damage cover is often sold as an add-on

Carpets usually fall under contents insurance. This is because, despite being fitted, they can theoretically be rolled up and transported to another property. However, if a carpet is glued to the floor, it may be covered under buildings insurance.

When it comes to spills on your carpet, a standard home contents insurance policy might not cover you. Typically, content insurance covers carpet damage in events like fire, flood, theft and malicious damage. Coverage for accidental spills is not always included as standard. Accidental damage cover is often sold as an optional extra and could protect your carpet from potential mishaps like spillage that stains, such as red wine or food.

Accidental damage cover can also protect your carpet from unforeseen DIY damage. For example, if you spill paint while painting without taking reasonable precautions, like putting down dust sheets, your claim may be refused on the grounds of negligence. Similarly, if you are doing major renovations, you must inform your insurance provider. With tradespeople around, the chance of damage rises, and your provider may need to extend your cover or charge a one-off fee that covers the renovation work.

If you are a tenant, you are responsible for any damage you cause to the carpet, even if it was accidental. You can take out tenants' liability insurance to cover these costs, which is generally included as standard in renters' content cover. If your carpets are damaged by tradespeople, they should have public liability insurance, which covers them for accidental damage to someone else's property.

Cancer and Life Insurance: Can You Get Covered?

You may want to see also

Explore related products

![]()

Landlord contents insurance covers carpets damaged by external factors

Generally, carpets are considered contents and are covered under contents insurance. This is because, despite being fitted, carpets can theoretically be rolled up and transported to another property. However, if a carpet is glued to the floor, it may be considered a part of the building and covered under buildings insurance.

When it comes to landlord contents insurance, carpets provided by the landlord are typically covered if they are damaged by external factors such as fire, theft, damp, mould, or pests. Landlord contents insurance can help cover the costs of repairing or replacing carpets in these situations.

It is important to note that landlord contents insurance typically does not cover accidental damage or wear and tear caused by tenants. If a tenant directly damages the carpet, such as by ripping, burning, or staining it, they are generally responsible for the costs of repair or replacement. Tenants may be able to claim on their tenant's liability insurance if they have it, or the landlord may deduct the costs from their security deposit.

Additionally, landlord contents insurance may not cover damage caused by pets, even with accidental damage cover included. It is possible to find more comprehensive policies that cover pet damage, but they typically come with a higher premium.

To summarise, landlord contents insurance can provide financial protection for landlords by covering the costs of repairing or replacing carpets damaged by external factors. However, it is essential to carefully review the policy's inclusions and exclusions, as different insurers may have varying coverage options.

Term Life Insurance: Renewing Your Policy and Options

You may want to see also

Frequently asked questions

Buildings insurance covers the physical structure of a property, including the walls, roof, floors, windows, and permanent fixtures like fitted kitchens and bathrooms. Contents insurance covers items inside the property, including furniture, household goods, and personal belongings.

Carpets, even fitted ones, are generally covered by contents insurance. This is because they can be rolled up and transported to another property. However, if a carpet is glued to the floor, it may be covered by buildings insurance.

Standard contents insurance typically covers carpet damage in events like fire, flood, theft, and malicious damage. Coverage for accidental spills like wine or paint is not always included and may require additional contents accidental damage cover.

If you are a tenant, your landlord may have a landlord's contents insurance policy that covers the cost of repairing or replacing a carpet damaged by external factors such as fire, theft, damp, mould, or pests. Tenants can also take out tenants' liability insurance, which is sometimes included in renters' content cover.