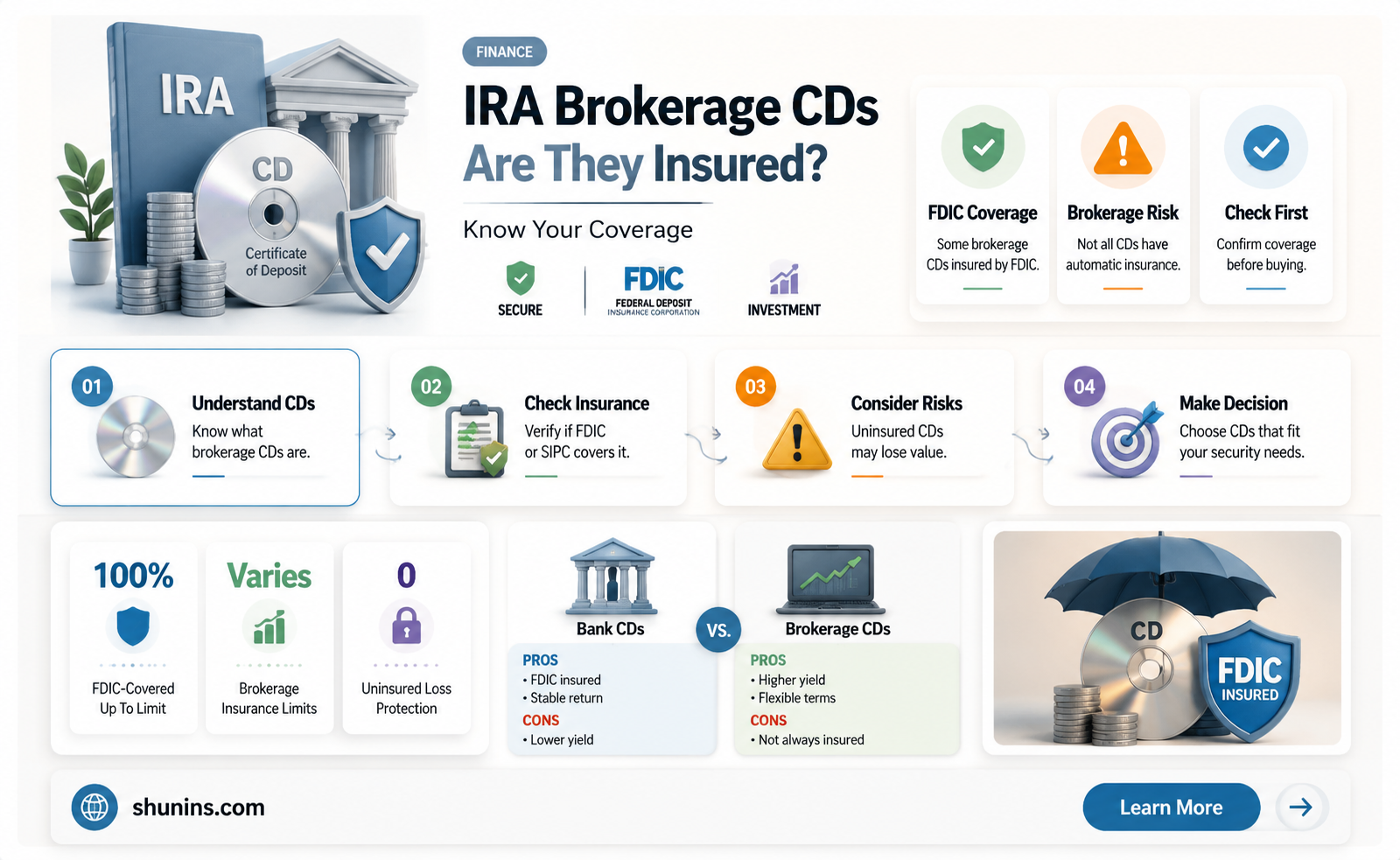

Certificates of deposit (CDs) are fixed-income investments that generally pay a set rate of interest over a fixed time period. Brokered CDs are like bank CDs, but instead of being purchased directly through the issuing bank, you buy them through brokerage firms. Brokered CDs are insured by the Federal Deposit Insurance Corporation (FDIC) or National Credit Union Administration (NCUA) up to $250,000 per depositor, per account. Brokered CDs can be held in different investment accounts, including IRAs, and are suitable for those who are risk-averse or approaching retirement.

| Characteristics | Values |

|---|---|

| Definition | Brokered CDs are like bank CDs, but instead of being purchased directly through the issuing bank, you buy them through brokerage firms. |

| Purchase | Brokered CDs may be purchased directly from banks or through secondary trades with another market participant. |

| Investment minimum | $1,000, with additional purchases in increments of $1,000. |

| Fee | $1 transaction fee per $1,000 CD ($250 maximum). |

| Broker-assisted fee | $25 for secondary trades placed over the phone. |

| FDIC insurance | FDIC insurance does not cover market losses. However, brokered CDs are FDIC-insured up to $250,000 per depositor, per account. |

| IRA CDs | You can open IRA CDs at banks, credit unions and brokerage firms. |

| Annual contribution limits | For 2025, you can contribute up to $7,000 and an extra $1,000 if you're age 50 or older. |

Explore related products

What You'll Learn

- Brokered CDs are FDIC insured up to $250,000 per depositor, per bank

- Brokered CDs are like bank CDs but bought through brokerage firms

- Brokered CDs are available to buy through Vanguard and Fidelity

- Brokered CDs are subject to the same FDIC insurance limits as bank-issued CDs

- Brokered CDs can be held in different investment account types, including IRAs

![]()

Brokered CDs are FDIC insured up to $250,000 per depositor, per bank

Brokered CDs are FDIC-insured, which means that your investments are protected up to $250,000 per depositor, per bank. FDIC insurance does not cover market losses, but it does protect your initial investment. This insurance covers both bank CDs and brokered CDs. Brokered CDs are purchased through brokerage firms, whereas bank CDs are purchased directly from the issuing bank. Brokered CDs offer the same benefits as bank CDs, including FDIC insurance, a broad selection of terms, and the ability to be held in various investment accounts, including IRAs.

Brokered CDs are issued by banks for customers of investment and brokerage firms. They are bank deposits that offer an interest rate for a certain period, with the issuing bank agreeing to return your money on a specific date. Brokered CDs can be purchased without a separate transaction fee, and they offer the potential for higher yields than some high-yield savings accounts and money market funds.

It is important to note that CDs may be sold on the secondary market prior to maturity, which may result in a substantial gain or loss. In such cases, the original face amount of the purchase is not guaranteed. Additionally, CDs purchased on the secondary market at a premium to their principal value are ineligible for FDIC insurance.

When considering CDs for retirement savings within an IRA, it is important to evaluate your personal investment goals, retirement time frame, and risk tolerance. While CDs offer a safe and stable investment option with guaranteed returns, they may not provide returns as high as stocks or exchange-traded funds (ETFs). IRAs have annual contribution limits, and early withdrawals may trigger penalties from both the financial institution and the IRS.

Life Insurance: Dividing Policies and Understanding the Process

You may want to see also

Explore related products

![]()

Brokered CDs are like bank CDs but bought through brokerage firms

Brokered CDs, or brokered certificates of deposit, are similar to bank CDs in many ways. They are both fixed-income investments, offering a set interest rate over a fixed time period. However, the key difference is that while bank CDs are purchased directly from a bank, brokered CDs are bought through brokerage firms.

Brokered CDs are issued by banks for customers of investment and brokerage firms. They are bank deposits that offer an interest rate for a specific period, and the issuing bank agrees to return your money, along with the interest, on a specific date. Brokered CDs are bought and sold through a dealer network.

Brokered CDs offer some of the same benefits as bank CDs, such as being steady and predictable. They also provide FDIC insurance and a broad selection of terms (maturity dates). Brokered CDs can be held in various investment accounts, including IRAs, and offer terms ranging from one month to 20 years or more.

One advantage of brokered CDs is that they provide access to multiple banks' CDs, allowing investors to shop around for competitive rates. Additionally, brokered CDs generally command a higher yield than bank CDs as they are in a more competitive market. The broker invests a large sum with the bank, which generates more interest than smaller amounts.

However, it's important to note that brokered CDs may cost more to obtain than bank CDs due to higher transaction costs. These costs depend on the specific brokerage and the services it offers. When considering brokered CDs, it's essential to review the fine print and understand the potential risks involved.

Finding a Life Insurance License: Resume Essentials

You may want to see also

Explore related products

![]()

Brokered CDs are available to buy through Vanguard and Fidelity

Vanguard's brokered CDs are bought and sold through a dealer network of over 100 dealers nationwide. They can be callable, meaning the issuing bank could terminate the CD before maturity, or noncallable, which can't be called back by the issuing bank before maturity. They also offer Jumbo CDs, which are certificates with a minimum denomination of $100,000 that provide a higher rate than regular CDs. All CDs offered by Vanguard Brokerage are FDIC-insured up to $250,000 per account owner per institution for depository assets.

Fidelity also offers brokered CDs, which can be purchased through multiple brokers. They are available through their affiliate National Financial Services LLC and from various third-party providers. Fidelity Brokerage Services LLC will charge a markup or markdown if you want to buy or sell a CD on the secondary market. They offer an Auto Roll Program, which can help you maintain your income stream by reinvesting the CD's maturing principal, or investing in multiple CDs of varying maturities. Brokered CDs through Fidelity can sometimes offer better rates because these brokers negotiate these rates in bulk, but this is not guaranteed as rates fluctuate.

Life Insurance Benefits for Teachers: What You Need to Know

You may want to see also

![]()

Brokered CDs are subject to the same FDIC insurance limits as bank-issued CDs

Brokered CDs are FDIC insured for up to $250,000 per depositor, per bank, just like bank CDs. This limit applies to both brokered and bank CDs, and the FDIC aggregates accounts held at the issuer, including those held through different broker-dealers or other intermediaries. This means that if you have multiple brokered CDs from different banks, each held within a single brokerage account, your coverage limit will still be $250,000 per bank.

The FDIC insurance limit of $250,000 per depositor, per bank, applies to both brokered and bank CDs. This limit is set by the FDIC and is the maximum amount that will be insured in the event of a bank failure. It's important to note that this limit applies per depositor, per bank, so if you have CDs at multiple banks, you will be covered up to $250,000 at each bank.

While brokered CDs offer the convenience of accessing multiple banks' CDs through a single brokerage account, it's important to understand that they are still subject to the same FDIC insurance limits as bank-issued CDs. This means that your deposits are fully insured up to $250,000 per depositor, per bank. Therefore, when considering brokered CDs, it's essential to stay within the FDIC limits and guidelines to ensure your deposits are fully insured.

The Future of Insurance: Alternative Insurance Options

You may want to see also

![]()

Brokered CDs can be held in different investment account types, including IRAs

Brokered CDs are like bank CDs, but instead of being purchased directly from the issuing bank, they are bought through brokerage firms. Brokered CDs offer some of the same benefits as bank CDs, such as FDIC insurance, a broad selection of terms (maturity dates), and the ability to be held in a variety of investment accounts, including IRAs.

Brokered CDs can be purchased through a broker, providing access to multiple banks and CDs, competitive rates, and assistance with renewals. They are also more convenient than a single bank and offer the same FDIC protection as bank-issued CDs. Brokered CDs are also tax-free, as the money is not withdrawn from your IRA to buy them.

When considering whether to put brokered CDs in your IRA, it's important to keep in mind your investment goals, retirement time frame, and risk tolerance. While brokered CDs are generally considered safe investments, they may not offer the same high returns as other investment options. Additionally, early withdrawals from CDs in an IRA can trigger steep penalties from both the financial institution and the IRS.

It's also important to note that while FDIC insurance typically covers brokered CDs, it does not cover market losses. The FDIC insurance limit is $250,000 per depositor, per bank.

Zakat and Life Insurance: What's the Verdict?

You may want to see also

Frequently asked questions

Brokerage CDs in an IRA are typically insured by the Federal Deposit Insurance Corporation (FDIC) or National Credit Union Administration (NCUA) for up to \$250,000 per depositor, per account.

Brokerage CDs offer a safe investment option with a guaranteed rate of interest. They also provide the added benefit of tax-deferred earnings growth.

While brokerage CDs offer stability, their returns may not keep up with inflation over the long term. Additionally, early withdrawals may trigger penalties from both the financial institution and the IRS.