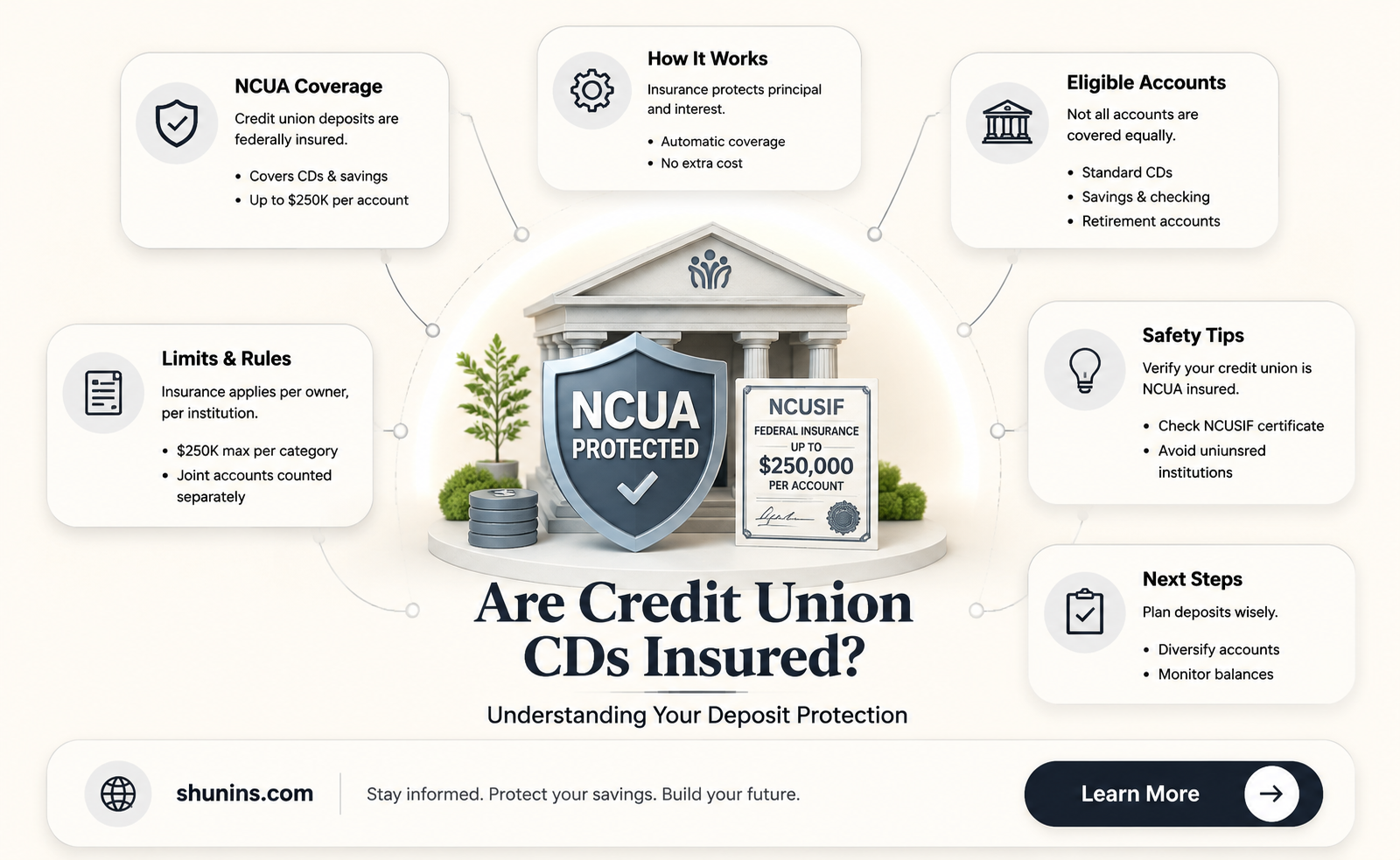

When considering where to deposit funds, many individuals wonder about the safety of their money, especially in the case of CDs (Certificates of Deposit). A common question is whether CDs at credit unions are insured. The good news is that, like banks, credit unions offer federal insurance on deposits, including CDs, through the National Credit Union Administration (NCUA). This insurance protects up to $250,000 per depositor, per insured credit union, for each account ownership category, providing peace of mind for those looking to invest in CDs at credit unions. This protection ensures that even if the credit union were to fail, depositors’ funds would remain secure, making credit union CDs a safe and reliable investment option.

| Characteristics | Values |

|---|---|

| Insurance Provider | National Credit Union Administration (NCUA) |

| Coverage Limit | Up to $250,000 per depositor, per insured credit union, per ownership category |

| Eligibility | Federally insured credit unions (look for NCUA logo or confirmation) |

| Types of CDs Covered | Traditional CDs, IRA CDs, and most share certificates |

| Non-Covered Accounts | Investments, mutual funds, stocks, bonds, or non-deposit products |

| Ownership Categories | Single, joint, retirement (e.g., IRA), revocable trust, etc. |

| State-Chartered Credit Unions | May be insured by NCUA or private insurers (confirm with the institution) |

| FDIC vs. NCUA | NCUA is the equivalent of FDIC for credit unions |

| Duration of Coverage | Continuous as long as the credit union remains federally insured |

| Claim Process | Automatic; NCUA handles payouts if a credit union fails |

| Latest Data Source | NCUA official website (as of October 2023) |

Explore related products

What You'll Learn

![]()

FDIC vs. NCUA Insurance

When considering where to invest in certificates of deposit (CDs), understanding the insurance coverage provided by financial institutions is crucial. In the United States, two primary entities insure deposits: the Federal Deposit Insurance Corporation (FDIC) and the National Credit Union Administration (NCUA). Both organizations offer similar protections but cater to different types of financial institutions. The FDIC insures deposits at banks, while the NCUA insures deposits at credit unions. This distinction is essential for investors looking to safeguard their funds, especially in CDs, which are long-term commitments.

FDIC Insurance covers deposits at banks, including CDs, up to $250,000 per depositor, per insured bank, for each account ownership category. This means if you have multiple CDs at the same bank, their combined value is insured up to the $250,000 limit. The FDIC’s coverage extends to various types of accounts, such as checking, savings, and money market accounts, in addition to CDs. It’s important to note that the $250,000 limit applies separately to different ownership categories, such as individual accounts, joint accounts, and retirement accounts, allowing depositors to maximize their insured amounts by strategically diversifying their account types.

NCUA Insurance, provided by the National Credit Union Share Insurance Fund (NCUSIF), offers similar protection for credit union members. Like the FDIC, the NCUA insures deposits, including CDs, up to $250,000 per share owner, per insured credit union, for each account ownership category. This coverage applies to credit union accounts such as share draft (checking), share (savings), and money market accounts, as well as CDs. The NCUA’s insurance structure mirrors the FDIC’s, allowing members to exceed the $250,000 limit by holding accounts in different ownership categories.

One key difference between FDIC and NCUA insurance lies in the nature of the institutions they cover. Banks, insured by the FDIC, are typically for-profit entities owned by shareholders, while credit unions, insured by the NCUA, are not-for-profit cooperatives owned by their members. This distinction can influence the types of services and rates offered, with credit unions often providing more favorable terms on CDs and other products due to their member-focused model.

For investors, the choice between a bank CD insured by the FDIC and a credit union CD insured by the NCUA often comes down to personal preference, rates, and the specific terms of the CD. Both types of insurance provide robust protection, ensuring that your funds are safe up to the $250,000 limit per depositor or share owner. It’s advisable to verify the insurance status of any financial institution before investing, as not all banks or credit unions are insured by the FDIC or NCUA. Additionally, understanding how different account ownership categories can maximize your insured amounts is a smart strategy for protecting your investments in CDs.

In summary, both FDIC and NCUA insurance offer strong protections for CD investors, with the primary difference being the type of institution they cover. Whether you choose a bank CD or a credit union CD, your funds are insured up to $250,000 per ownership category, providing peace of mind for long-term investments. By understanding these insurance mechanisms, investors can make informed decisions to safeguard their financial future.

Affordable Life Insurance: Best Low-Cost Options

You may want to see also

Explore related products

![]()

Coverage Limits for CDs

When considering Certificates of Deposit (CDs) at credit unions, understanding the coverage limits for these insured products is crucial. In the United States, credit union CDs are typically insured by the National Credit Union Administration (NCUA) through the National Credit Union Share Insurance Fund (NCUSIF). This insurance provides protection similar to that of the Federal Deposit Insurance Corporation (FDIC) for banks. The standard coverage limit for CDs at credit unions is $250,000 per depositor, per insured credit union, for each account ownership category. This means that if you have multiple CDs under different ownership categories, such as individual accounts, joint accounts, or retirement accounts, each category is insured separately up to $250,000.

It’s important to note that the $250,000 coverage limit applies to the total of all deposits held by a depositor at a single credit union, including CDs, savings accounts, and checking accounts. For example, if you have a $100,000 CD and a $150,000 savings account at the same credit union under the same ownership category, the entire $250,000 is insured. However, if your total deposits exceed $250,000 in a single ownership category, the excess amount will not be covered. To maximize insurance coverage, depositors can strategically spread their funds across different ownership categories or even across multiple credit unions.

For joint accounts, the $250,000 coverage limit applies to each co-owner, providing additional protection. For instance, a joint CD account with two owners would be insured up to $250,000 for each owner, totaling $500,000 in coverage. This makes credit union CDs an attractive option for couples or families looking to safeguard larger sums of money. Similarly, retirement accounts, such as IRAs, are treated as separate ownership categories, allowing depositors to extend their coverage beyond the standard limit.

Credit union CDs held in trust accounts also benefit from separate coverage limits. Depending on the type of trust and the number of beneficiaries, these accounts may qualify for additional insurance. Revocable trust accounts, for example, can be insured up to $250,000 per beneficiary, up to a maximum of five beneficiaries, potentially providing up to $1.25 million in coverage. Understanding these nuances is essential for depositors looking to fully leverage the insurance benefits offered by credit unions.

Finally, it’s worth mentioning that while the NCUA insurance covers CDs at credit unions, not all financial products offered by credit unions are insured. For example, investments in stocks, bonds, or mutual funds are not covered by NCUA insurance. Depositors should carefully review the terms of their accounts and ensure that their funds are allocated in a way that maximizes insurance protection. By staying informed about coverage limits and ownership categories, individuals can confidently invest in credit union CDs, knowing their funds are secure.

Life Insurance Trusts: Tax Returns and Legalities

You may want to see also

Explore related products

![]()

Joint Account Protection

When considering joint account protection, particularly in the context of CDs (Certificates of Deposit) at credit unions, it's essential to understand the insurance coverage provided. In the United States, credit unions are insured by the National Credit Union Administration (NCUA), which operates the National Credit Union Share Insurance Fund (NCUSIF). This insurance protects members' deposits, including those in joint accounts, up to $250,000 per depositor, per insured credit union, for each account ownership category. For joint accounts, this means that each co-owner is insured separately, effectively doubling the coverage to $500,000 for a jointly owned CD.

In addition to the basic joint account protection, credit union members can further enhance their insurance coverage by structuring their accounts strategically. For instance, a married couple can hold a CD jointly, providing $500,000 in coverage, and also maintain individual CDs or other eligible accounts, each insured up to $250,000. This allows for a total of $1 million in coverage across different account ownership categories. Understanding these nuances is vital for maximizing the benefits of NCUA insurance while ensuring joint account protection.

It’s important to note that not all joint accounts are structured equally, and the specific terms of ownership can impact insurance coverage. For example, accounts titled as "joint tenants with right of survivorship" are treated differently from those held as "tenants in common." The former ensures equal ownership and automatic transfer of assets to the surviving owner, while the latter allows for unequal shares and does not automatically transfer ownership. Credit union members should consult with their financial institution to ensure their joint accounts are titled correctly to receive full NCUA insurance protection.

Finally, while NCUA insurance provides robust protection for joint accounts, including CDs, it’s advisable for account holders to regularly review their account structures and balances. This ensures compliance with NCUA insurance limits and maximizes coverage. Credit unions often provide tools and resources to help members understand their insurance coverage, and members should take advantage of these to protect their joint accounts effectively. By staying informed and properly structuring their accounts, joint account holders can enjoy peace of mind knowing their funds are secure and insured.

U.S.A.A. Life Insurance Rates: Competitive or Not?

You may want to see also

![]()

Credit Union Failure Risks

One of the primary risks of credit union failure stems from financial mismanagement or economic downturns. Credit unions, like any financial institution, can face challenges such as poor lending practices, insufficient capital reserves, or exposure to high-risk investments. During economic recessions, credit unions may experience increased loan defaults, reducing their ability to meet financial obligations. Members with CDs or other deposits must be aware that while their funds are insured, the failure of a credit union could lead to temporary disruptions in accessing their money until the NCUA steps in to resolve the situation.

Another risk factor is the smaller scale and limited resources of some credit unions compared to larger banks. Credit unions often serve specific communities or groups, and their size can make them more vulnerable to localized economic shocks. For instance, a credit union heavily reliant on a single industry or geographic area may face significant challenges if that industry declines or the local economy suffers. Members should research the financial health and stability of their credit union, including its capitalization and asset quality, to mitigate these risks.

Despite these risks, it is important to note that credit union failures are relatively rare due to regulatory oversight and the conservative nature of their operations. The NCUA regularly examines credit unions to ensure compliance with financial standards and takes corrective action when necessary. Additionally, the NCUSIF has a strong track record of protecting depositors, with no loss of insured funds since its inception. However, members should remain vigilant and diversify their deposits across different institutions or account types to further minimize risk.

In the event of a credit union failure, the NCUA typically resolves the situation by merging the failed institution with a healthier one or by paying out insured deposits directly to members. While this process is designed to be seamless, it can still cause inconvenience or uncertainty for depositors. Therefore, staying informed about your credit union’s financial health and understanding the insurance protections in place are crucial steps in managing credit union failure risks. By doing so, you can ensure that your CDs and other deposits remain secure, even in the unlikely event of a credit union failure.

Life Insurance Options for People with Lung Cancer

You may want to see also

![]()

Insurance Claim Process

When dealing with CDs (Certificates of Deposit) at credit unions, understanding the insurance claim process is crucial, as these financial products are indeed insured, providing a safety net for your investments. The insurance coverage for credit union CDs is primarily provided by the National Credit Union Administration (NCUA), which is the independent federal agency that oversees and insures credit unions in the United States. This insurance is similar to the FDIC (Federal Deposit Insurance Corporation) coverage for banks, ensuring that your money is protected.

Initiating the Insurance Claim Process: In the unlikely event that a credit union fails, the insurance claim process for your CD begins automatically. The NCUA is notified, and they step in to manage the situation. As a CD holder, you don't need to file a claim yourself. The NCUA's first step is to find a healthy credit union to assume the failed institution's accounts, including CDs. This means your CD will be transferred to the new credit union, and you'll continue to earn interest without any interruption. If a purchasing credit union cannot be found, the NCUA will pay you directly.

Understanding Coverage Limits: It's essential to know the insurance limits to ensure your funds are fully protected. The NCUA insures CDs up to $250,000 per depositor, per insured credit union, for each account ownership category. This means if you have multiple CDs in different ownership categories, such as individual and joint accounts, each category is insured separately up to the $250,000 limit. For example, if you have a $200,000 CD in your name and a $150,000 joint CD with your spouse, both are fully insured.

Receiving Your Insured Funds: If the NCUA needs to pay you directly, they will do so within a few days of the credit union's closure. You'll receive a check for the insured amount, ensuring you get your money back promptly. It's important to keep your contact information updated with your credit union to facilitate a smooth process in case of such an event. The NCUA also provides resources and assistance to answer any questions you may have during this time.

Additional Considerations: While the insurance claim process is straightforward, it's beneficial to stay informed about your credit union's financial health. Regularly reviewing their financial reports and staying updated on any news can provide peace of mind. Additionally, diversifying your investments across different institutions and account types can further safeguard your funds, ensuring you maximize insurance coverage across various categories. Understanding these processes and limits empowers you to make informed decisions about your CD investments in credit unions.

Mid-Policy Life Insurance: Can You Re-up?

You may want to see also

Frequently asked questions

Yes, CDs at credit unions are insured by the National Credit Union Administration (NCUA) through the National Credit Union Share Insurance Fund (NCUSIF), up to $250,000 per depositor, per insured credit union, for each account ownership category.

NCUA insurance for credit union CDs is equivalent to FDIC insurance for bank CDs. Both provide coverage up to $250,000 per depositor, per institution, for each account ownership category, ensuring similar protection for depositors.

Yes, all traditional CDs offered by NCUA-insured credit unions are covered, including fixed-rate, variable-rate, and callable CDs, as long as they meet the eligibility criteria for share insurance.

If a credit union fails, the NCUA will step in to ensure you receive your insured funds up to $250,000. You may also have the option to transfer your CD to another insured credit union or receive payment for the insured amount.

Yes, NCUA insurance covers CDs in joint accounts and trusts, but the coverage limits may vary depending on the ownership category. For example, joint accounts with two or more owners are insured separately from individual accounts, potentially increasing the total coverage.