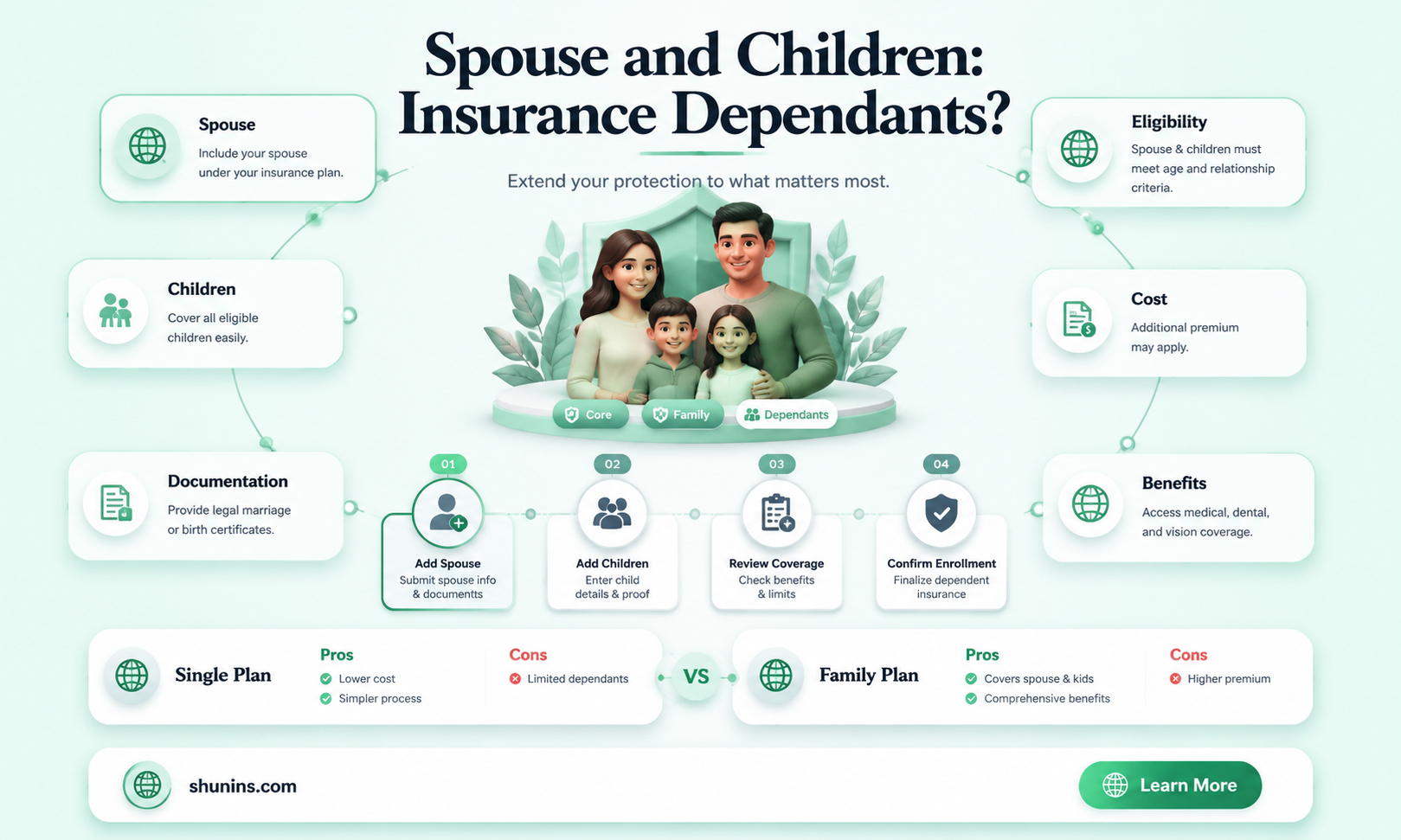

A dependent is someone who is eligible to be added to a policyholder's health insurance coverage. This can include a spouse, domestic partner, or child. In most cases, biological children, adoptive children, stepchildren, and foster children are all considered dependents, as long as they meet age and other eligibility criteria. Generally, insurance coverage for dependent children extends until they reach the age of 26 or until they no longer financially depend on you. A current spouse is often eligible to be added as a dependent, but ex-spouses usually are not.

| Characteristics | Values |

|---|---|

| Who can be added as a dependent? | Spouse, children, domestic partner, parents (in rare cases), siblings (in rare cases), non-family members (in rare cases) |

| Child age limit | Up to 26 years old |

| Child eligibility | Biological, adopted, stepchildren, foster children, grandchildren, adult children with a disability |

| Spouse eligibility | Current spouse, common-law spouse, same-sex spouse |

| Other eligibility | Legal guardianship, extenuating circumstances, civil unions, unique circumstances |

| Additional considerations | Length of residency, income contribution, tax filing, other claims, marital status, school enrolment, employer-based coverage |

Explore related products

What You'll Learn

![]()

Children: biological, step, foster, and adoptive

When it comes to health insurance, a dependent is someone who is eligible to be added to a policyholder's insurance coverage. The policyholder is typically the individual who has primary eligibility for coverage, such as an employee whose employer offers health insurance benefits. Dependents can receive the benefits of the policyholder's health insurance plan and use it in much the same way.

Children, including biological, step, foster, and adoptive children, are generally considered dependents on their parents' or guardians' health insurance plans. This also extends to grandchildren and adult children with disabilities. To be considered a dependent, a child must meet certain criteria, including age requirements, financial dependence, and length of residency.

The specific requirements for children as dependents may vary depending on the insurance provider and the type of policy. However, here are some general guidelines:

- Age: The child must be under a certain age, typically up to 26 years old, to be considered a dependent.

- Relationship: The child must be the policyholder's biological, step, adopted, or foster child.

- Length of Residency: The child must have lived with the policyholder for at least six months to qualify as a dependent.

- Financial Dependence: The child's income must be less than half of their support expenses to qualify as a dependent.

- Tax Filing: The child cannot be claimed as a dependent if they file a joint tax return for the same year.

- Other Claims: A child cannot be claimed as a dependent by more than one household.

It is important to note that insurance policies may have different criteria for dependents, so it is advisable to review the specific terms of your health insurance plan to understand the eligibility requirements for adding children as dependents.

Unraveling the Maryland Bridge Insurance Billing Process

You may want to see also

Explore related products

![]()

Spouse eligibility

Eligibility Criteria

In most cases, a person's current spouse is eligible to be added as a dependent on their health insurance plan. This is a standard provision across various insurance providers and policies. However, it is important to note that eligibility criteria may vary, so reviewing the specific terms of your policy is crucial.

Timeframe for Enrollment

After getting married, there is usually a designated timeframe, often up to 60 days, to enroll your spouse as a dependent on your insurance plan. This timeframe is crucial to ensure continuous coverage for your spouse.

Tax Implications

While you cannot claim your spouse as a dependent on your federal income tax return, they may still be considered a dependent in a broader financial sense. This distinction is important, as it can impact tax credits and deductions. Consult with a tax professional to understand how your marital status affects your tax obligations and benefits.

Impact of Divorce

In the unfortunate event of a divorce, an ex-spouse is generally no longer eligible for dependent coverage under your insurance plan. They will need to obtain their own insurance coverage, possibly through options like COBRA or the health insurance marketplace.

Special Circumstances

It is worth noting that certain unique circumstances may allow for exceptions. For example, if your spouse has special needs or disabilities that make them reliant on you for financial or medical support, some health plans might recognize them as eligible dependents.

Employer-Sponsored Insurance

If you have access to employer-sponsored health insurance, it is essential to understand the specific rules and limitations regarding dependent coverage. Consult with your employer's human resources department to explore the available options for spouse eligibility.

Open Enrollment and Qualifying Events

Similar to health insurance, spouse coverage for life insurance can typically only be purchased during open enrollment or after certain qualifying events, such as marriage. Understanding these enrollment periods is crucial for ensuring continuous coverage for your spouse.

In summary, spouse eligibility as a dependent varies depending on the insurance provider and the specific policy. It is essential to carefully review the terms of your insurance plan and consult with professionals to ensure you make informed decisions regarding coverage for your spouse.

Understanding the Benefits of a Children's Term Insurance Rider

You may want to see also

Explore related products

![]()

Coverage limits

When it comes to insurance coverage limits for dependents, there are several factors to consider. Firstly, the type of insurance policy and the specific terms of the plan play a crucial role in determining coverage limits. Let's explore the coverage limits for different types of insurance and their impact on dependents:

Health Insurance Coverage Limits:

Health insurance policies typically set a maximum age limit for dependent coverage. In most cases, dependent children can remain on their parents' or guardians' health insurance plans until they reach the age of 26. This provision is mandated by the Affordable Care Act, ensuring young adults have access to essential healthcare services during critical transitional periods, such as graduating from college or starting their careers. It is important to note that the coverage may end on the dependent's 26th birthday or at the end of the year they turn 26, depending on the specific insurance plan.

Additionally, health insurance plans may have different criteria for qualifying as a dependent. Biological, adopted, and stepchildren are generally considered dependents. In some cases, foster children, grandchildren, adult children with disabilities, or children under the legal guardianship of the insured may also qualify as dependents. The length of residency requirements, income contribution limits, and tax filing status may also impact the eligibility of dependent children.

Spouses are usually eligible for dependent coverage, while ex-spouses are typically not considered dependents after a legal divorce. Domestic partners or same-sex partners may be covered as dependents, depending on the insurance plan and state laws.

Life Insurance Coverage Limits:

Life insurance policies also offer dependent coverage options, typically including spouses and children. Similar to health insurance, many life insurance plans consider children as dependents until they reach the age of 26. Some plans may offer coverage for other adult dependents, such as elderly parents or domestic partners, but this is less common.

Dependent life insurance coverage amounts are generally limited to a lower amount compared to individual policies. These coverage limits vary by insurer and plan, with maximum coverage amounts specified per eligible dependent. Spouses often have higher coverage limits compared to children. Additionally, the cost of dependent life insurance coverage may differ based on the number of dependents and their ages, with rates typically increasing as the dependent ages.

Other Considerations:

It is important to note that insurance plans may have specific exceptions and limitations. For example, dependent coverage may end if the dependent gets married, gains access to their employer's insurance, or reaches a certain age. Additionally, divorce or separation can impact the coverage of spouses, and special circumstances may apply for dependents with disabilities. Therefore, it is essential to carefully review the specific terms and conditions of your insurance plan to understand the coverage limits and any applicable exceptions.

The Intricacies of Dwelling Insurance: Unraveling the Concept of 'Dwelling' in Property Coverage

You may want to see also

Explore related products

$26.38 $29.34

![]()

Adding parents

In most cases, you won't be allowed to add your parents to your health insurance. Typically, health plans consider spouses and children as dependents, but parents aren't usually eligible for dependent coverage. However, there are some situations in which you may be able to add your parents as dependents on your health insurance.

Legal Guardianship

If you have legal guardianship of your parents due to incapacitation or other reasons, some providers may allow you to add them to your health insurance policy as dependents.

Extenuating Circumstances

If your parents have special needs or disabilities that make them rely on you for financial or medical support, certain health plans might consider your parents eligible dependents.

Tax Dependents

If you claim your parents as dependents on your federal income tax return, some health plans might allow you to add them to your insurance. The Inland Revenue Service (IRS) has strict eligibility requirements for declaring parents as tax dependents:

- They must be citizens or residents of the United States

- Their gross income must be less than $4,300 per year

- They cannot be someone else's legal dependent

- You must provide for more than half of their financial needs per year

State Laws

State laws may also impact your ability to add your parents to your health insurance. For example, in California, a new state law allows adult children to add their dependent parents or stepparents to their health plan policy if they are not eligible for or enrolled in Medicare and live in the health plan's service area.

Employer-Sponsored Plans

If you have a private, employer-sponsored health care plan, your HR department will be a good resource to learn about your options for adding your parents as dependents. Criteria may include your parents living with you, being claimed on your tax return as a dependent, or the adult child being financially responsible for the parent.

If your parents are not eligible for dependent coverage on your health insurance, you can explore other options such as enrolling them in a separate health plan through the Marketplace or Medicare (if they are 65 or older).

The Renewal Riddle: Unraveling the Mystery of Level Term Insurance

You may want to see also

Explore related products

![]()

Other adult dependents

While children and spouses are typically considered dependents for insurance purposes, other adult dependents may also be eligible for coverage under certain circumstances.

In most cases, health insurance plans consider spouses and children as dependents, but parents aren't usually eligible for dependent coverage. However, there are some situations in which you can add your parents to your health insurance as dependents. For example, if you have legal guardianship of your parents due to incapacitation or other reasons, some providers may allow you to add them as dependents. Additionally, if your parents have special needs or disabilities that make them rely on you for financial or medical support, certain health plans might consider them eligible dependents.

It's important to note that the criteria for dependents can vary among insurance providers and policies, so it's always a good idea to consult with your provider or employer to understand the specific requirements and benefits offered.

Navigating a Doctor Change with AR Kids First Insurance: A Step-by-Step Guide for Parents

You may want to see also

Frequently asked questions

Yes, your current spouse is often eligible to be added as a dependent on your health insurance plan. Once a marriage is legally ended through divorce, the ex-spouse is no longer considered a dependent.

Yes, biological children, adoptive children, stepchildren and foster children are all normally considered dependents, as long as they meet age and other eligibility criteria. Generally, insurance coverage for dependent children extends until they reach the age of 26, or until they no longer financially depend on you.

In most instances, you won’t be allowed to add your parents as dependents. Typically, health plans consider spouses and children as dependents, but parents aren’t usually eligible for dependent coverage. However, there are some exceptions, such as if you have legal guardianship of your parents or if they have special needs or disabilities that make them reliant on you for financial or medical support.