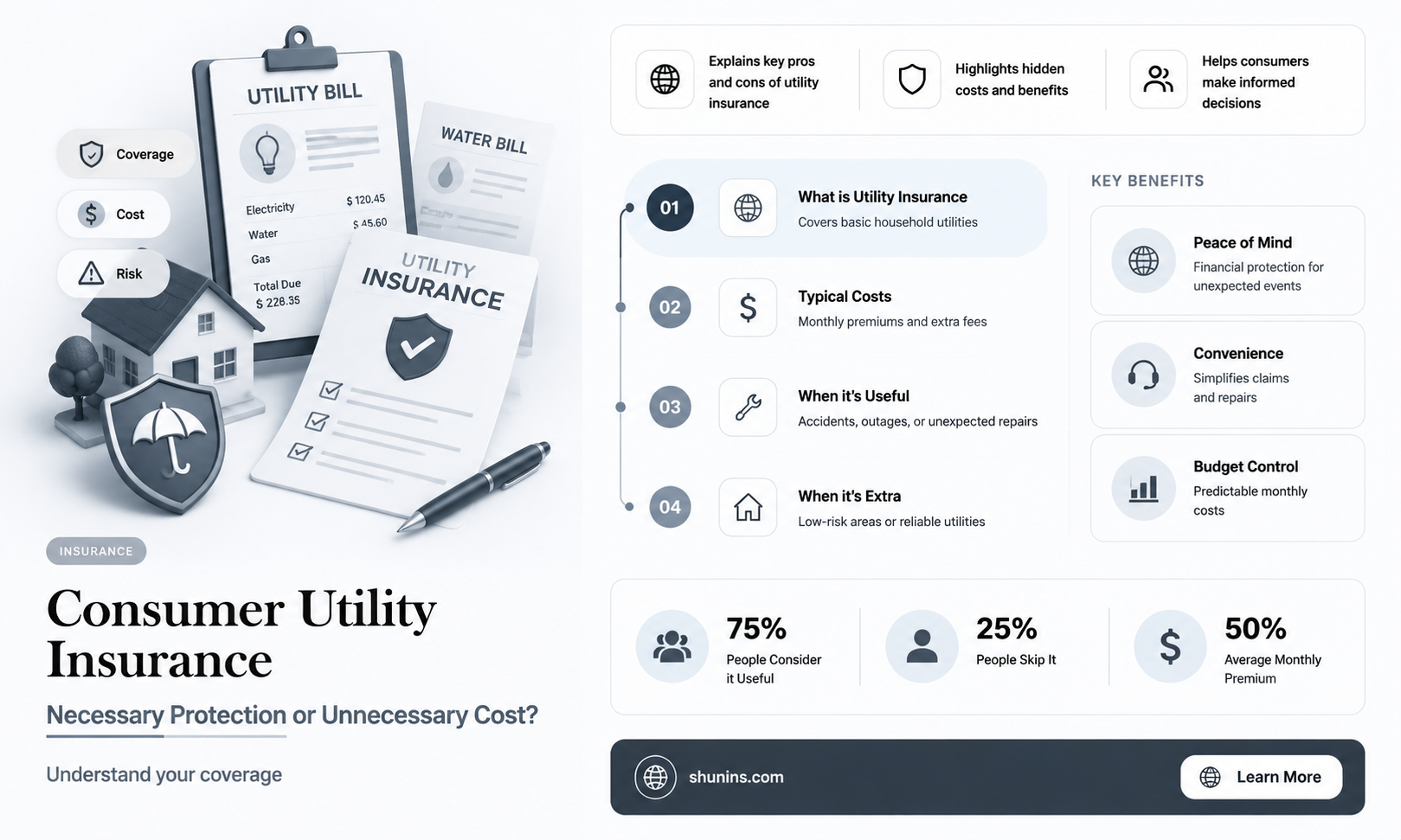

Utility bills are a necessary part of running a household, but are consumer utility insurance plans necessary? Utility companies often send notices warning homeowners that they are responsible for repairs to water and sewer lines on their property, and that such repairs could cost thousands of dollars. These notices, however, are often pitches from third-party companies that have partnered with utility providers to sell their warranty plans. While line protection plans are not required for utility service, consumers must decide whether to enroll in such plans based on their unique circumstances. This decision should be made carefully and with full knowledge of what is and is not covered by the plan and whether their homeowners insurance covers utility line replacements.

| Characteristics | Values |

|---|---|

| Necessity of consumer utility insurance | Not necessary as part of the infrastructure of running your house |

| Utility bills | Monthly or bi-monthly statements of the amount owed by a household for essential services that keep a home operational |

| Examples of utility bills | Water, electricity, gas, mobile data |

| Utility line protection plans | Voluntary and unregulated by the Indiana Utility Regulatory Commission (IURC) |

| Considerations before enrolling in a utility line protection plan | Likelihood of utility line problems, whether homeowners insurance covers utility line replacements, living in a rental property |

| Concerns with utility line protection plans | Overpriced, potential for unnecessary repairs, unclear coverage and responsibility |

Explore related products

What You'll Learn

![]()

Utility insurance is not a necessity for running your home

Insurance does not generally fall under the category of utility bills. While utilities are essential for running your home, insurance is not part of this infrastructure. It is possible to sustain your life without insurance.

Some utility companies may send notices warning homeowners that they are responsible for costly repairs to water and sewer lines on their property. These notices may seem official but are often pitches from third-party companies partnering with utility providers to sell their warranty plans. While these plans are voluntary, they are typically overpriced and may not be necessary.

Before considering a utility line protection plan, it is important to carefully review your homeowners' insurance policy. In some cases, your insurance may already cover utility line replacements, making additional insurance redundant. It is also crucial to understand the fine print of any warranty plan, including coverage limits, deductibles, and exceptions.

In conclusion, while utilities are essential for the functioning of a home, utility insurance is not a necessity. Homeowners can make informed decisions by reviewing their existing coverage and carefully considering the terms and conditions of any additional protection plans.

Becoming a Life Insurance Agent in California: A Guide

You may want to see also

Explore related products

![]()

Consumers are not required to purchase line protection plans

Line protection plans are offered by third-party companies that partner with utility providers to sell warranty plans to their customers. These companies use utility company letterheads and logos to make their notices seem official and create a sense of urgency, warning homeowners that they are responsible for costly repairs to water and sewer lines on their property.

However, before enrolling in such a plan, consumers should carefully consider their unique circumstances and make an informed decision. It is crucial to read the fine print and understand what is covered, whether there are deductibles or maximum limits on repairs, and who will carry out the repairs. Consumers should also check if their homeowners insurance policy already covers utility line replacements, as this would make a separate line protection plan unnecessary.

Additionally, line protection plans may come with additional fees, such as sign-up charges or early termination penalties. Therefore, consumers should be cautious and weigh their options before signing up for these plans. While they can provide peace of mind, they may also be overpriced for the coverage they offer. Ultimately, the decision to purchase a line protection plan rests with the consumer, taking into account the potential risks and costs associated with utility line repairs.

Health Insurance: A Key to Longevity?

You may want to see also

Explore related products

![]()

Peace of mind policies are often overpriced

Before enrolling in a utility line warranty plan, consumers should carefully consider their unique circumstances and read the fine print to understand what is and is not covered, including any deductibles, maximum limits, and exceptions. In some cases, homeowners insurance may already cover utility line replacements, making a separate line protection plan unnecessary.

Similarly, "peace of mind" policies for services like RideTo's Compulsory Basic Training (CBT) course are available but may not offer significant benefits beyond the standard training. While the policy covers individuals who fail to complete the course due to issues like balance, clutch control, or steering, it does not cover late arrivals or failures due to eyesight requirements. The policy may save individuals money if they need an additional day of training, but it is not an insurance policy or guaranteed pass.

Ultimately, individuals should weigh the costs and benefits of these policies and assess their own risk tolerance. While it is important to have insurance to protect against financially catastrophic risks, such as house fires or auto accidents, paying for coverage of unlikely repairs that one can afford may not be necessary. This is especially true if the cost of the peace of mind policy exceeds the potential savings or benefits gained from having the additional coverage.

Life Insurance and Short-Form Death Certificates: What's Accepted?

You may want to see also

Explore related products

![]()

Homeowners insurance may already cover utility line replacements

Utility line protection plans are not mandatory for consumers. These plans are also not regulated by entities such as the Indiana Utility Regulatory Commission (IURC). Consumers are advised to carefully review the terms of such plans before enrolling, including the likelihood of needing repairs, whether their homeowners insurance covers utility line replacements, and whether there are maximum limits on payouts for repairs.

Homeowners insurance policies typically do not cover service line damage, meaning repairs or replacements needed due to service line damage are the responsibility of the homeowner. However, some insurance companies now offer service line coverage as an optional add-on to homeowners insurance policies. Service line coverage insures against unexpected costs related to the damage of service lines on one's property, including power lines, phone and cable lines, water and sewer pipes, and more.

Service line coverage may also cover excavation and landscaping costs, as well as the repair and replacement of wiring and piping. In the event of a covered service line failure, some insurance providers will pay up to 150% of the cost of replacing with like-kind and quality using environmentally friendly materials. The deductible for service line coverage is typically around $500 per occurrence, and coverage usually applies to breakage caused by the weight of equipment, animals, or people.

The decision to enroll in a utility line warranty plan or purchase service line coverage depends on individual circumstances. Homeowners should carefully review their homeowners insurance policy to determine whether utility line replacements are covered and consider the likelihood of needing repairs. If their insurance covers replacements, a separate line protection plan may be unnecessary.

Get a Life Insurance License: Missouri Requirements

You may want to see also

Explore related products

![ESSENTIAL Car Auto Insurance Registration BLACK Document Wallet Holders 2 Pack - [BUNDLE, 2pcs] - Automobile, Motorcycle, Truck, Trailer Vinyl ID Holder & Visor Storage - Strong Closure On Each -](https://m.media-amazon.com/images/I/61px7jy3NmL._AC_UL320_.jpg)

![]()

Third-party companies use utility company branding to sell warranty plans

Millions of US homeowners receive official-looking notices with warnings that they are responsible for repairs to water and sewer lines on their property. These notices seem to come from utility companies but are actually from third-party companies that have partnered with utility providers. Through these partnerships, third-party companies are allowed to use utility company branding to sell their warranty plans.

Utility companies that partner with warranty providers lend their names and logos to these companies in exchange for a share of the premiums. For example, a warranty company working with the San Francisco Public Utilities Commission (SFPUC) paid it $3.61 every month for each enrolled policy, with plans sold for $12.99 a month. This means that 28% of the premiums collected went to the SFPUC.

Many utilities that partner with warranty companies say they direct their shares of sales to a good cause. For instance, a spokesperson for Washington (State) Water Service stated that the warranty fees they receive are recycled back to their customers and used for company-related projects.

However, these "peace of mind" policies are typically overpriced, and it is important to carefully consider whether such a plan is necessary. Consumers should check whether their homeowners' insurance covers utility line replacements, as well as the likelihood that their utility lines will need repairs.

New York Life Insurance: Is It Worth the Hype?

You may want to see also

Frequently asked questions

A utility bill is a monthly invoice sent by a utility company or service provider to consumers for using their services. Water, electricity, gas, and mobile data are some standard services that provide utility bills to users.

No, insurance premiums are generally not included in utility bills. Utility bills are for essential services that are necessary for running your household. Insurance is not considered part of this infrastructure.

Utility line protection plans are not necessary for everyone. It is a personal choice based on individual circumstances. It is recommended to check if your homeowner's insurance covers utility line replacements, in which case a separate protection plan may be unnecessary.

No, these plans are not regulated by bodies such as the Indiana Utility Regulatory Commission (IURC). Therefore, it is important to carefully review the terms and conditions before enrolling in such a program.

Consider factors such as the age of your home, whether it still has original utility lines, and whether your neighbours have needed repairs. If you live in a rented property, discuss this with your landlord and review your lease.

![Life Insurance Lottery [DVD]](https://m.media-amazon.com/images/I/717EhWE0rqL._AC_UL320_.jpg)