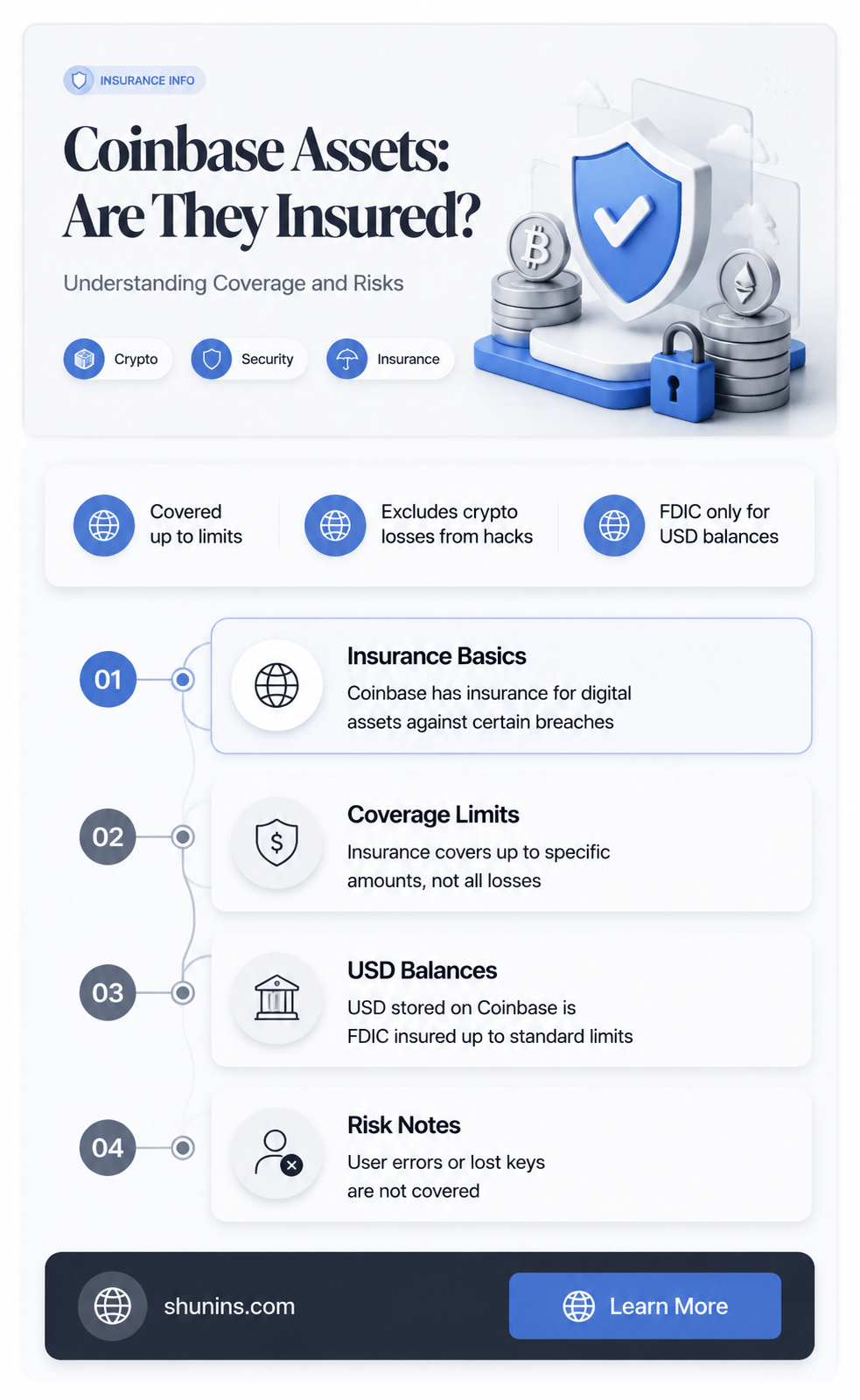

Coinbase users have often wondered whether their assets are insured. Coinbase holds insurance against theft or loss of its bitcoin, and the company has been insured for almost a year. The insurance covers losses due to breaches in physical or cyber security, accidental loss, and employee theft. It is important to note that the insurance does not cover bitcoin lost or stolen due to a user's negligence in maintaining secure control over their login credentials. Additionally, Coinbase's crime insurance protects a portion of digital assets and currencies held across its storage systems against losses from theft, including cybersecurity breaches. While Coinbase is not an FDIC-insured bank, its U.S. customers' funds are held in pooled custodial accounts at FDIC-insured banks or NCUSIF-insured credit unions, providing pass-through insurance coverage of up to $250,000 per depositor.

| Characteristics | Values |

|---|---|

| Crime insurance | Covers a portion of digital assets held across storage systems against losses from theft, including cybersecurity breaches |

| Coverage limit | $250,000 per depositor |

| Insurance provider | Aon, the world's largest insurance broker |

| Underwriters | High credit ratings (S&P rating of A+ or A.M. Best Rating of A XV or higher) |

| Customer funds | Maintained in pooled custodial accounts at FDIC-insured banks or NCUSIF-insured credit unions |

| Pass-through insurance | May be available to protect funds held on behalf of a Coinbase customer if the insured financial institution fails |

| Non-US customers | Funds are held as cash in dedicated custodial accounts separate from Coinbase funds |

| Exclusions | Losses resulting from unauthorized access due to a breach or loss of user credentials are not covered |

Explore related products

What You'll Learn

![]()

Coinbase's crime insurance policy

Coinbase, Inc. and its subsidiaries are covered by Coinbase Global, Inc.'s crime insurance policy. This policy protects a portion of the digital currencies held across Coinbase's storage systems against losses from theft, including cybersecurity breaches. However, it is important to note that the policy does not cover any losses resulting from unauthorized access to personal or business Coinbase accounts due to a breach or loss of credentials. Non-fungible tokens are also not covered by this policy.

For US customers, Coinbase combines customer balances with the balances of other customers and holds those funds in custodial accounts at US financial institutions. They may also invest these funds in liquid US Treasuries, USD-denominated money market funds, or other permissible investments, in accordance with state money transmitter laws. For non-US customers, funds are held as cash in dedicated custodial accounts separate from Coinbase funds.

Additionally, Coinbase has established custodial accounts at FDIC-insured banks or NCUSIF-insured credit unions for US customer funds held as cash. This allows Coinbase to make a claim against pass-through FDIC or NCUSIF insurance for each customer up to the per-depositor coverage limit, which is currently $250,000 per depositor. This pass-through insurance provides additional protection for customer funds in the event of a failure of any insured financial institutions where Coinbase maintains custodial accounts.

Valuation in Life Insurance: Why It's Essential

You may want to see also

Explore related products

![]()

Insurance against theft and hacking

Coinbase is insured against theft and hacking, but this insurance only covers a portion of the digital currencies held across its storage systems. The insurance covers losses due to physical or cybersecurity breaches, accidental loss, and employee theft. It does not cover losses from unauthorised access to personal or business accounts, such as phishing, stolen credentials, or SIM swapping. It also does not cover non-fungible tokens.

Coinbase's insurance policy is provided through a combination of third-party insurance underwriters and Coinbase itself as a co-insurer. The policy amount is greater than the value of the digital currency maintained in online storage at any given time.

It is important to note that Coinbase does not insure individual user accounts. While Coinbase protects its platform, users are responsible for maintaining the security of their login credentials and using strong passwords. Users can take additional steps to protect their accounts, such as keeping their recovery phrase offline and securing their devices and online accounts.

To protect against broader digital threats, users can subscribe to additional services like Aura, which offers up to $1 million in identity theft insurance and additional security features like credit file locking and financial fraud scanning.

Sarcoidosis: Life Insurance Considerations and Impacts

You may want to see also

Explore related products

![]()

FDIC-insured banks for US customers

Coinbase is not an FDIC-insured bank, and digital currency is not insured or guaranteed by the Federal Deposit Insurance Corporation (FDIC). However, for US customers, Coinbase holds their balances in custodial accounts at one or more FDIC-insured banks or NCUSIF-insured credit unions. These custodial accounts are established in a way that allows Coinbase to make an insurance claim for each customer, up to a specific coverage limit (currently $250,000 per depositor). This pass-through FDIC insurance coverage protects Coinbase customers' funds if an FDIC-insured bank where Coinbase maintains custodial accounts fails.

It is important to note that this FDIC insurance coverage is contingent on Coinbase maintaining accurate records and the determinations of the relevant federal regulator at the time of a bank failure. Additionally, while Coinbase has crime insurance policies to cover losses from theft or cybersecurity breaches, it does not cover losses from unauthorised access due to a breach of user credentials. Therefore, customers are responsible for maintaining strong passwords and securing their login credentials.

Coinbase combines US customers' balances with balances from other customers and invests these funds in various permissible investments, including US Treasuries and money market funds, as per state money transmitter laws. These investments are made to ensure the safety and liquidity of customers' funds. However, it is essential to understand that cryptocurrency is not legal tender and is not backed by the government, so it may lose value.

While Coinbase provides certain protections and insurance measures for its customers' funds, it is not equivalent to FDIC insurance for individual accounts. The FDIC insurance coverage only applies to the extent that US customer funds are held in cash at FDIC-insured banks. Therefore, customers should carefully review Coinbase's insurance policies and understand the risks associated with investing in cryptocurrencies.

Life Insurance: MLM or Legit?

You may want to see also

Explore related products

![]()

Non-US customers' funds

Coinbase is not an FDIC-insured bank, and digital currency is not insured or guaranteed by the Federal Deposit Insurance Corporation (“

For non-US customers, funds are held as cash in dedicated custodial accounts separate from Coinbase funds. Coinbase will not use these funds for its operating expenses or any other corporate purposes. It is important to note that the availability of pass-through insurance is contingent upon Coinbase maintaining accurate records and the determination of the relevant federal regulator at the time of a receivership of a bank or credit union holding a custodial account.

While Coinbase has insurance in the event of a security breach, it only covers a small fraction of the total crypto value they hold. Therefore, if a hack or theft is significant, they may not have sufficient funds to cover all customer losses. Additionally, if an individual's account is hacked, Coinbase is not responsible for covering those losses.

To enhance the security of their funds, Coinbase users, including non-US customers, can consider utilizing a cold storage device or hardware wallet. By purchasing and using a cold storage device, individuals can take control of their Bitcoin balance and ensure their funds remain secure even if Coinbase experiences operational issues or insolvency.

Monthly Insurance Quotes: How Much Do They Cost?

You may want to see also

Explore related products

![]()

Insurance for stablecoin bootstrap fund

Coinbase, Inc. and its subsidiaries are covered by Coinbase Global, Inc.'s crime insurance, which protects a portion of the digital currencies held across its storage systems from theft, including cybersecurity breaches. However, this policy does not cover losses from unauthorised access to personal or business Coinbase accounts due to a breach or loss of credentials, and it does not cover non-fungible tokens. Coinbase is not an FDIC-insured bank, and digital currencies are not insured or guaranteed by the Federal Deposit Insurance Corporation (FDIC), the National Credit Union Share Insurance Fund (NCUSIF), or the Securities Investor Protection Corporation (SIPC).

Coinbase has launched a second Stablecoin Bootstrap Fund, managed by Coinbase Asset Management (CBAM), to deepen stablecoin liquidity in DeFi capital markets. The fund will be placed with protocols including Aave, Morpho, Kamino, and Jupiter, with the goal of enabling users to access reliable rates across mature and emerging protocols.

The price of insuring stablecoins can be estimated using standard option pricing methods applied to bank deposit insurance. As crypto assets, stablecoins have raised financial stability concerns, and their collapses have resembled traditional bank runs. Insuring stablecoins similarly to bank deposits, with a third-party guarantee to cover losses in the event of a collapse, has been proposed as a risk mitigation strategy. The Federal Deposit Insurance Corporation (FDIC) is studying whether certain stablecoins might be eligible for its coverage, including pass-through FDIC insurance and regular, direct deposit insurance for banks issuing stablecoins.

The price of insuring stablecoins depends on various factors, including the financial landscape, asset volatility, and the capital buffer. Estimates of the quarterly price of insurance for major stablecoin issuers have ranged from zero to just below $0.13 per dollar insured for 90 days, with more recent estimates falling below $0.02 per dollar. The cost of insurance is influenced by reduced asset volatility and increased capital buffers, which reduce the sensitivity of insurance cost estimates to shifts in asset volatility.

Becoming an Independent Life Insurance Broker in the UK

You may want to see also

Frequently asked questions

Coinbase carries crime insurance that protects a portion of digital assets held across its storage systems against losses from theft, including cybersecurity breaches. However, this policy does not cover losses resulting from unauthorized access to your account due to a breach or loss of your credentials. It is your responsibility to use a strong password and maintain control of all login credentials.

Coinbase is insured against theft and hacking in an amount that exceeds the average value of bitcoin held in online storage at any given time. The insurance covers losses due to breaches in physical or cyber security, accidental loss, and employee theft.

For U.S. customers, Coinbase combines your balance with the balances of other customers and holds those funds in custodial accounts at U.S. financial institutions. These custodial accounts are FDIC-insured banks or NCUSIF-insured credit unions, which provide pass-through insurance coverage of up to $250,000 per depositor.