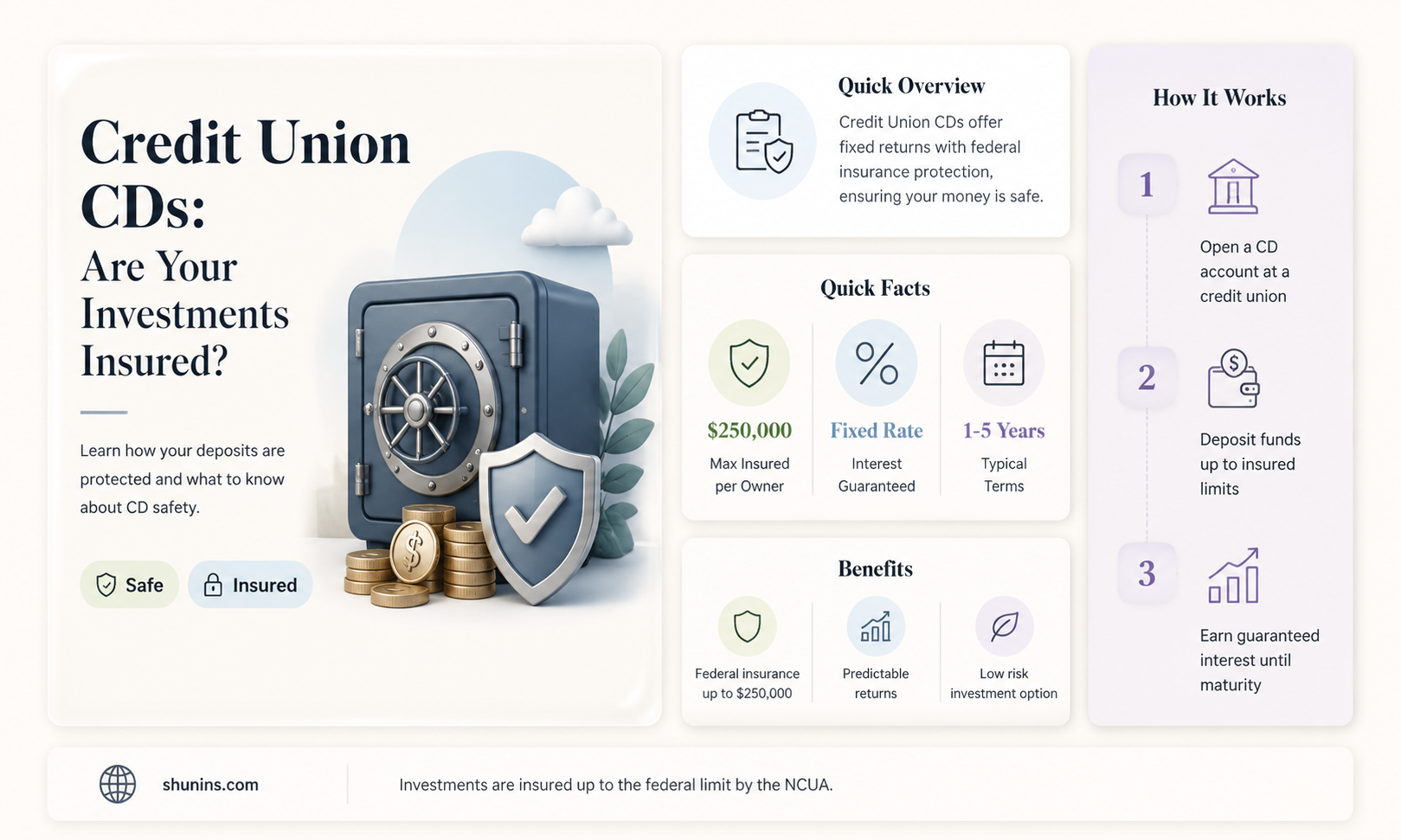

Certificates of deposit (CDs) are insured by the Federal Deposit Insurance Corporation (FDIC) at banks and the National Credit Union Administration (NCUA) at credit unions. The NCUA operates and manages the National Credit Union Share Insurance Fund, which insures deposits of over 143 million account holders in federal credit unions and most state-chartered credit unions. The FDIC and NCUA insurance covers up to $250,000 per depositor per insured bank or credit union per ownership category.

| Characteristics | Values |

|---|---|

| Are credit union CDs insured? | Yes, credit union CDs are insured. |

| Insurer | Federal insurance is provided by the National Credit Union Administration (NCUA) and the National Credit Union Share Insurance Fund (NCUSIF). |

| Insurance limit | $250,000 per depositor, per insured bank or credit union, per ownership category. |

| Insured deposits | All deposits at federally insured credit unions are protected. |

| Insured entities | Over 143 million account holders in all federal credit unions and most state-chartered credit unions are insured. |

| Display of insurance | Federally insured credit unions must display the official NCUA insurance sign at each teller station, on their website, and where they accept share deposits or open accounts. |

| Non-insured items | The NCUA does not insure money invested in stocks, bonds, mutual funds, life insurance policies, annuities, municipal securities, safe deposit boxes, or digital assets such as cryptocurrencies. |

| Insurance verification | To verify insurance, individuals can use the FDIC's BankFind tool for banks and the Research a Credit Union tool for credit unions. |

Explore related products

What You'll Learn

![]()

Federally insured credit unions

The NCUA operates and manages the NCUSIF, which insures the deposits of more than 143 million account holders in all federal credit unions and most state-chartered credit unions. Federally insured credit unions offer a safe place for members to save money, with deposits insured up to at least $250,000 per individual depositor and per ownership category. Credit union members have never lost any insured savings at a federally insured credit union.

The NCUA does not insure money invested in stocks, bonds, mutual funds, life insurance policies, annuities, or municipal securities, even if these investment or insurance products are sold at a federally insured credit union. Additionally, the NCUA does not insure safe deposit boxes or their contents, nor does it insure digital assets such as cryptocurrencies.

Birla Sun Life Insurance: Changing Your Nominee Simplified

You may want to see also

Explore related products

![]()

Share Insurance Coverage

The NCUSIF insures individual accounts at federally insured credit unions up to $250,000, and a member's interest in all joint accounts combined is insured up to $250,000. The fund also separately protects IRA and KEOGH retirement accounts up to $250,000 and provides additional coverage for members' trust accounts. The NCUSIF has the backing of the full faith and credit of the United States government, and no one has ever lost any insured deposits at a federally insured credit union.

Federally insured credit unions are required to display the official NCUA insurance sign at each teller station, on their website, and where they accept share deposits or open accounts. Members can use the NCUA's Share Insurance Estimator to calculate the amount of coverage their insured funds have at a federally insured credit union. It's important to note that the NCUA does not insure money invested in stocks, bonds, mutual funds, life insurance policies, annuities, cryptocurrencies, or municipal securities, even if these products are sold at a federally insured credit union.

There are some state-chartered credit unions that are insured by private insurers, providing non-federal share insurance coverage that is not backed by the full faith and credit of the United States. Members should confirm their credit union is federally insured by using the NCUA's Credit Union Locator tool.

Who Can Be a Life Insurance Beneficiary as an Adult?

You may want to see also

Explore related products

![]()

CD account insurance limits

Certificates of deposit (CDs) are insured by the Federal Deposit Insurance Corporation (FDIC). The standard deposit insurance amount is $250,000 per depositor, per FDIC-insured bank, per ownership category. This limit is permanent and has been in place since 2010.

The FDIC insurance covers the principal amount of the CD and any accrued interest. It does not cover market losses or the premium paid when purchasing a CD on the secondary market. In the unlikely event of a bank failure, the FDIC acts quickly to ensure that all depositors get prompt access to their insured deposits. The FDIC will first search for another bank willing to assume the insured accounts. When it is not possible to sell or transfer the deposits, the FDIC reimburses account holders according to insurance limits.

The ownership categories that apply to the $250,000 limit include single accounts, certain retirement accounts, employee benefit plan accounts, joint accounts, revocable trust accounts, irrevocable trust accounts, and business and government accounts. The maximum insurance coverage for a trust owner with five or more beneficiaries is $1,250,000 per owner for all trust accounts held at the same bank.

Federally insured credit unions are insured by the National Credit Union Administration (NCUA). All deposits at federally insured credit unions are protected by the National Credit Union Share Insurance Fund, with deposits insured up to at least $250,000 per individual depositor. The NCUA does not insure money invested in stocks, bonds, mutual funds, life insurance policies, annuities, municipal securities, or safe deposit boxes and their contents.

Life Insurance: Adding Third-Party Notifications Simplified

You may want to see also

![]()

CD account insurance exceptions

CD accounts are generally insured by the Federal Deposit Insurance Corporation (FDIC) for bank-issued CDs or the National Credit Union Administration (NCUA) for CDs opened at credit unions. Both agencies cover up to $250,000 per depositor, per institution, and per account category. However, there are some exceptions to this insurance coverage.

Firstly, not all banks or credit unions are federally insured. State-chartered credit unions, for example, may not offer deposit insurance because they are regulated by the state and not the NCUA. Therefore, it is crucial to verify that the financial institution offering the CD account is federally insured before opening an account.

Secondly, some types of CDs do not carry deposit insurance even when held at an FDIC or NCUA-insured bank. For instance, investing in CDs issued by foreign banks residing in the US (known as Yankee CD accounts) may not be covered by FDIC insurance. Additionally, purchasing CD accounts through a non-bank institution, such as a brokerage firm, may also lack FDIC insurance.

Thirdly, exceeding the insurance limits can result in a loss of reimbursement. The FDIC and NCUA insurance covers up to $250,000 in each account category at a single bank or credit union. Depositing more than this amount at one institution increases the risk of losing any excess funds in the event of a bank failure.

Furthermore, the NCUA does not insure certain investment and insurance products, even if they are sold at a federally insured credit union. These include money invested in stocks, bonds, mutual funds, life insurance policies, annuities, or municipal securities. Additionally, safe deposit boxes and their contents, as well as digital assets like cryptocurrencies, are not insured by the NCUA.

Lastly, while CDs are generally considered low-risk, there is still a possibility of losing some money. It is important to understand the terms and conditions of the CD account and evaluate the issuing bank's stability to make an informed decision about uninsured CD accounts.

Flex Term Rider: Enhancing Your Life Insurance Coverage

You may want to see also

![]()

CD account insurance verification

When it comes to CD account insurance verification, it is important to understand the different types of insurance available and the steps that can be taken to ensure your funds are protected. Certificates of Deposit (CDs) are generally considered a safe and low-risk investment option. Most CDs are insured by the Federal Deposit Insurance Corporation (FDIC) in the US, which protects your funds in the event that the bank fails. This insurance is automatic for any deposit account opened at an FDIC-insured bank, and there is no need to purchase additional coverage. The FDIC insurance limit is $250,000 per depositor, per bank, per ownership category, which includes the principal amount and any accrued interest. You can verify if a bank is FDIC-insured by using their BankFind tool, contacting their Call Center, or looking for the FDIC sign at the bank.

It is worth noting that not all CDs are FDIC-insured. Some CDs may be offered by companies that are not federally insured, and in those cases, your funds could be at risk if the company goes bankrupt. Additionally, some CDs may be insured by private insurers, particularly in the case of state-chartered credit unions. To verify if your CD is insured by a private insurer, you may need to contact the credit union directly or refer to their website for information.

If you have a CD with a credit union, it may be insured by the National Credit Union Administration (NCUA). The NCUA operates the National Credit Union Share Insurance Fund, which insures deposits in federal credit unions and most state-chartered credit unions. Federally insured credit unions are required to display the official NCUA insurance sign at each teller station and on their website. The NCUA also provides a Credit Union Locator tool that allows members to confirm their credit union is federally insured. The insurance coverage limits for NCUA-insured credit unions are similar to those of the FDIC, with deposits insured up to at least $250,000 per individual depositor.

It is important to understand the specific insurance coverage and limitations of your CD account. If your CD is not FDIC-insured or NCUA-insured, it may be worth considering alternative options or evaluating the stability of the issuing institution. Additionally, be cautious of high-interest rate offers, as they may be marketing strategies to lure customers into uninsured investments. Always read the terms and conditions carefully and consider seeking financial advice if you are unsure about the insurance coverage of your CD account.

Understanding Insurance Coverage When Listed as a Driver

You may want to see also

Frequently asked questions

Yes, credit union CDs are insured by the National Credit Union Administration (NCUA) for up to $250,000 per depositor.

The NCUA insurance covers share deposits received at a federally insured credit union, including deposits in a share draft account, share savings account, and share certificates or CDs.

All federally insured credit unions are required to display the official NCUA insurance sign at each teller station, on their website, and where they accept share deposits or open accounts. You can also use the NCUA's Credit Union Locator tool to confirm if a credit union is federally insured.

In the unlikely event that your credit union fails, the NCUA will step in to protect your insured deposits. Your account will either be transferred to another federally insured institution, or the NCUA will reimburse you up to the insured amount.