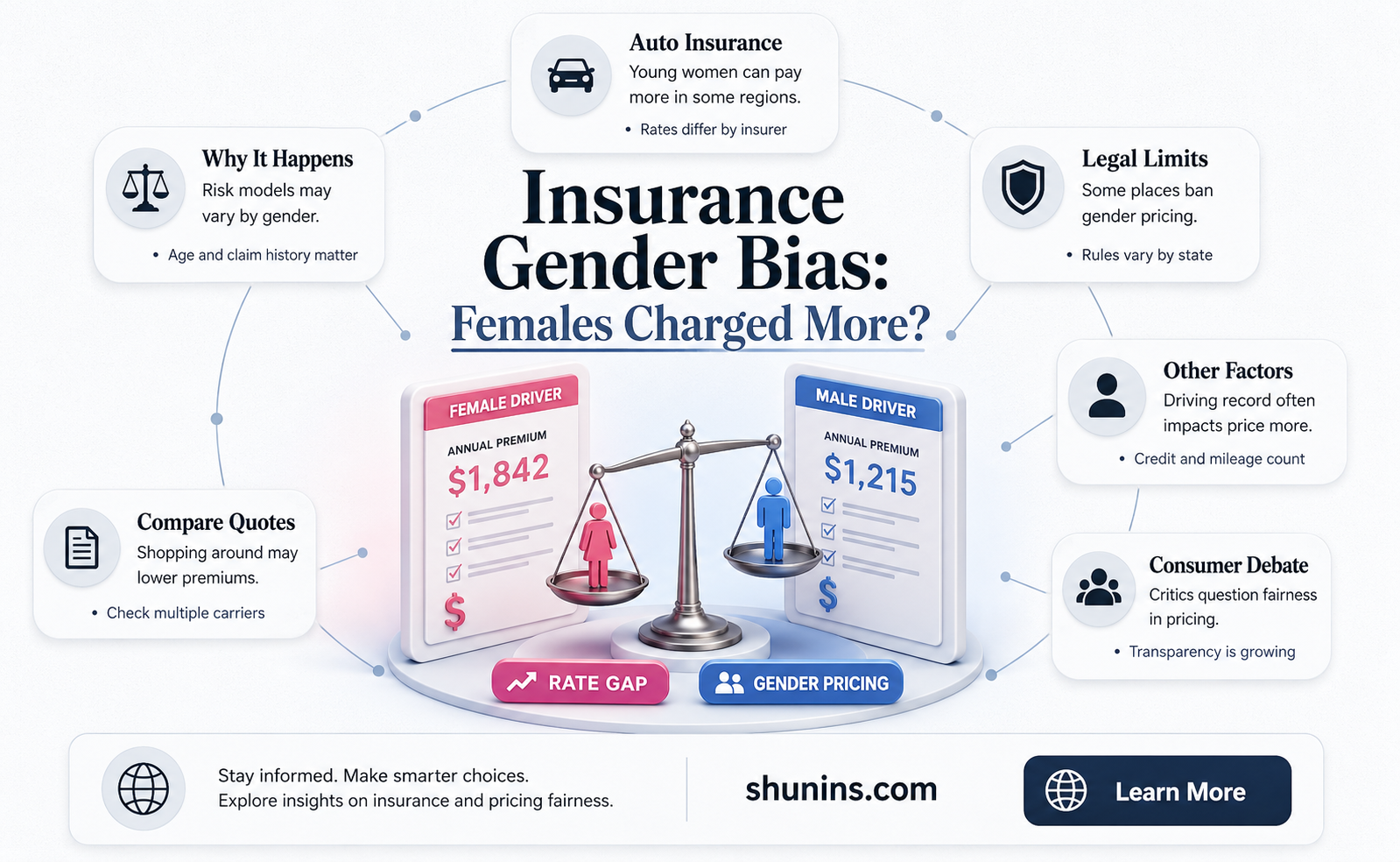

The question of whether women are charged more per insurance policy than men has been a topic of debate for decades. While the difference in cost between men and women is often small, it is still a prevalent issue. In most states, gender will impact insurance rates, with men paying about 1% more than women for car insurance coverage. However, in certain states, such as Florida, New York, Oklahoma, and Oregon, women pay more than men, with a difference of 0.04-2%. The cost of insurance is based on risk factors, and insurers have found that young men are more likely to be involved in accidents and file claims, leading to higher rates for this demographic. On the other hand, women tend to have fewer accidents and driving under the influence (DUI) incidents, resulting in lower insurance rates.

| Characteristics | Values |

|---|---|

| Gender impact on insurance rates | In most states, gender impacts insurance rates, though only slightly. Men pay about 1% more than women for car insurance coverage. |

| Gender-neutral options | As of mid-2022, more than 20 states have gender-neutral options on driver's license forms. |

| States where women pay more | Florida, New York, Oklahoma and Oregon |

| States with the highest difference between what men and women pay | Idaho, Missouri, Texas, and Wyoming, which all have an increase of 4-5% for men. |

| States that don't consider gender | California, Hawaii, Massachusetts, Michigan, Montana, North Carolina, and Pennsylvania |

| Average annual cost for car insurance for women | $1,480 |

| Average annual cost for car insurance for men | $1,470 |

| Average annual cost for car insurance for women under 20 | $1,296 |

| Average annual cost for car insurance for men under 20 | $1,478 |

| Difference in cost for women and men under 20 | 14% |

| Difference in cost for women and men in most age brackets | $10 |

Explore related products

$12.82 $16.95

What You'll Learn

![]()

Auto insurance: Men vs. women

Auto insurance rates vary for men and women, with several factors influencing the cost of coverage. While the difference in rates is generally slight, it is worth understanding how gender influences insurance pricing.

Firstly, it is important to note that gender is not the only factor that determines auto insurance rates. Insurers consider various risk factors when setting prices, including an individual's driving experience, marital status, residence, the car's make and model, and credit score. These factors can have a more significant impact on insurance costs than gender alone.

Historically, auto insurance rates have been higher for men than for women. This is primarily due to statistical differences in driving behaviour and accident risk. Men are more likely to engage in risky driving behaviours, such as speeding and driving under the influence (DUI), and are overrepresented in car crash fatalities. As a result, insurers have traditionally considered men to be a higher-risk group, leading to higher insurance premiums.

However, the situation is more complex than a simple gender divide. The difference in rates varies across different states and age groups. For example, in states like California, eliminating gender as a rating factor could benefit young male drivers with less driving experience, while potentially increasing costs for lower-risk young female drivers. Additionally, in states like Idaho, Missouri, Texas, and Wyoming, men pay slightly more than women on average, while the opposite is true in Florida, New York, Oklahoma, and Oregon.

The gap in insurance rates between men and women also tends to close as motorists reach a certain age. Younger male drivers, particularly teens and those under 20, often pay significantly more for insurance than their female counterparts. This is because insurance companies consider young drivers to be more likely to take risks, drive recklessly, and file claims, regardless of gender. As drivers age, their auto insurance rates typically decrease.

It is worth noting that not all states allow gender to be used as a pricing factor for auto insurance. Some states have outlawed insurance companies from considering gender when setting rates, along with other personal factors such as age, credit history, and occupation. In these states, insurers must rely on other factors to determine insurance costs.

In conclusion, while gender can influence auto insurance rates, the impact varies depending on location and age group. Other risk factors also play a significant role in determining insurance costs. Individuals concerned about the impact of gender on their insurance rates can shop around for insurance companies that do not consider gender when setting prices or offer more favourable rates for their gender.

Life Insurance Payouts After Suicide: What You Need to Know

You may want to see also

Explore related products

![]()

Gender-neutral insurance

Gender has traditionally played a role in determining insurance costs, with men paying more for car insurance overall due to higher crash rates and other harmful driving behaviours. However, the impact of gender on insurance rates has been disputed, with some studies showing that women are charged more than men in certain states. In recent years, there has been a growing movement towards gender-neutral insurance, with an increasing number of states banning gender-based pricing and insurance companies offering non-binary gender options on insurance applications.

The concept of gender-neutral insurance aims to address the disparities in insurance rates between men and women and to provide more inclusive options for transgender and non-binary individuals. While gender-based pricing has been a common practice in the insurance industry, it has been criticised for perpetuating gender stereotypes and failing to consider other risk factors. As a result, there has been a push for insurance companies to move towards gender-neutral policies and pricing structures.

In the context of car insurance, gender-neutral insurance involves setting rates and premiums based on factors other than gender, such as driving history, age, and type of car. This means that insurance companies would no longer use gender as a rating factor when determining the cost of coverage. Instead, they would rely on other data and metrics to assess risk and set prices.

As of 2023, it was reported that 42 states in the US allow insurance rates to change if an individual transitions genders. This means that in these states, insurance companies can legally take gender into account when determining insurance prices. However, this practice has been outlawed in a growing number of states, including California, Hawaii, Massachusetts, Michigan, Montana, North Carolina, and Pennsylvania. In these states, insurance companies are prohibited from using gender as a factor in setting rates, and they must offer non-binary gender options on insurance applications.

The movement towards gender-neutral insurance is not only about ensuring fair and equal treatment for all individuals but also about recognising the diverse and fluid nature of gender identity. By offering non-binary gender options and removing gender as a rating factor, insurance companies can better serve the LGBTQ+ community and create a more inclusive environment for all.

Borrowing Against Your Guardian Life Insurance: Is it Possible?

You may want to see also

Explore related products

![]()

Insurance rates by state

Insurance rates vary across the United States, and several factors can influence these rates. While gender is one of the factors that impact insurance rates, other factors, such as age, location, credit score, driving history, and the type of vehicle insured, also play a significant role in determining insurance premiums.

In terms of gender, there are discrepancies in insurance rates between men and women across different states. In 37 states, women pay more annually than men for auto insurance, with a national average difference of $32. Florida, Oregon, and Delaware have the most significant gaps in insurance costs between genders, with Florida having a $199 difference. On the other hand, men pay more than women in seven states, with Wyoming, Vermont, and Ohio exhibiting the most considerable disparities.

However, it is important to note that some states have taken steps to address this gender disparity in insurance rates. California, Hawaii, Massachusetts, Michigan, North Carolina, and Pennsylvania do not use gender as a determining factor in calculating insurance premiums. These states believe that insurance costs should primarily reflect an individual's driving history and claims record rather than personal characteristics.

Location is another critical factor influencing insurance rates. Urban areas with higher crime rates and traffic violations tend to have higher insurance premiums. Additionally, states with poor road conditions and a high number of uninsured motorists, such as Colorado, may contribute to elevated insurance costs.

Credit score is also a significant component in determining insurance rates. However, this varies across states. California, Hawaii, Massachusetts, Michigan, Oregon, and Utah do not allow insurance companies to consider credit scores when setting rates. As a result, insurers in these states may place more weight on other factors, such as driving history and vehicle type.

Age is another factor that impacts insurance rates, although its influence varies by state. Teen drivers tend to have higher insurance rates due to their increased risk of accidents and filing claims. Male teens, in particular, often face higher insurance costs than their female counterparts, as they are statistically more likely to be involved in car accidents.

In conclusion, insurance rates by state are influenced by a multitude of factors, including gender, location, credit score, age, and driving history. While gender plays a role in insurance rates, it is just one aspect of a broader set of considerations that insurance companies use to assess risk and set premiums.

Insurance or Life Insurance: What's in a Name?

You may want to see also

Explore related products

![]()

Risk factors

Insurance companies set premiums based on risk and on factors they are allowed by law to take into consideration. Insurers can’t set premiums based on an applicant’s race or religion, for example. But insurance companies traditionally have tied gender to an applicant's risk, so it's often been a factor in setting premiums.

When it comes to auto insurance, men are considered to be riskier drivers than women. Figures from the Department of Transportation’s Fatality Analysis Reporting System (FARS) show that men accounted for 72% of all car crash deaths in 2020. Men also typically drive more miles than women and are more likely to practice risky driving behaviours, including speeding, driving while under the influence (DUI), and not wearing seatbelts. As a result, men tend to pay more for auto insurance than women, especially at younger ages.

However, the situation is reversed for health insurance, where women are considered to be riskier and thus more expensive to insure. Women of reproductive age, for example, are at risk of pregnancy and childbirth, which can be very expensive.

It's important to note that not all states or countries allow insurers to use gender as a pricing factor. In the United States, California, Hawaii, Massachusetts, Michigan, Montana, North Carolina, and Pennsylvania prohibit insurers from considering gender when calculating premiums. Similarly, in the context of life insurance, charging women of reproductive age more would incentivise them to drop their insurance, which could result in only the riskiest group of men remaining insured, leading to higher premiums for all.

In conclusion, while gender has traditionally been used as a factor in setting insurance premiums, it is only one of many factors that insurers consider. Other factors may include age, marital status, residence, credit score, and the type of car driven. Additionally, the impact of gender on insurance rates varies by location and insurer, and there are an increasing number of states and companies that do not consider gender at all when setting rates.

Whole Life Insurance: A Comprehensive Employee Benefit?

You may want to see also

Explore related products

![]()

Health insurance

Women in the US consistently pay more for healthcare than men, despite legislation designed to prevent this. In 2021, women paid about 20% more for out-of-pocket medical expenses than men, with similar findings in other years. This equates to around $15 billion more spent on healthcare per year than men.

There are several reasons why women may utilise healthcare more than men. Women are more likely to visit healthcare professionals and to require more services when they do. This may be due to recommendations for annual check-ups at earlier ages, the regular frequency of gynaecological exams, and the effects of menopausal transitions. The services they receive also more often surpass the deductibles, meaning higher costs.

In addition, women have lower actuarial values, meaning that insurance covers less of their health claims. This could be because insurers do not cover expensive follow-up services, or because women have worse insurance plans with higher deductibles or copays.

While the Affordable Care Act prohibits gender rating, meaning insurers must charge men and women the same premium costs, this does not reflect the actual cost as premiums are only part of the financial story. The higher costs that women face for healthcare contribute to the gender pay gap.

Life Insurance: Extreme Sports and Your Coverage

You may want to see also

Frequently asked questions

It depends on the type of insurance. Women are charged more than men for health insurance because they are statistically more expensive to insure. However, men are charged more for auto insurance because they are more likely to get into accidents and file claims.

There is no fixed amount by which females are charged more for health insurance. However, historically, health insurance has cost more for women than for men.

Males below 20 years of age pay 14% more per year for auto insurance than females in the same age bracket. The difference is more pronounced for younger drivers, with the gap closing once motorists reach a certain age. On average, men pay about 1% more than women for auto insurance coverage.

The states with the highest difference between what men and women pay for auto insurance are Idaho, Missouri, Texas, and Wyoming, with an increase of 4-5% for men.