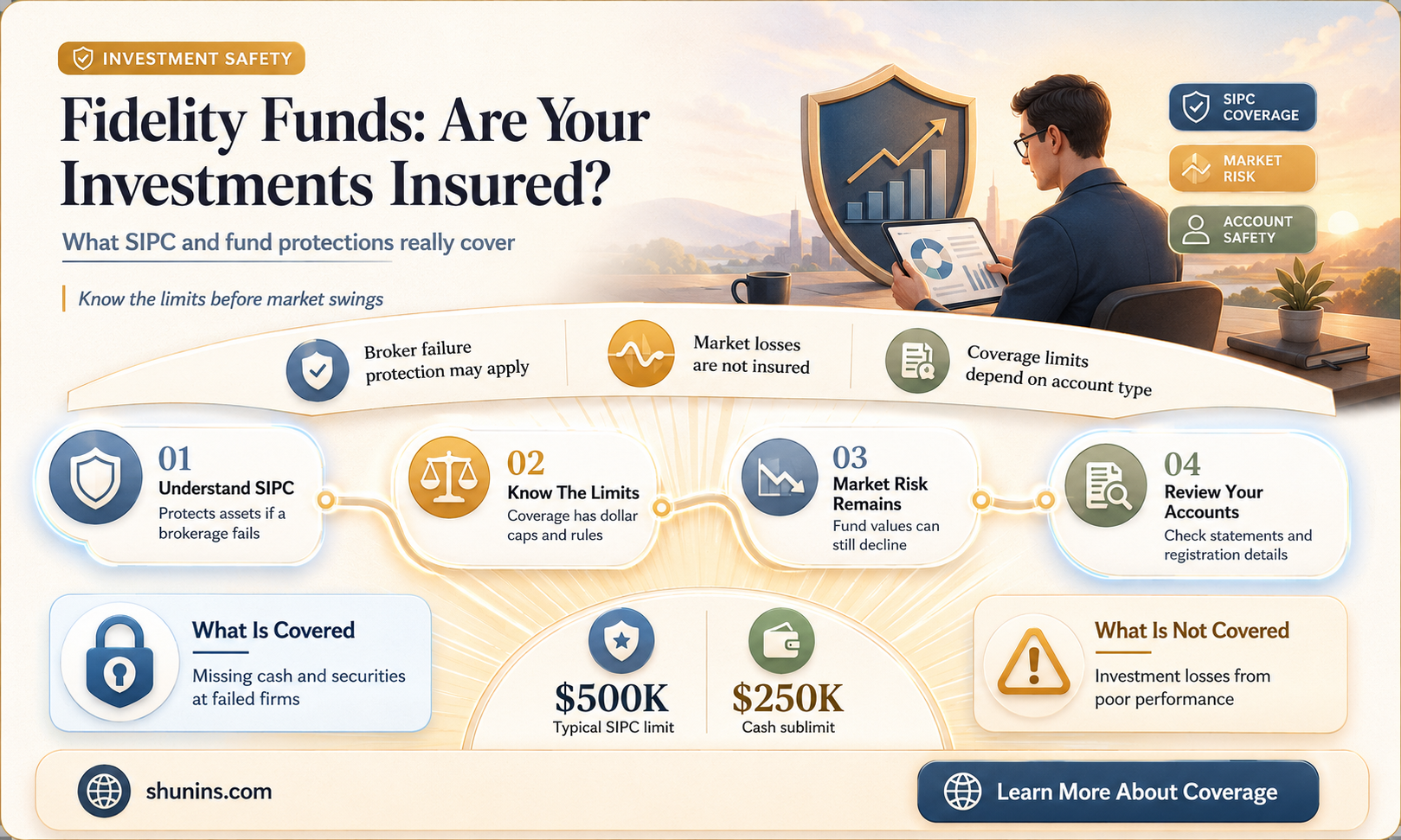

Fidelity offers a range of financial services, including the Fidelity Cash Management Account, a brokerage account that allows customers to spend, save, and invest. This account is not a bank account and is not FDIC-insured, but uninvested cash balances are eligible for FDIC insurance. Deposits swept into program banks are eligible for FDIC Insurance, subject to coverage limits. Balances that exceed these limits may be swept to a Money Market Mutual Fund, which is not FDIC-insured but is eligible for SIPC coverage. The Securities Investor Protection Corporation (SIPC) is a nonprofit organization that protects stocks, bonds, and other securities in the event of brokerage firm bankruptcy or missing assets. While Fidelity is committed to protecting its customers' assets, it is important to note that investing involves risk, and customers should be aware of the potential for financial loss.

| Characteristics | Values |

|---|---|

| Type of fund | Money market mutual fund |

| Insured by Federal Deposit Insurance Corporation (FDIC) | No |

| Insured by Securities Investor Protection Corporation (SIPC) | Yes |

| Insured by any other government agency | No |

| Fidelity reimburses ATM fees charged by other institutions | Yes |

| Fidelity charges foreign transaction fees | No |

| Fidelity provides legal or tax advice | No |

Explore related products

What You'll Learn

![]()

Fidelity Cash Management Account

The Fidelity Cash Management Account (CMA) is a brokerage account designed for spending, cash management, and saving. It is intended to complement, not replace, an existing brokerage account. It offers a competitive rate of return, no account fees, and no minimum account balance.

Fidelity's CMA is not a bank account and is not FDIC-insured. However, uninvested cash balances are eligible for FDIC insurance and are swept into an FDIC-insured interest-bearing account at one or more program banks. Each program bank will receive a maximum of $245,000 to ensure that any accrued interest is also eligible for FDIC insurance (with a $250,000 coverage limit). Any deposits over $245,000 will be distributed across multiple available program banks.

Deposits swept into the program banks are eligible for FDIC Insurance, subject to FDIC insurance coverage limits. Balances that are swept to the Money Market Overflow are not eligible for FDIC insurance but are eligible for SIPC coverage under SIPC rules. The Securities Investor Protection Corporation (SIPC) is a nonprofit organization that protects stocks, bonds, and other securities in the event a brokerage firm goes bankrupt and assets are missing. The SIPC will cover up to $500,000 in securities, including a $250,000 limit for cash held in a brokerage account.

The CMA offers features such as a free debit card, check writing, Bill Pay, mobile check deposit, and payment apps integration. It also offers overdraft protection and automated transfers.

Life Insurance: Global Coverage and Death Benefits

You may want to see also

Explore related products

![]()

FDIC-insured interest-bearing accounts

The Federal Deposit Insurance Corporation (FDIC) provides insurance for depositors at insured banks. This insurance covers the depositor's principal and any accrued interest up to a limit of $250,000 per depositor, per insured bank, and per ownership category. This insurance is automatic and free for depositors and covers a range of deposit products, including checking and savings accounts, money market deposit accounts, and certificates of deposit. It's important to note that FDIC insurance does not cover investments, including stocks, bonds, mutual funds, annuities, and life insurance policies.

Fidelity offers a Cash Management Account, which is a brokerage account designed for spending and cash management. While brokerage accounts are not FDIC-insured, uninvested cash balances in the Fidelity Cash Management Account are eligible for FDIC insurance. This is achieved through an FDIC-insured Deposit Sweep program, which automatically sweeps uninvested cash into FDIC-insured interest-bearing accounts at program banks, ensuring that the cash balances are protected.

The number of program banks available can vary, and each bank will receive a maximum of $245,000 to ensure that any accrued interest is also eligible for FDIC insurance. Any deposits exceeding this amount will be distributed across multiple program banks. For example, if a customer deposits $500,000, $245,000 will be swept into each of the first two available program banks, and the remaining $10,000 will be swept into a third. This strategy ensures that customers' cash balances are protected up to the FDIC insurance limits.

It's important to note that balances swept into the Money Market Overflow fund, a money market mutual fund, are not eligible for FDIC insurance. However, they are eligible for coverage by the Securities Investor Protection Corporation (SIPC), which protects stocks, bonds, and other securities in the event of brokerage firm bankruptcy. The SIPC provides coverage of up to $500,000 in securities, including a $250,000 limit for cash held in a brokerage account.

In summary, the FDIC provides insurance for depositors at insured banks, covering principal and accrued interest up to specified limits. Fidelity's Cash Management Account utilizes an FDIC-insured Deposit Sweep program to ensure that uninvested cash balances are protected by sweeping them into FDIC-insured interest-bearing accounts at program banks. Any excess funds swept into the Money Market Overflow fund are covered by SIPC instead of FDIC.

Weight's Impact: Life Insurance Premiums and Health

You may want to see also

Explore related products

![]()

Money Market Mutual Fund

Fidelity offers government, prime, and municipal (or tax-exempt) money market funds, and is an industry leader, managing over $900 billion in total money market assets. Government money market funds generally invest at least 99.5% of the fund's total assets in cash, US government securities, and repurchase agreements. Prime money market funds have historically offered higher yields than government funds.

Fidelity's money market funds offer benefits such as stability, safety, liquidity, competitive returns, and potential tax advantages. However, it is important to consider the investment objectives, risks, charges, and expenses of any mutual fund before investing. Performance data shown represents past performance and is not a guarantee of future results. Investment return and principal value will fluctuate, and you may gain or lose money when shares are sold.

Fidelity also offers a Cash Management Account, which is a high-yield alternative to traditional banking. If elected, the cash balances in this account are swept into an FDIC-insured interest-bearing account at one or more program banks and, under certain circumstances, a Money Market Overflow fund. Deposits held at the program banks are eligible for FDIC insurance, while balances in the Money Market Overflow fund are not FDIC-insured but are eligible for SIPC coverage.

Insurable Interest: Life Insurance's Core Principle Explained

You may want to see also

![]()

Securities Investor Protection Corporation (SIPC)

The Securities Investor Protection Corporation (SIPC) is a federally mandated, non-profit, member-funded, United States government corporation. It was created under the Securities Investor Protection Act (SIPA) of 1970, which mandates membership of most US-registered broker-dealers. Although created by federal legislation and overseen by the Securities and Exchange Commission, the SIPC is neither a government agency nor a regulator of broker-dealers. The SIPC has a Board of Directors that determines the policies that govern its operations. The board consists of seven members, all of whom serve for terms of three years.

The purpose of the SIPC is to protect investors by recovering and returning missing customer cash and assets during the liquidation of a failed investment firm. It has been protecting investors for over 50 years and has recovered billions of dollars for investors. The SIPC protects stocks, bonds, and other securities in case a brokerage firm goes bankrupt and assets are missing. It covers up to $500,000 in securities, including a $250,000 limit for cash held in a brokerage account.

All Fidelity brokerage accounts are covered by SIPC, including money market funds held in a brokerage account since they are considered securities. However, it is important to note that SIPC protection does not apply when investors place their cash or securities with a non-SIPC member firm. Therefore, investors should always ensure that the brokerage firm and its clearing firm are members of SIPC.

The SIPC steps in when a SIPC-member brokerage firm fails financially and assets are missing from customer accounts. It does not protect against losses caused by a decline in the market value of securities and does not provide protection for investment contracts not registered with the SEC.

Life Insurance: What Makes a Policy Appreciable?

You may want to see also

![]()

Fidelity Government Money Market Fund

Money market funds are mutual funds that invest in debt securities with short maturities and minimal credit risk. These funds are issued by government entities or companies that borrow money and repay principal and interest to investors within a short period. Money market funds are among the lowest-volatility types of investments.

The fund is not covered by FDIC insurance and is subject to market risk. An investment in the fund is not a bank account and is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. However, the fund is eligible for SIPC coverage, which will cover up to $500,000 in securities, including a $250,000 limit for cash held in a brokerage account.

Money market funds like the Fidelity Government Money Market Fund accrue interest daily, and deposit this accrued interest on the first business day of the following month. The fund seeks to preserve the value of your investment at $1.00 per share, but it cannot guarantee it will do so.

Borrowing Against Your Globe Life Insurance: What You Need to Know

You may want to see also

Frequently asked questions

The Fidelity Cash Management Account is not a bank account. It is a brokerage account that allows you to spend, save, and invest. The cash balance in the account is swept into an FDIC-insured interest-bearing account at one or more program banks. Deposits swept into the program bank(s) are eligible for FDIC Insurance, subject to FDIC insurance coverage limits.

The FDIC-Insured Deposit Sweep Program sweeps your uninvested cash into an FDIC-insured interest-bearing account at one or more program banks.

The Money Market Overflow, or Money Market Mutual Fund Overflow, is a component of the FDIC-Insured Deposit Sweep Program. It comes into play when deposit amounts exceed FDIC insurance limits. Excess funds are swept to the Fidelity Government Money Market Fund.

No, money market funds are not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency.

Yes, all Fidelity brokerage accounts, including money market funds held in a brokerage account, are covered by the Securities Investor Protection Corporation (SIPC). The SIPC is a nonprofit organization that protects stocks, bonds, and other securities in case a brokerage firm goes bankrupt and assets are missing. The SIPC will cover up to $500,000 in securities, including a $250,000 limit for cash held in a brokerage account.