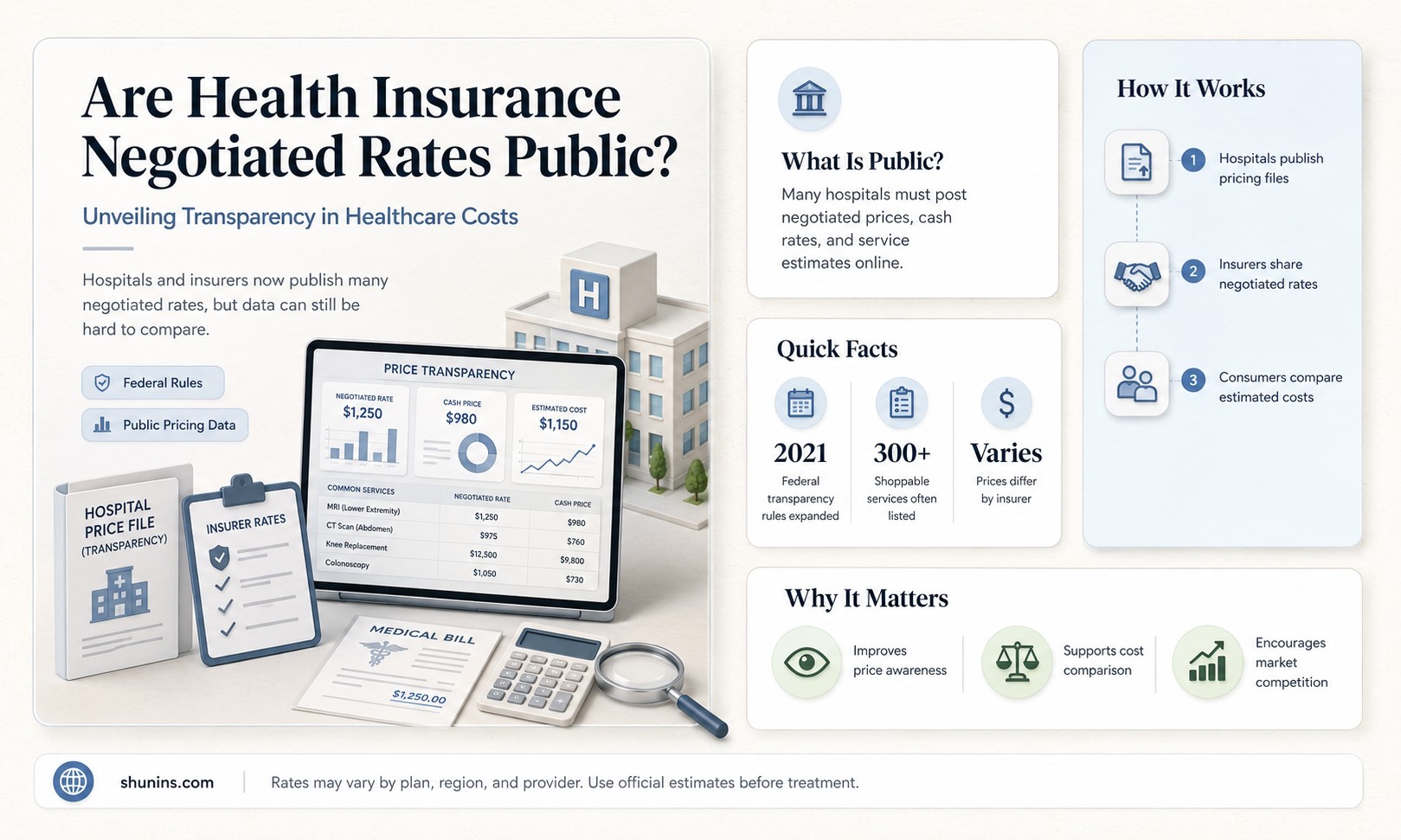

The question of whether health insurance negotiated rates are public is a critical issue in the healthcare industry, as it directly impacts transparency, affordability, and consumer decision-making. Negotiated rates, which are the discounted prices insurers agree upon with healthcare providers, are often kept confidential through contractual agreements, leaving patients and policymakers in the dark about the true cost of medical services. While some argue that disclosing these rates could lead to more informed choices and reduce overall healthcare costs, others contend that publicizing them might hinder insurers' ability to negotiate effectively. This debate has sparked legislative efforts in some regions to mandate rate transparency, yet challenges remain in balancing the interests of insurers, providers, and consumers. Understanding the implications of making negotiated rates public is essential for addressing the broader issues of healthcare accessibility and cost control.

| Characteristics | Values |

|---|---|

| Public Availability | Negotiated rates between health insurers and providers are generally not publicly disclosed in the U.S. due to confidentiality agreements. |

| Transparency Laws | Some states (e.g., California, Colorado) have passed laws requiring limited transparency, but federal mandates are lacking. |

| Exceptions | Medicare and Medicaid rates are publicly available, but private insurer rates remain private. |

| Reason for Secrecy | Insurers and providers argue that disclosing rates could weaken their negotiating positions. |

| Consumer Impact | Lack of transparency makes it difficult for patients to compare costs or understand billing. |

| Recent Developments | The No Surprises Act (2022) addresses surprise billing but does not mandate public disclosure of negotiated rates. |

| Advocacy Efforts | Groups like the Healthcare Financial Management Association (HFMA) push for greater transparency. |

| International Comparison | Countries like Germany and the UK have more transparent healthcare pricing systems. |

| Data Sources | Limited data is available through employer-sponsored plans or third-party platforms like Turquoise Health. |

| Future Outlook | Increasing pressure from policymakers and consumers may lead to gradual disclosure of negotiated rates. |

Explore related products

What You'll Learn

![]()

Transparency Laws and Regulations

Health insurance negotiated rates, often shrouded in secrecy, are increasingly becoming a focal point of transparency laws and regulations. These laws aim to shed light on the complex pricing agreements between insurers and healthcare providers, empowering consumers to make informed decisions. For instance, the federal No Surprises Act, enacted in 2022, prohibits surprise medical billing and requires providers to disclose out-of-network charges, indirectly pushing for greater rate transparency. However, while progress is being made, the landscape remains fragmented, with state-specific laws varying widely in their scope and enforcement.

One of the most significant challenges in achieving transparency is the proprietary nature of negotiated rates. Insurers and providers often argue that disclosing these rates could undermine their bargaining power, leading to higher costs for consumers. However, this argument is increasingly being challenged by policymakers and consumer advocates. States like Colorado and Maine have taken bold steps, mandating the publication of negotiated rates in a standardized format. Colorado’s HB21-1286, for example, requires insurers to provide a publicly accessible database of in-network rates, allowing consumers to compare costs before seeking care. Such initiatives demonstrate that transparency is not only feasible but also beneficial in driving market competition.

Implementing transparency laws requires careful consideration of practical challenges. One major hurdle is ensuring data accuracy and usability. Negotiated rates are often complex, varying by procedure, provider, and patient population. Standardizing this data for public consumption is no small feat. For instance, California’s Senate Bill 852 mandates the disclosure of negotiated rates but has faced criticism for producing datasets that are difficult for the average consumer to navigate. To address this, regulators must collaborate with stakeholders to develop user-friendly tools, such as cost estimators or comparison platforms, that translate raw data into actionable insights.

Despite these challenges, the momentum toward transparency is undeniable. The Centers for Medicare & Medicaid Services (CMS) has introduced federal rules requiring insurers to make negotiated rates publicly available by 2024. This move is expected to set a national standard, reducing the patchwork of state-level regulations. However, enforcement will be critical. Without robust oversight, insurers and providers may find loopholes to circumvent disclosure requirements. Consumer education will also play a vital role, as transparency alone does not guarantee informed decision-making. Practical tips, such as verifying in-network status and using cost estimation tools, can help individuals navigate this new landscape effectively.

In conclusion, transparency laws and regulations are reshaping the health insurance industry, but their success hinges on thoughtful implementation and enforcement. By learning from early adopters like Colorado and addressing practical challenges, policymakers can ensure that negotiated rates become a tool for empowerment rather than confusion. As these laws evolve, consumers must stay informed and proactive, leveraging available resources to make cost-effective healthcare choices. The journey toward full transparency is ongoing, but each step brings us closer to a fairer, more accessible healthcare system.

Tennessee Medicaid: Which Health Insurers Are Involved?

You may want to see also

Explore related products

![]()

Provider-Insurer Contract Confidentiality

Health insurance negotiated rates are often shrouded in secrecy due to provider-insurer contract confidentiality clauses. These clauses, embedded in agreements between healthcare providers and insurance companies, explicitly prohibit the disclosure of negotiated rates to third parties, including patients and the public. This practice raises significant questions about transparency in healthcare pricing and its impact on consumer decision-making.

The Rationale Behind Confidentiality

Proponents of contract confidentiality argue that it fosters a competitive environment. Insurers claim that revealing negotiated rates could weaken their bargaining power, leading to higher costs for everyone. Providers, similarly, fear that publicizing rates might encourage patients to shop around solely based on price, potentially undermining the value of their services. This perspective views confidentiality as a necessary tool to maintain stability in the healthcare market.

The Consumer Perspective

From a consumer standpoint, the lack of transparency surrounding negotiated rates is a major obstacle to informed decision-making. Patients often face unexpected medical bills due to the opacity of pricing structures. Knowing negotiated rates upfront would empower individuals to compare costs across providers, choose the most cost-effective options, and potentially negotiate better terms with their insurers.

Legal and Policy Landscape

The legal landscape regarding provider-insurer contract confidentiality is complex and evolving. Some states have enacted laws requiring greater price transparency, while federal initiatives like the No Surprises Act aim to protect patients from surprise medical bills. However, these efforts often face resistance from industry stakeholders who argue that mandated disclosure could disrupt existing contractual agreements and market dynamics.

Balancing Act: Transparency vs. Market Stability

Striking a balance between transparency and market stability is crucial. While complete disclosure of all negotiated rates might be impractical, targeted transparency measures could be implemented. For instance, providing patients with estimated out-of-pocket costs based on their insurance plan and the provider's negotiated rates could significantly improve affordability and accessibility.

Moving Forward

Ultimately, addressing provider-insurer contract confidentiality requires a multi-faceted approach. Policymakers, industry leaders, and consumer advocates must collaborate to develop solutions that promote transparency without compromising market stability. This could involve exploring alternative pricing models, strengthening price comparison tools, and fostering greater public awareness about healthcare costs.

Primary Insurance: VA Medical as Your Default Option

You may want to see also

Explore related products

![]()

Consumer Access to Rate Information

Health insurance negotiated rates, often shrouded in secrecy, are a critical component of healthcare affordability. While these rates are typically confidential agreements between insurers and providers, there’s a growing push for transparency. Consumer access to this information is limited, yet it holds the potential to empower individuals to make informed decisions about their healthcare spending. Understanding the landscape of negotiated rates requires dissecting the barriers, tools, and implications of making this data public.

One practical step toward transparency is leveraging state-level initiatives and online tools. For instance, states like Colorado and New Hampshire have launched price transparency websites, allowing consumers to compare costs for common procedures across providers. These platforms, though not exhaustive, provide a glimpse into the variability of negotiated rates. Additionally, third-party tools like FAIR Health and Turquoise Health aggregate data to offer estimates, though they often lack real-time accuracy. Consumers can maximize these resources by focusing on specific procedures, such as MRIs or colonoscopies, and cross-referencing data with their insurance provider’s cost estimator.

However, accessing negotiated rates isn’t without challenges. Insurers and providers often cite proprietary concerns to justify keeping this information private. Legal battles, such as the 2021 federal rule requiring hospitals to disclose negotiated rates, have faced pushback and delays. Consumers must navigate this opacity by advocating for themselves—asking providers for out-of-pocket estimates, scrutinizing Explanation of Benefits (EOB) statements, and appealing unexpected charges. For example, if a bill exceeds the estimated cost by more than 10%, patients can request a review under state surprise billing laws.

The implications of public access to negotiated rates extend beyond individual savings. Transparency could drive market competition, forcing providers to justify high costs and insurers to negotiate better deals. A 2020 study by the RAND Corporation found that employer-sponsored insurance plans paid 247% of Medicare rates on average, highlighting the inefficiencies in the current system. By demanding access to this data, consumers can collectively pressure stakeholders to address these disparities. Practical tips include joining advocacy groups like Patients Rights Advocate and using social media to amplify calls for transparency.

In conclusion, while negotiated rates remain largely hidden, consumers are not entirely powerless. By utilizing available tools, understanding legal protections, and advocating for systemic change, individuals can navigate the opaque landscape of healthcare pricing. The push for transparency is not just about saving money—it’s about reshaping a system that prioritizes clarity and fairness. As the debate continues, staying informed and proactive is key to unlocking the potential of public access to negotiated rates.

Medicare and Elders: Are There Other Insurance Options?

You may want to see also

Explore related products

![]()

State vs. Federal Disclosure Rules

Health insurance negotiated rates, often shrouded in secrecy, are increasingly becoming a focal point in the push for healthcare transparency. While federal efforts have set the stage, states are emerging as the primary drivers of disclosure rules, creating a patchwork of regulations that vary widely in scope and impact. This divergence raises critical questions about accessibility, fairness, and the future of healthcare pricing.

Consider the federal landscape: The 2021 Transparency in Coverage Rule mandates that insurers publicly disclose in-network rates and out-of-network allowed amounts. However, this rule stops short of requiring the disclosure of actual negotiated rates, leaving a significant gap in transparency. For instance, while consumers can see a range of prices for a procedure, they cannot access the specific rate their insurer has negotiated with a provider. This limitation underscores the federal approach’s focus on broad accessibility over granular detail, a strategy that prioritizes compliance across diverse markets but may fall short of empowering individual consumers.

In contrast, states like California and Colorado have taken bold steps to bridge this gap. California’s Senate Bill 910, for example, requires hospitals to disclose payer-specific negotiated rates, offering consumers a clearer picture of pricing disparities. Similarly, Colorado’s House Bill 1286 mandates that insurers and providers publish negotiated rates for the top 250 medical services. These state-level initiatives demonstrate a more aggressive approach to transparency, one that directly challenges the opacity of healthcare pricing. However, such measures are not without controversy, as industry stakeholders argue that disclosing negotiated rates could undermine competitive advantages and destabilize markets.

The tension between state and federal rules highlights a broader dilemma: How can transparency be achieved without compromising the stability of the healthcare ecosystem? For consumers, the answer lies in actionable information. Knowing the exact negotiated rate for a knee replacement or a routine MRI can significantly influence provider choice and reduce out-of-pocket costs. Yet, the fragmented nature of state-level disclosures means that access to this information varies dramatically by geography. A resident of California may enjoy greater transparency than someone in Texas, where no such disclosure laws exist.

To navigate this landscape, consumers must stay informed about their state’s specific regulations. Practical steps include checking state health department websites for transparency initiatives, using online tools like Healthcare Bluebook to estimate fair prices, and advocating for stronger disclosure laws through local representatives. Employers can also play a role by pressing insurers for more transparent pricing models in group plans. While federal rules provide a baseline, it is at the state level where the battle for true healthcare pricing transparency is being fought—and won, one jurisdiction at a time.

Who Regulates Florida's Insurance Companies: Understanding the Governing Bodies

You may want to see also

Explore related products

![Public Enemies [Blu-ray]](https://m.media-amazon.com/images/I/81G4BHHCQDL._AC_UY218_.jpg)

![]()

Impact on Healthcare Cost Comparisons

Health insurance negotiated rates, when kept private, create a veil of opacity that significantly hampers consumers' ability to make informed healthcare cost comparisons. Without access to these rates, patients often face unexpected out-of-pocket expenses, as the billed amount and the insurer-negotiated rate can differ drastically. For instance, a routine MRI might be billed at $2,000, but the insurer’s negotiated rate could be $600—a disparity that remains hidden from the patient until the bill arrives. This lack of transparency not only breeds frustration but also limits the ability to shop for cost-effective care, perpetuating a system where prices are dictated by secrecy rather than competition.

Consider the practical implications for a 45-year-old patient needing a colonoscopy. In a transparent system, they could compare negotiated rates across providers, perhaps finding one charging $800 versus another at $1,500 for the same procedure. Armed with this information, they could choose the more affordable option, potentially saving hundreds of dollars. However, in the current opaque system, such comparisons are nearly impossible, leaving patients at the mercy of hidden agreements between insurers and providers. This inefficiency not only inflates individual costs but also contributes to the broader issue of escalating healthcare expenditures nationwide.

Advocates for transparency argue that publicizing negotiated rates would foster competition among providers, driving down costs. For example, if a hospital’s negotiated rate for a knee replacement were publicly known to be 30% higher than nearby facilities, patients might opt for the more affordable option, incentivizing the higher-priced hospital to lower its rates. However, opponents counter that such transparency could lead to price-fixing or reduced flexibility in negotiations. Yet, this concern overlooks the potential for regulatory safeguards to prevent anticompetitive behavior while still empowering consumers with critical cost information.

From a comparative standpoint, industries like auto insurance and travel thrive on price transparency, allowing consumers to make informed choices. Healthcare, however, remains an outlier, with negotiated rates locked away in proprietary contracts. A step-by-step approach to addressing this could include: (1) mandating insurers to disclose negotiated rates in an accessible format, (2) developing user-friendly tools for cost comparisons, and (3) educating consumers on how to leverage this information. Cautions include ensuring data privacy and avoiding overwhelming patients with complex details, perhaps by focusing on high-impact procedures like surgeries or diagnostic tests.

In conclusion, the impact of publicizing health insurance negotiated rates on healthcare cost comparisons cannot be overstated. It shifts power from opaque systems to informed consumers, enabling smarter decisions and potentially reducing costs. While challenges exist, the benefits of transparency—lower expenses, increased competition, and empowered patients—far outweigh the drawbacks. As the healthcare landscape evolves, making negotiated rates public is not just a policy option but a necessity for a fairer, more efficient system.

Who Takes the Reins? Understanding Insurance Company Control and Leadership

You may want to see also

Frequently asked questions

No, health insurance negotiated rates are typically not public information. They are confidential agreements between insurers and healthcare providers.

Patients can often access their specific out-of-pocket costs through their insurance provider’s tools or by contacting customer service, but the full negotiated rates are usually not disclosed.

Negotiated rates are kept private due to contractual agreements between insurers and providers, as well as concerns about competitive disadvantages and market dynamics.