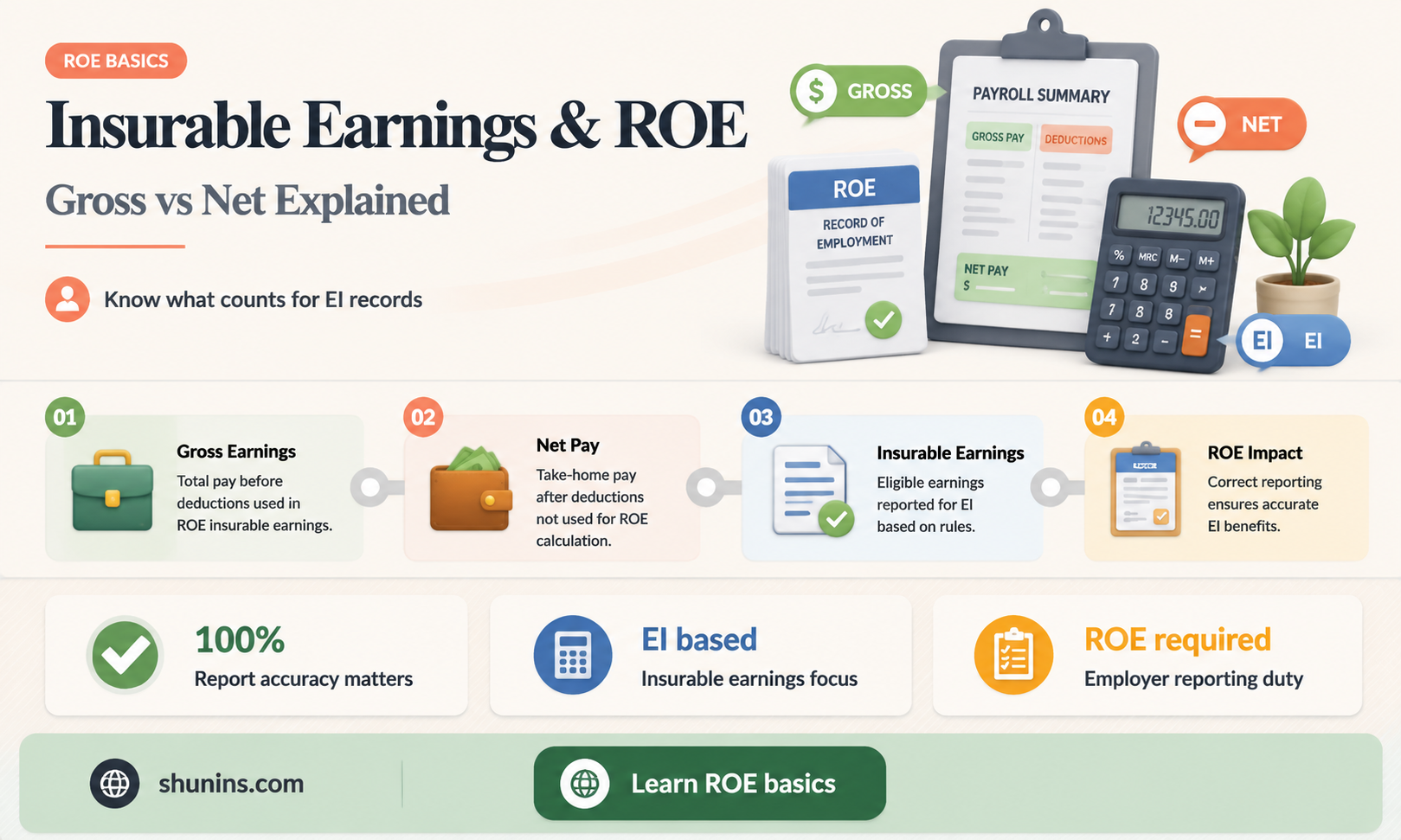

In Canada, the Record of Employment (ROE) form is used to record insurable earnings and hours for employees who have stopped working and experienced an interruption in earnings. Insurable earnings are all earnings reported on an employee's earnings statement prior to deductions. This includes wages, salaries, tips and gratuities, as well as any payments controlled by the employer. The ROE form is used to determine eligibility for employment insurance (EI) benefits and the amount of benefits to be received. The total insurable earnings on the ROE form may differ from an employee's gross income due to timing differences, as the ROE may span more than one calendar year.

| Characteristics | Values |

|---|---|

| Definition | Insurable earnings are the portion of your income that is used to calculate your contributions, and your employers' contributions to employment insurance premiums. |

| Calculation | Insurable earnings are all of those reported on your earnings statement prior to your deductions. |

| Maximum insurable earnings | For all of Canada except Quebec, the maximum insurable earnings amount in 2020 was $54,200, rising from $53,100 in the previous year. In 2023, the maximum insurable earnings were $61,500, and in 2024, they are $63,200. |

| Employment Insurance (EI) premiums | On every $100 of insurable earnings, you will pay $1.58 in employment insurance premiums. |

| Maximum EI premiums | The maximum amount of insurance premiums payable in 2020 is $865.36. |

| ROE form | The Record of Employment (ROE) form is completed by employers for employees receiving insurable earnings who stop working and experience an interruption of earnings. |

| ROE and T4 differences | ROEs usually span more than one calendar year, whereas T4s are calendar-year only. |

Explore related products

What You'll Learn

- Insurable earnings are all earnings reported before deductions

- Employers must include insurable earnings on ROE forms

- Insurable earnings are used to calculate employment insurance contributions

- There are timing differences between ROE and T4 insurable earnings

- Insurable earnings are all wages, salaries, tips and gratuities

![]()

Insurable earnings are all earnings reported before deductions

Insurable earnings must be paid partially or totally in cash. If a worker is paid entirely in cash, then the earnings are entirely insurable. If a worker is paid partly in cash and partly in non-cash benefits, only the cash portion of the payment is considered an insurable earning. If a worker is paid entirely in non-cash benefits, then there are no insurable earnings. However, there is an exception to this rule: if a worker is provided with board and lodging and paid remuneration for the same pay period, then the value of the board and lodging is included in insurable earnings.

The Canada Revenue Agency (CRA) is responsible for determining which types of earnings and hours are insurable. Employers are required by law to deduct Canada Pension Plan (CPP) contributions and EI premiums from most amounts they pay to their employees. Employers must then remit these amounts to the CRA along with their share of CPP contributions and EI premiums. The CRA also provides employers with an insurability ruling if they are unsure whether the earnings and hours of their employees are insurable.

When applying for employment insurance, it is important to know your total insurable earnings. This information is provided by the employer on the employee's Record of Employment (ROE). Service Canada will use the information in the ROE to determine whether the employee should receive EI and how much.

Life Insurance's Cash Accumulation: How Does It Work?

You may want to see also

Explore related products

![]()

Employers must include insurable earnings on ROE forms

In Canada, employers are required to complete a Record of Employment (ROE) form for employees who receive insurable earnings and experience an interruption in their earnings. This applies even if the employee does not intend to apply for Employment Insurance (EI) benefits.

Insurable earnings refer to the portion of an employee's income that is used to calculate their contributions to EI. This includes all wages, salaries, tips, and gratuities. It is important to note that insurable earnings are reported on an employee's earnings statement prior to any deductions. Employers must determine the number of consecutive pay periods that occurred during the period of employment, including any nil pay periods where the employee did not work and did not receive any earnings.

When completing the ROE form, employers must include the total insurable earnings in Block 15B. This may differ from the insurable earnings listed in Box 14 of the employee's T4 slip due to timing differences, as ROEs usually span more than one calendar year, while T4s are for a single calendar year. Employers must also enter the date in Block 12 and specify the pay period type in Block 6.

It is important for employers to ensure that all details on the ROE form are correct, as Service Canada will use this information to determine an employee's eligibility for EI and the amount they will receive. Any errors on the form can be corrected by contacting the Employer Contact Centre or referring to the ROE Web user guide.

Aflac Term Life Insurance: Protecting Your Family's Future

You may want to see also

Explore related products

$20.69 $21.99

![]()

Insurable earnings are used to calculate employment insurance contributions

In Canada, insurable earnings are used to calculate employment insurance (EI) contributions. This is a federally legislated program that provides temporary support for unemployed workers. Insurable earnings are the portion of an employee's income that is used to calculate their contributions to EI. These earnings are reported on an employee's earnings statement prior to any deductions. It is important to note that not all earnings are insurable. For instance, non-insurable earnings, such as top-ups to EI maternity benefits or sick pay credits used for early retirement, are excluded from an employee's insurable payroll.

Insurable earnings include all wages, salaries, tips, and gratuities. Any payment that is controlled by the employer is typically considered an insurable earning. This includes cash taxable benefits but does not encompass non-cash taxable benefits, with the exception of the value of board and lodging if provided in the same pay period as the employee's earnings. Controlled tips are also included in insurable earnings, whereas direct tips are excluded. Additionally, there is no age limit for deducting EI premiums, unlike CPP contributions.

To calculate EI premiums, employers are responsible for deducting these premiums from their employees' gross pay and remitting payments to the CRA. The premium amount is determined by multiplying an employee's insurable earnings by the current year's EI premium rate. This calculation ensures that EI contributions are based on the most recent rate. It is worth noting that EI premiums have a maximum threshold, which is updated annually. As of 2020, the maximum insurable earnings for employment insurance in Canada, except for Quebec, were $54,200. This means that any earnings above this amount would not be subject to additional EI premiums.

When applying for EI, individuals need to be aware of their total insurable earnings, which can be found on their Record of Employment (ROE). The ROE details the insurable earnings and the total premiums paid to EI and other programs. Service Canada uses the information on the ROE to determine eligibility for EI and the corresponding benefit amount. The number of weeks used to calculate benefits varies depending on the region's rate of unemployment. In regions with the lowest unemployment rates, the best 22 weeks are considered, while in other regions, the number of weeks ranges from 14 to 22.

Living with Psoriasis: Life Insurance and You

You may want to see also

Explore related products

![]()

There are timing differences between ROE and T4 insurable earnings

In Canada, insurable earnings are the portion of your income that is used to calculate your contributions to Employment Insurance (EI) and your employer's employment insurance premiums. These premiums allow you to benefit from Canada's employment insurance plan if you become unemployed. It is important to ensure that your insurable earnings are correct, as they will be used to calculate your EI payments.

When it comes to the Record of Employment (ROE) and T4 forms, there are timing differences that can lead to variations in the reported insurable earnings. ROEs usually span more than one calendar year, while T4s are specific to a single calendar year. This means that the ROE and T4 won't necessarily align, and there may be discrepancies in the reported insurable earnings.

For example, consider an employee with a weekly payroll who started in December 2010 and ended their employment in July 2011. On the ROE, 15A shows total insurable hours of 1027.50, which covers the entire period of employment. However, on the T4, box 24 shows EI insurable earnings for the calendar year of 2011 only, resulting in a different amount.

Additionally, the number of pay period boxes completed on the ROE depends on the period of employment, starting with the last day for which the employee was paid (Box 11) and working backward to the first day worked (Box 10). If an employee was absent for a pay period and had no insurable earnings, the corresponding box is left as $0.00. This can further contribute to the timing differences between the ROE and T4 insurable earnings.

To calculate total insurable earnings, employers need to determine the number of consecutive pay periods during the period of employment, including full, partial, and nil pay periods. This information is used to calculate the employee's EI payments and ensure they receive the correct amount of employment insurance premiums.

When Does Life Insurance Kick In?

You may want to see also

Explore related products

$18.99 $19.99

![]()

Insurable earnings are all wages, salaries, tips and gratuities

In Canada, insurable earnings are all wages, salaries, tips, and gratuities. They are the portion of an employee's income that is used to calculate their contributions to Employment Insurance (EI) and their employer's employment insurance premiums. Insurable earnings are typically included in most of the different kinds of compensation that employers provide to their employees. This includes cash payments and non-cash benefits, such as board and lodging. However, there are some exceptions, and not all earnings are considered insurable.

When an employee experiences an interruption in earnings, such as a period of unemployment, they may receive a Record of Employment (ROE) that lists their insurable earnings and the total of premiums paid to EI and other programs. The ROE is used by Service Canada to determine if the employee should receive EI and how much. Employers are required to issue an ROE for employees who receive insurable earnings and work insurable hours.

Insurable earnings are reported on an earnings statement or wage slip before any deductions for income tax, EI, Canada Pension Plan (CPP), health care plans, loan payments, and union dues. These deductions are made by employers and remitted to the Canada Revenue Agency (CRA) along with their share of CPP contributions and EI premiums. The CRA is responsible for determining which types of earnings and hours are insurable.

It is important for individuals to understand what specific money they receive from their employer counts as insurable earnings to ensure they are contributing the correct amount to EI. Additionally, when applying for EI, individuals need to know their total insurable earnings, as this information will be used to calculate their benefits.

Prescription Privacy: What Life Insurers Can Access

You may want to see also

Frequently asked questions

Insurable earnings are the portion of your income that is used to calculate your contributions to Employment Insurance (EI). All wages, salaries, tips and gratuities are considered insurable earnings.

To calculate your total insurable earnings, you need to add up all the insurable earnings you received during your pay periods. This includes all money made up to a certain threshold, which in 2020 was $54,200.

Total insurable earnings are not the same as gross income. Insurable earnings are reported on your earnings statement prior to your deductions. Gross income, on the other hand, refers to your total earnings before any deductions or taxes.

The ROE is a form that employers complete for employees who receive insurable earnings and experience an interruption of earnings. The ROE details an employee's work history, including insurable earnings and insurable hours. Service Canada uses the information in the ROE to determine eligibility for EI and calculate the amount.