Life insurance is often seen as a reliable way to provide for loved ones after death. One of its biggest advantages is the tax relief it offers. Typically, the death benefit your beneficiaries receive isn't taxed as income, meaning they get the full amount to use for expenses like paying off debts, covering funeral costs or securing their future. However, there are a few situations where taxes could come into play, and it's important to know when that might happen.

Explore related products

What You'll Learn

![]()

Interest on life insurance benefits is taxable income

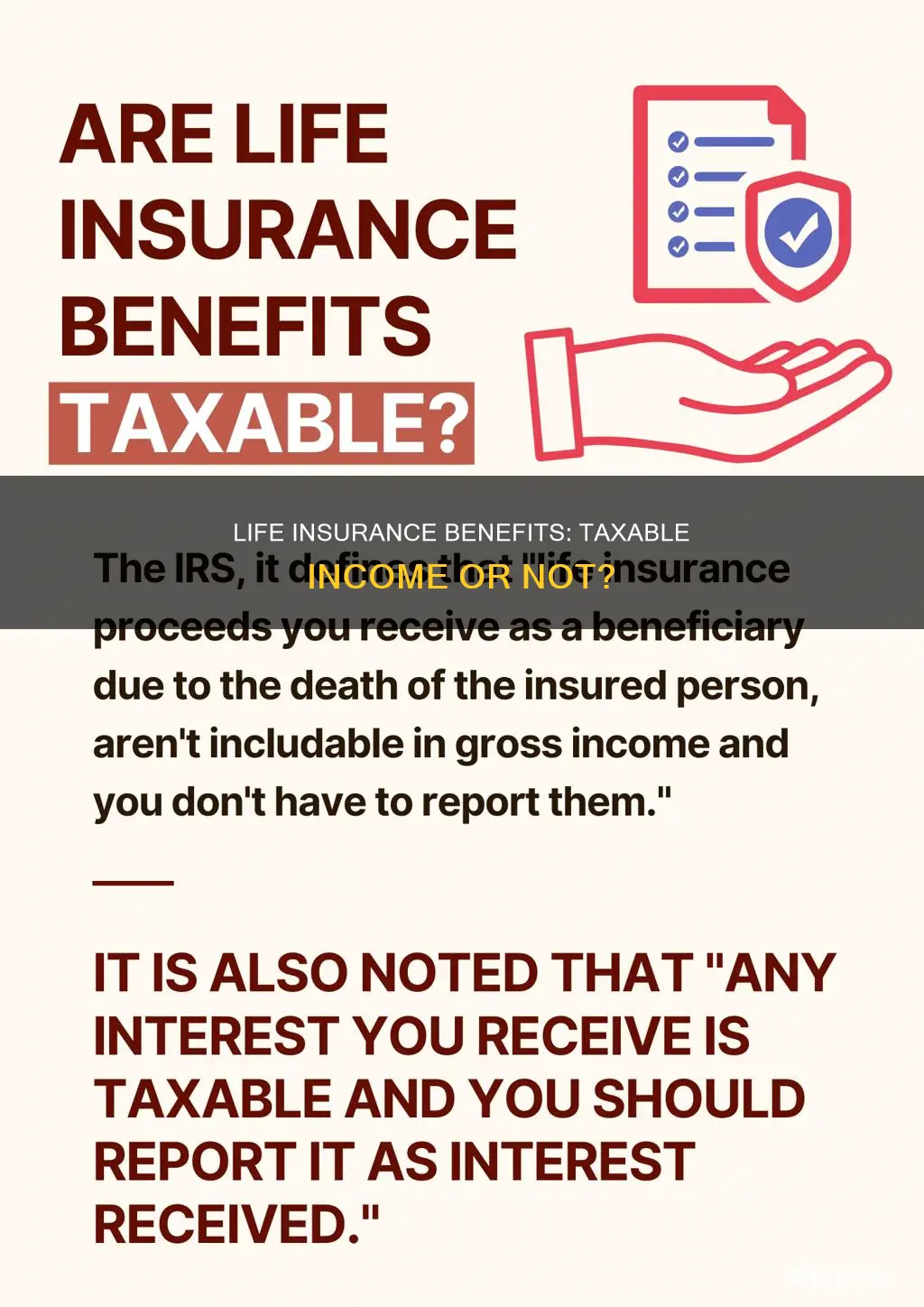

Life insurance benefits are generally not taxable income. However, interest on life insurance benefits is taxable income. If you receive life insurance benefits as a beneficiary due to the death of the insured person, you do not need to include this in your gross income or report it. Nevertheless, if you receive any interest on top of the benefits, this is taxable and must be reported as interest received.

For example, if your loved ones choose to receive the life insurance payout in instalments instead of a lump sum, any interest that builds up on those payments could be taxed. This extra money from interest is considered taxable income, even though the original death benefit is not.

If the policy was transferred to you for cash or other valuable consideration, the exclusion for the proceeds is limited to the sum of the consideration you paid, additional premiums you paid, and certain other amounts. There are some exceptions to this rule. You report the taxable amount based on the type of income document you receive, such as a Form 1099-INT or Form 1099-R.

Life Insurance and Mass Shootings: What Coverage is Offered?

You may want to see also

Explore related products

![]()

Naming an estate as a beneficiary may trigger estate taxes

With the estate as the beneficiary, the proceeds are first distributed to the estate and then passed to the heirs according to the terms of the will. This can have several negative consequences. One of the main disadvantages is the potential for higher taxes. Estates are subject to a five-year rule for distributions, whereas most individual beneficiaries can take advantage of a 10-year rule. The shorter timeline may result in higher annual distributions, which can lead to a higher overall tax bill.

Additionally, larger distributions can lead to higher Medicare charges and increased taxes on Social Security payments. Naming an estate as a beneficiary may also expose assets to creditor invasion, higher estate administration costs, and an increased potential for legal challenges from disgruntled heirs.

Therefore, it is generally recommended to name specific individuals, such as spouses, children, or grandchildren, as beneficiaries, rather than the estate itself. By designating individuals or qualifying trusts as beneficiaries, policyholders can provide greater flexibility in distribution options, avoid probate, and potentially reduce the overall tax burden on heirs.

Life Insurance Coverage for Grandchildren: What You Need to Know

You may want to see also

Explore related products

![]()

Choosing an annuity payout may result in taxes on interest

Life insurance benefits are generally not considered taxable income. However, there are certain scenarios where the proceeds may be taxed. One such scenario is when the beneficiary chooses to receive the death benefit as an annuity, which is a series of payments over several years. In this case, any interest accrued by the annuity account may be subject to taxes.

When choosing an annuity payout, it's important to understand how it will be taxed. Annuities can be funded with either pre-tax or post-tax money, and the taxation will depend on this funding source. If an annuity is funded with pre-tax money, the entire amount of the payout will be taxable as income when it is received. On the other hand, if an annuity is funded with post-tax money, only the earnings will be taxable. This includes any interest accrued over time.

The timing of withdrawals can also impact the taxation of annuity payouts. Withdrawing funds from an annuity before the designated time period, such as before the age of 59 1/2, may result in early withdrawal penalties. Additionally, the tax status of the contract, whether qualified or non-qualified, will determine how much of the withdrawal is taxed. For non-qualified annuities, only the earnings portion of the withdrawal is typically taxed.

It's worth noting that beneficiaries may have to pay income taxes on the interest accrued in the annuity account, as this is considered taxable income. Consulting with a qualified tax professional is advisable to understand the specific tax implications of choosing an annuity payout.

AIG Life Insurance: AM Best Rating Explained

You may want to see also

Explore related products

![]()

Withdrawing from a whole life policy may be taxable

Whole life insurance policies are a form of permanent life insurance, which includes a cash value component. This means that the policy has the potential to grow in value over time and accrue interest. Withdrawing money from this cash value component can, in some cases, trigger tax consequences.

Firstly, it is important to note that certain types of whole life policies may not allow withdrawals from the cash value at all. If your policy does permit withdrawals, the amount you can withdraw without tax consequences is typically limited to your basis in the policy. Your basis is the total amount of premiums you have paid into the policy, minus any dividends received or previous withdrawals. Withdrawing an amount equal to or less than your basis is generally not taxable, as you have already paid income tax on these dollars.

However, if you withdraw more than your basis, the excess amount will likely be considered taxable income. This is because the earnings or interest accrued on your policy grow tax-deferred while inside the policy, and therefore become subject to income tax when withdrawn. Withdrawals are usually treated as coming out of your policy basis first, so if you withdraw more than your basis, a portion of the withdrawal will be taxed as ordinary income.

It is also important to consider the potential impact of surrender charges when withdrawing from your policy. These charges may apply even if you only withdraw up to your basis. One way to avoid these charges is to take out a policy loan from the insurance company, using the cash value in the policy as collateral. While the loan amount is generally not treated as taxable income if repaid, it will accrue interest, which is not tax-deductible.

In summary, withdrawing from a whole life policy may be taxable if you withdraw more than your basis in the policy. The portion of the withdrawal that exceeds your basis will typically be treated as taxable income, subject to ordinary income tax rates. Additionally, surrender charges or loan interest may apply, further reducing the net amount received. Therefore, it is essential to carefully review the terms of your policy and consult a tax advisor before making any withdrawals.

Race and Life Insurance: Does It Affect Premiums?

You may want to see also

Explore related products

![]()

Surrendering a whole life policy may be taxable

Surrendering a whole life insurance policy may come with tax implications. When you surrender a policy, you receive the cash surrender value (CSV), which is the cash value minus any surrender charges. If the CSV is higher than the total amount of premiums you've paid into the policy (your cost basis), the excess amount is typically taxed as ordinary income.

For example, if you've paid $30,000 in premiums and the CSV of your policy is $45,000, the difference of $15,000 would be taxed as ordinary income, possibly pushing you into a higher tax bracket for that year.

It's important to note that the surrender charge typically applies only within the first 10 to 20 years of owning the policy, and it usually phases out over time. Insurers often reduce surrender charges by a certain percentage each year during the initial period.

Before surrendering your policy, it's advisable to consult a financial advisor to understand the potential tax implications and explore alternative options, such as withdrawing from the cash value or taking out a loan against the policy.

Additionally, if you have a "modified endowment contract" (MEC), the tax rules are different. In this case, it's best to consult a financial professional to understand the specific tax implications.

Whole Foods: Free Life Insurance for Employees?

You may want to see also

Frequently asked questions

False. Life insurance benefits are not considered taxable income and are generally tax-free.

No, beneficiaries do not usually have to pay taxes on the death benefit, especially if it is paid as a lump sum.

Yes, there are some cases where taxes may be payable. For example, if the benefit is paid in installments, the interest accrued will be taxable.

Yes, according to the IRS, if an employer-paid plan pays out more than $50,000, it may be taxable.

Yes, if the value of the estate, including the life insurance proceeds, exceeds the federal estate tax threshold, estate taxes must be paid on the amount over the limit.