When it comes to buying a home, there are a multitude of factors to consider. While many people focus on the property's price, it is important to remember that there are additional costs to homeownership, such as property taxes and homeowners insurance. These costs can be built into your mortgage payments, but it is not a given. In some cases, you may need to pay these expenses separately, so it is crucial to understand how these costs interact with your mortgage. This knowledge will help you navigate your financial responsibilities effectively and confidently.

| Characteristics | Values |

|---|---|

| Are property taxes built into a mortgage? | Property taxes are included in most mortgage payments. |

| Are homeowners insurance built into a mortgage? | Homeowners insurance is commonly paid through an escrow account. |

| What is an escrow account? | An escrow account is set up by the mortgage lender to collect and manage the funds needed for property taxes and homeowners insurance. |

| What are the benefits of paying through an escrow account? | Paying through an escrow account makes budgeting for taxes predictable. |

| What if I don't want to use an escrow account? | If you choose not to use an escrow account, you will be responsible for making those payments directly to your local tax authority. |

Explore related products

$4.99 $14.99

What You'll Learn

![]()

Escrow accounts and how they work

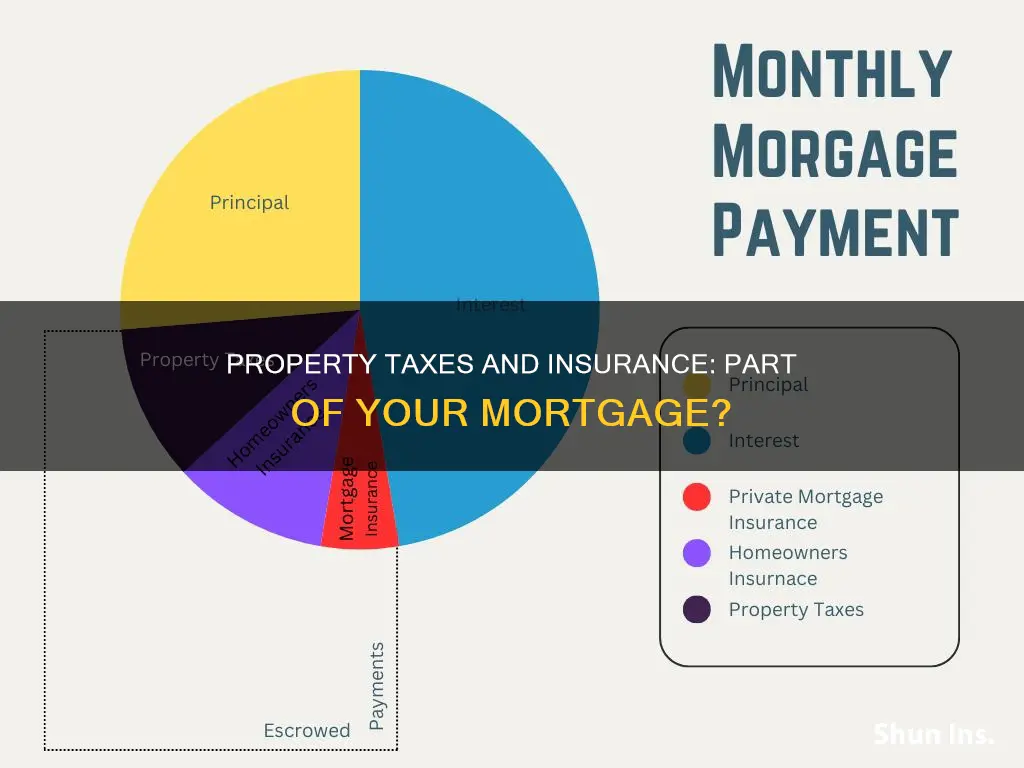

An escrow account is a financial intermediary account that is commonly required by mortgage lenders. It is set up by the lender or a third party like an escrow company, escrow agent, or mortgage servicer. The account is funded through your monthly mortgage payment, which is typically higher than it would be without escrow. The lender calculates your annual tax and insurance payments, divides the amount by 12, and adds the result to your monthly mortgage statement. The lender then deposits the escrow portion of your mortgage payment into the account and pays your insurance premiums and real estate taxes when they are due.

Escrow accounts are designed to manage specific recurring expenses related to homeownership, such as property taxes and homeowners insurance. These expenses are included in your mortgage payment, and the lender pays them on your behalf when they are due. This means that you don't have to worry about saving for or paying these large expenses separately, and you can avoid late payment fees and penalties. Additionally, if you change insurance providers or policies, you will need to provide the new policy information to your lender or servicer.

The amount needed for your escrow account depends on your property taxes and homeowners insurance costs, which can change from year to year. To ensure that there are enough funds in the account, the lender will perform an escrow analysis each year. This involves reviewing the account activity from the previous 12 months and making projections for the upcoming 12 months. If there is a shortage or surplus in the account, your monthly escrow payments may be adjusted accordingly.

It is important to note that escrow accounts do not cover all costs associated with homeownership. For example, payments for utilities, homeowners association (HOA) fees, and supplemental tax bills are typically handled directly by the homeowner. Additionally, some lenders may give you the option to pay taxes and insurance directly to the insurer or tax authority, rather than through an escrow account. However, this may require more proactive financial planning and saving to ensure that you can cover these expenses when they are due.

Earthquake Insurance in Seattle: Worth the Cost?

You may want to see also

Explore related products

$11.25 $16.99

![Manitoba Lands for Sale by Crotty & Cross, Real Estate Brokers, Financial and Insurance Agents Funds Invested on First Mortgage Security, Rents Collected, Taxes Paid, and 1893 [Leather Bound]](https://m.media-amazon.com/images/I/617DLHXyzlL._AC_UY218_.jpg)

![]()

Property taxes and how they are calculated

Property taxes are calculated by multiplying the local tax rate by a specific property's assessed value. The assessed value of a property is determined by an assessor from the city, based on the home's size, recent sales in the area, the state of the local real estate market, and other factors. It is important to note that the assessed value is different from the appraised or market value, as it only considers the taxable value.

Property taxes are typically included in mortgage payments and are paid through an escrow account. This account is set up by the mortgage lender to collect funds for property taxes and insurance, ensuring timely payments. However, some homeowners may opt to pay property taxes separately, directly to the local tax authority.

The inclusion of property taxes in mortgage payments can vary depending on the loan and location. Property taxes can significantly impact monthly mortgage payments, and it is essential for homeowners to understand these components to effectively manage their finances.

In some cases, property taxes may be calculated based on the property's appraised value. For example, if a property is appraised at $400,000, and the assessed value is $100,000 (25% of the appraised value), the tax rate set by the county commission is applied. In this case, the tax rate of $2.50 per hundred dollars of assessed value would be calculated as $100,000 divided by 100, and then multiplied by the tax rate.

Property taxes are subject to fluctuations, and these changes can impact monthly mortgage payments. Additionally, property taxes may be eligible for exemptions, such as agricultural exemptions, which can provide tax relief for properties used for agricultural purposes.

Hospital Insurance: Is It Worth the Cost?

You may want to see also

Explore related products

![]()

Homeowners insurance and what it covers

When it comes to mortgages, property taxes and homeowners insurance are often included in the monthly payment. These costs are typically managed through an escrow account set up by the lender. An escrow account acts as a financial intermediary, collecting funds for property taxes and insurance and paying them when they are due. This guarantees adherence to the lender's terms and conditions.

Now, let's delve into homeowners insurance and what it covers:

Homeowners insurance provides financial protection for your home and belongings in the event of damage or loss. It covers repair or replacement costs for your home and personal belongings, including expensive items like jewelry, art, and collectibles. The coverage extends to detached structures such as garages and sheds, usually up to a certain percentage of the insured value of the main residence. It also provides liability protection if you or your family members cause injury or damage to someone else or their property, including damage caused by pets. This liability coverage includes legal defence costs and any court-awarded compensation, up to the limit stated in your policy.

In addition to the standard coverage mentioned above, homeowners insurance also provides coverage for additional living expenses (ALE) incurred if you need to live away from home due to damage from an insured disaster. This includes hotel bills, restaurant meals, and other costs above your usual living expenses. However, it's important to note that ALE coverage has limits, and some policies include a time restriction.

While standard homeowners insurance covers damage due to fire, wind, snow, hurricanes, hail, lightning, and other listed disasters, it typically excludes coverage for floods and earthquakes and routine wear and tear. To protect against these perils, additional insurance policies may be necessary, depending on your location and specific risks.

Furthermore, homeowners insurance policies have coverage limits and deductibles. The deductible is the amount you must pay towards a claim before the insurance company covers the rest. By choosing a higher deductible, you can lower your insurance premium. It's important to carefully review the coverage limits, exclusions, and deductibles to ensure you have adequate protection for your home and belongings.

Patent Insurance: Worth the Investment?

You may want to see also

Explore related products

![]()

Mortgage insurance and when it's required

Mortgage insurance, also known as private mortgage insurance (PMI), is typically required when a borrower makes a down payment of less than 20% of the total purchase price of a home. It protects the lender in the event that the borrower defaults on the loan. By purchasing mortgage insurance, borrowers with smaller down payments can qualify for loans that they may not have otherwise been eligible for. Mortgage insurance is usually included in the total monthly payment made to the lender, or it can be included in the costs at closing, or both.

Mortgage insurance is often required for Federal Housing Administration (FHA) loans and US Department of Agriculture (USDA) loans. In the case of FHA loans, mortgage insurance premiums are paid to the FHA and are required for all FHA loans. For USDA loans, the program is similar to the FHA, but typically cheaper. Similar to FHA loans, the insurance premium can be rolled into the mortgage to avoid paying out of pocket, but this increases the overall loan amount and costs.

For conventional loans, lenders can arrange for mortgage insurance with a private company. Private mortgage insurance rates vary depending on the down payment amount and credit score, but they are generally cheaper than FHA rates for borrowers with good credit. Private mortgage insurance is usually paid monthly, with little to no upfront payment. Under certain circumstances, PMI can be cancelled. As an alternative to mortgage insurance, some lenders may offer a "piggyback" second mortgage, but this may not always be the cheaper option.

Mortgage Insurance Percentages in DC: What You Need to Know

You may want to see also

Explore related products

![]()

Additional insurance and why you might need it

When you take out a mortgage, your bank or lender will likely require you to have homeowners insurance, also known as hazard insurance. This type of insurance covers losses to your home, its contents, and any additional living expenses incurred due to a loss of its use. It also provides liability coverage for accidents that occur at the home or caused by the homeowner. While homeowners insurance is a common requirement, there are several other types of additional insurance you may need, depending on your specific circumstances and location.

One important type of additional insurance to consider is mortgage insurance, also known as private mortgage insurance (PMI). This type of insurance protects your lender in case you default on your loan. While it doesn't directly benefit the homeowner, it is often required by lenders if you make a down payment of less than 20% of the total loan amount. The cost of PMI is typically included in your mortgage payment, and you may be able to cancel the policy once your loan balance falls below a certain threshold.

Depending on where you live, you may also need to consider flood insurance or hurricane protection. If your home is located in a designated flood plain or an area with a high risk of flooding, your lender will likely require you to have flood insurance. Even if your home is not in a high-risk area, you may still want to consider this added protection, as standard homeowners insurance policies usually exclude flood damage. Similarly, if you live in an area prone to earthquakes, such as certain parts of the West Coast, you may need to purchase earthquake insurance. This coverage is often sold as an endorsement to your basic policy or as a separate policy in certain states.

Another type of insurance to consider is title insurance, which protects against issues related to the property's title. While lender's title insurance is typically required when you have a mortgage, you may also want to consider purchasing owner's title insurance for added protection, especially if you're buying the property with cash. Consulting with an attorney can help you identify any potential issues and determine if this type of insurance is necessary for your situation.

By understanding the various types of additional insurance available and assessing your specific needs, you can ensure that you have the necessary coverage in place to protect your home and financial interests.

Homeowners Insurance: Landslide Coverage and Exclusions

You may want to see also

Frequently asked questions

An escrow account is set up by your lender and acts as a financial intermediary, collecting funds for property taxes and insurance and paying them when they are due. It is essentially a savings account managed by your mortgage servicer.

Most mortgage lenders require homeowners insurance and an escrow account to manage insurance payments. However, some lenders may give you the option to pay insurance and taxes directly.

Homeowners insurance provides coverage against specific damages and incidents affecting your home. Mortgage insurance protects the lender if you default on the loan.

Your monthly mortgage payment often consists of four parts: principal, interest, taxes and insurance. Collectively known as PITI, these components make up most or all of your monthly mortgage payment.

Your mortgage lender will estimate your annual tax obligation, divide it into equal monthly payments and add it to your mortgage payment.