Whole life insurance is a permanent life insurance policy that provides coverage for the entirety of the insured person's life. It is more expensive than term life insurance but offers a guaranteed death benefit and a savings component, allowing the policyholder to build cash value over time. This cash value can be accessed through withdrawals, loans, or by surrendering the policy. In the event of the policyholder's death, the beneficiary will receive the death benefit, and if the policy has matured, they may also receive the accumulated cash value. To redeem a whole life insurance policy, the policyholder or their nominee must notify the insurance company and submit the required documents, which typically include a claimant statement form, death certificate, KYC documents, and bank details.

| Characteristics | Values |

|---|---|

| Coverage | Throughout the life of the insured person |

| Tax | Tax-free death benefit |

| Savings | Cash value may accumulate |

| Interest | Accrues on a tax-deferred basis |

| Premium | Level premiums |

| Cash value | Can be drawn on or borrowed from |

| Interest rate | Fixed rate of interest |

| Withdrawals | Tax-free up to the value of total premiums paid |

| Loans | Charged at a lower rate than personal or home equity loans |

| Death benefit | Reduced by withdrawals and outstanding loan balances |

| Dividends | Can be reinvested into the cash value |

| Riders | Can be added for an additional cost |

| Surrender | Ends the insurance policy |

Explore related products

What You'll Learn

- Whole life insurance provides coverage for the entirety of the insured person's life

- It has a savings component, allowing cash value to accumulate

- Interest accrues on a tax-deferred basis

- Whole life insurance policies are more expensive than term life insurance policies

- The cash value of a whole life policy can be used to pay monthly premiums

![]()

Whole life insurance provides coverage for the entirety of the insured person's life

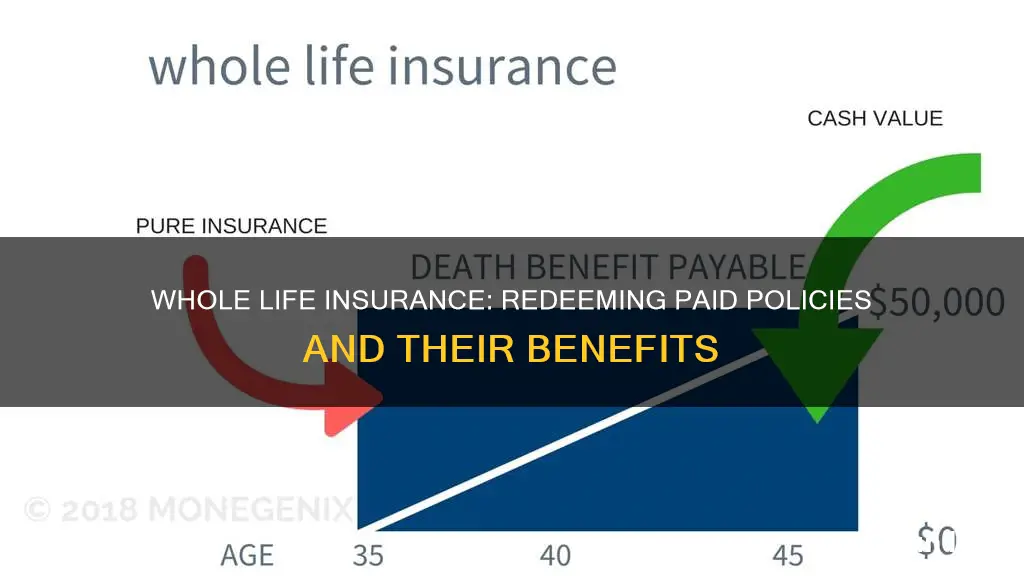

Whole life insurance is a type of permanent life insurance that provides coverage for the entirety of the insured person's life. It combines an investment account, known as the "cash value", with an insurance product. This means that, as long as the premiums are paid, the policy remains active for the entire life of the insured person, and the beneficiaries will receive a death benefit upon the insured person's death.

The "cash value" component of whole life insurance functions as a savings and investment vehicle for the policyholder. It grows over time, providing the policyholder with a source of funds that can be accessed through policy loans or withdrawals. This money can be used for various purposes, such as retirement, college tuition, or emergency funding. The "cash value" also allows the policyholder to borrow money from the insurance company at a low-interest rate, with the "cash value" serving as collateral.

Whole life insurance policies typically have level premiums, meaning the amount paid every month remains the same throughout the duration of the policy. These premiums are generally higher than those of term life insurance policies, as whole life insurance provides coverage for the entire life of the insured, whereas term life insurance only covers a specific number of years.

Whole life insurance also offers a guaranteed death benefit, which means that the beneficiaries will receive a set amount of money upon the death of the insured person, regardless of how much has been paid in premiums. This is in contrast to term life insurance, where the death benefit may depend on the amount of coverage chosen and the length of the policy.

In summary, whole life insurance provides lifelong coverage, a savings and investment component in the form of "cash value", and a guaranteed death benefit. These features make it a valuable option for individuals seeking long-term financial security and protection for their loved ones.

Life Insurance: Pre-Death Benefits and Payouts Explained

You may want to see also

Explore related products

![]()

It has a savings component, allowing cash value to accumulate

Whole life insurance is a type of permanent life insurance that provides coverage for the entirety of the insured person's life. It is distinguished by its savings component, which allows cash value to accumulate over time. This cash value can be invested in an account that grows at a fixed rate, with interest accruing on a tax-deferred basis. This feature sets whole life insurance apart from term life insurance, which only provides coverage for a specific number of years and does not have a cash savings component.

The savings component of whole life insurance, known as the "cash value", offers several benefits to policyholders. Firstly, it allows policyholders to build up a substantial sum of money over time, which can be accessed through withdrawals or loans. This can be particularly advantageous for those who wish to supplement their income during retirement or make large purchases. Secondly, the cash value grows in a tax-efficient manner. Withdrawals up to the total amount of premiums paid are typically tax-free, and any investment gains may be taxable at a lower rate if withdrawn during retirement.

Policyholders can choose to make additional payments beyond the scheduled premium to purchase extra coverage, known as paid-up additions (PUA). Policy dividends can also be reinvested into the cash value, further increasing the overall return. Over time, the dividends and interest earned on the policy's cash value can exceed the total amount of premiums paid.

However, it is important to note that withdrawals and outstanding loan balances will reduce the death benefit paid out to beneficiaries. Therefore, policyholders should carefully consider their options before accessing the cash value of their whole life insurance policy.

Heart Surgery: A Life Insurance Deal-Breaker?

You may want to see also

Explore related products

![]()

Interest accrues on a tax-deferred basis

Whole life insurance is a type of permanent life insurance that covers the insured person for their entire life. It provides a tax-free death benefit and contains a savings component, known as the cash value, which may accumulate interest over time. This interest accrues on a tax-deferred basis, allowing the policyholder's money to grow faster as it is not reduced by annual taxes.

The tax-deferred status of whole life insurance means that interest accumulates on the cash value without being subject to annual taxation. This results in a higher base amount for interest calculations, leading to more significant gains over time. The tax-deferred nature of whole life insurance is particularly advantageous for individuals in higher income tax brackets during their prime working years. By withdrawing funds later in life when their tax bracket may be lower, policyholders can benefit from reduced taxation on their earnings.

The cash value component of whole life insurance policies grows over time and can be accessed by the policyholder through withdrawals or loans. Withdrawals up to the total amount of premiums paid are typically tax-free. However, if the withdrawal exceeds this amount and includes investment gains, the additional amount is subject to taxation. Policyholders can also take out loans against the cash value, which are not treated as taxable income.

The ability of whole life insurance to accumulate cash value makes it not just a safety net for beneficiaries but also a potential investment vehicle for the insured. The tax-deferred nature of interest accumulation further enhances the attractiveness of whole life insurance as an investment option.

In summary, the tax-deferred basis of interest accumulation in whole life insurance policies offers policyholders the benefit of tax-free growth on their cash value. This feature, along with the ability to access funds through withdrawals or loans, makes whole life insurance a versatile financial tool for individuals seeking both insurance coverage and investment opportunities.

Irrevocable Life Insurance Trusts: Taxable or Not?

You may want to see also

Explore related products

![]()

Whole life insurance policies are more expensive than term life insurance policies

The higher cost of whole life insurance is due to its permanent nature and the inclusion of a cash value component. Whole life insurance premiums are significantly higher because the coverage typically lasts a lifetime, and the policy accumulates cash value. Term life insurance, on the other hand, is temporary and does not build cash value, making it a more affordable option.

While term life insurance offers basic protection at a lower cost, whole life insurance provides additional benefits such as lifelong coverage, guaranteed death benefit, and the ability to borrow against or withdraw from the policy. Whole life insurance is ideal for those who want coverage for their entire lives and desire the added flexibility of a cash value component. However, the complexity and high cost of whole life insurance may make it challenging for some consumers to maintain payments.

When deciding between term and whole life insurance, it is essential to consider your financial goals, budget, and specific needs. Term life insurance may be sufficient for those seeking coverage for a specific period, such as during their working years or until their children become financially independent. On the other hand, whole life insurance is suitable for those seeking lifelong coverage, building cash value, or ensuring final expenses are covered, regardless of when death occurs.

Life Insurance Proceeds: Can Creditors Garnish Your Money?

You may want to see also

Explore related products

![]()

The cash value of a whole life policy can be used to pay monthly premiums

Whole life insurance is a type of permanent life insurance that provides coverage for the entire life of the insured person. It combines an investment account, known as the "cash value", with an insurance product. The cash value of a whole life policy can be used in several ways, including paying monthly premiums.

The cash value of a whole life policy is a savings component that accumulates over time. It is funded by a portion of the premium payments made by the policyholder. This cash value grows over time and can be accessed by the policyholder through loans or withdrawals. It is important to note that withdrawals are tax-free up to the total amount of premiums paid.

Using the cash value to pay monthly premiums means that the policyholder can effectively cover their insurance costs without having to pay out of pocket. This can be especially useful if the policyholder is facing financial difficulties or wants to free up money for other purposes.

However, it is important to consider the potential impact on the death benefit. Withdrawals and outstanding loan balances against the cash value will reduce the death benefit paid out to beneficiaries. Therefore, it is crucial for policyholders to carefully weigh their options and make informed decisions about using the cash value to pay premiums.

In summary, the cash value of a whole life insurance policy offers policyholders flexibility and can be used to pay monthly premiums. While this can provide financial relief, it is important to understand the potential consequences on the death benefit to ensure that the policy continues to meet the needs of the insured and their beneficiaries.

American Life Insurance: Legit or a Scam?

You may want to see also

Frequently asked questions

Whole life insurance is a type of permanent life insurance that provides coverage for the entirety of the insured person's life. It combines an investment account, known as "cash value", with a life insurance product. Whole life insurance policies are typically more expensive than term life insurance policies.

Whole life insurance offers several benefits, including lifelong coverage, a guaranteed minimum rate of return on the cash value, fixed premium payments, and a guaranteed death benefit amount. It also allows the policyholder to access the cash value during their lifetime.

Whole life insurance rates are determined by factors such as age, medical history, and coverage goals. The premiums are fixed throughout the policy, and a portion of the premiums is usually invested in an account that grows over time. The death benefit is certain, and the beneficiary will receive the accrued cash value when the policy ends.

In the event of the death of the policyholder, the nominee will need to notify the insurance company and submit the required documents, including a claimant statement form, death certificate, KYC documents, and bank details. If the policyholder survives the policy term, they can redeem the policy by visiting the insurance company's branch office and submitting the necessary documents.

Whole life insurance offers some tax benefits. The cash value component of the policy grows tax-free, and withdrawals up to the total amount of premiums paid are typically not taxable. However, withdrawals exceeding the total premiums paid may be subject to taxes, and there may be tax consequences if the policy is surrendered or lapses.