Life insurance is a policy that provides a death benefit payout to beneficiaries after the policyholder's death. There are five main types of life insurance: term life insurance, whole life insurance, universal life insurance, variable life insurance, and final expense life insurance. Each type of life insurance is designed to meet specific needs and budgets, with variations in coverage length, complexity, coverage amount, cash value, and other features. Term life insurance, for example, is geared towards those seeking coverage for a certain number of years, while whole life insurance offers lifelong coverage. Universal life insurance provides flexibility, while variable life insurance offers higher risk and potentially higher returns. Final expense life insurance helps cover bills and expenses after the policyholder's death. Understanding these options is crucial to choosing the best plan for one's family and financial goals.

Types of Life Insurance

| Characteristics | Values |

|---|---|

| Purpose | To provide money to your loved ones to help protect them financially after you're gone. |

| Number of Main Types | 5: Term, Whole, Universal, Variable, and Final Expense. |

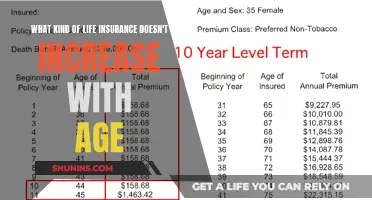

| Term Insurance | Temporary coverage for a specific period, e.g., 1 year, 10 years, 20 years, or until a specified age. It is generally more affordable than permanent insurance. |

| Whole Life Insurance | Permanent coverage for your entire lifetime. It includes a savings component and tends to be more expensive. |

| Universal Life Insurance | Permanent coverage with more flexibility than Whole Life. It treats premium, death benefit, and cash value as separate elements. |

| Variable Life Insurance | A riskier type of permanent insurance with a variable cash value based on payments and performance of selected investments. |

| Final Expense Life Insurance | Designed to cover bills and expenses, such as funeral costs and medical bills, that your family may face after your passing. |

| Dependent Life Insurance | Coverage provided if a spouse or dependent child passes away, typically used to offset expenses that occur after death. |

| Considerations | Family size, income, financial aspirations, and health status. |

Explore related products

$15.95

What You'll Learn

![]()

Term life insurance

There are several types of term life insurance plans:

- Fixed Term: The most popular choice. It is the most basic version and lasts 10, 20, or 30 years. The premiums remain static.

- Increasing Term: Allows the policyholder to scale up the value of their death benefit throughout the term. Premiums increase slightly over time, and these policies tend to cost more but deliver a larger payout.

- Decreasing Term: Reduces the premium payments over time, resulting in a smaller death benefit. This type of insurance makes sense for those who predict they will have fewer financial obligations as they age.

- Annual Renewable: Provides coverage on a yearly basis and must be renewed by the end date to continue coverage. Premiums usually increase each time the plan is renewed, and this option is best for those who need short-term coverage.

High Cholesterol and Life Insurance: What's Possible?

You may want to see also

Explore related products

$12.99 $14.95

![]()

Whole life insurance

The cash value of whole life insurance typically works like a savings account. It grows over time, but the specifics can vary by company and policy. In most cases, a portion of your premium goes into this account and earns interest, gradually increasing the cash value. You may also be able to borrow against the cash value, withdraw some money, or end the policy for its cash value. The cash value in your policy is guaranteed to grow over time, tax-deferred, and is eligible for dividends every year.

Life Insurance at 65: What You Need to Know

You may want to see also

Explore related products

![]()

Universal life insurance

One of the key advantages of universal life insurance is its flexibility. Policyholders can adjust their premium payments within certain limits, making it a good option for those with variable incomes. Additionally, universal life insurance provides the opportunity to increase the death benefit as you build the cash value. This flexibility also extends to the method of cash value growth, allowing policyholders to choose between a secured rate or investment-based growth.

However, there are some disadvantages to universal life insurance. The interest rate is not guaranteed, and if interest rates drop, the cash value may not perform well. Additionally, if the investments underperform or the policyholder underpays for too long, it could affect the death benefit or cause the policy to lapse. Universal life insurance can also be more complex than other forms of life insurance, requiring careful management of premium payments and investment choices.

Overall, universal life insurance offers a flexible way to obtain permanent life insurance coverage, making it a good option for those seeking adjustable premium payments and the potential for higher returns through investment options.

Prudential Life Insurance: Is It Worth the Hype?

You may want to see also

Explore related products

![]()

Variable life insurance

Before buying variable life insurance, it is important to review all the costs, including fees, and determine whether you can afford this type of policy. You should also determine how much coverage you need to meet your goals and how long you will likely need the insurance. Generally, investments with a longer time horizon can carry more risk than those with a shorter time horizon because they have more time to recoup any losses in the market. It is also important to ensure that the insurance company providing the policy is reputable or financially sound.

Supplemental Life Insurance: How and When Payouts Happen

You may want to see also

Explore related products

![]()

Final expense life insurance

Life insurance is a policy that provides a death benefit payout to beneficiaries if the policyholder dies while the policy is active. There are five main types of life insurance: term life insurance, whole life insurance, universal life insurance, variable life insurance, and final expense life insurance. Each type of life insurance is designed to fill a specific coverage need.

Final expense insurance is one of the most affordable types of life insurance, with policies starting at $63 per month for coverage ranging from $5,000 to $40,000. The application process is quick and easy, and coverage can be issued in days, sometimes even on the same day. Final expense policies can build cash value over time, which can be withdrawn or used to borrow money or pay premiums.

Unlike traditional life insurance policies, final expense insurance usually does not require a medical exam. Policyholders simply have to answer a few health questions, and their coverage can start immediately. Final expense insurance offers competitive, fixed premiums that do not change over time, and the benefit can be used to cover funeral and burial costs, medical needs, or anything else that will help loved ones.

Teamsters' Life Insurance: What Happens Post-Retirement?

You may want to see also

Frequently asked questions

Life insurance is a contract between an insurance policyholder and an insurer, where the insurer promises to pay a designated beneficiary a sum of money in exchange for a premium, upon the death of the insured person.

Term life insurance and permanent life insurance are the two main types. Term life insurance covers you for a set number of years, while permanent life insurance covers you for the rest of your life.

Term life insurance is a simple, low-cost policy that replaces your income when you die. It is typically sold in lengths of 1, 5, 10, 15, 20, 25 or 30 years.

Permanent life insurance remains in place as long as the premium is being paid. It also has a cash value that increases over time, allowing the policyholder to borrow against that cash value. Whole life, universal life, variable life, and variable universal life are types of permanent life insurance.

The best type of life insurance depends on your needs and budget. Factors such as your family size, income, financial aspirations, budget, age, health, preferences, and risk tolerance should be considered when choosing a policy.