Gap insurance is an optional insurance policy that covers the difference between the current market value of a vehicle and the balance remaining on its finance or lease contract in the event of a total loss. While it is not a state requirement, Toyota does offer gap insurance to its customers. This insurance is only available at the time of financing and may be included in the loan or lease, paid off in monthly instalments. Gap insurance can also be purchased from car insurance companies or banks and credit unions, and is generally cheaper when bought separately from car dealerships.

| Characteristics | Values |

|---|---|

| What is GAP insurance? | Insurance that covers the "gap" between what you owe and the car's worth at the time of an accident. |

| Is GAP insurance a state requirement? | No, it is not a state requirement. |

| When is GAP insurance required? | When you lease a vehicle, your lease agreement may require that you have GAP insurance in case of a total loss. |

| Where can you buy GAP insurance? | From your car insurance provider, an online insurer that specializes in GAP coverage, or from the finance team at Toyota. |

| When do you not need GAP insurance? | When the amount you owe is less than the car's value, or you can afford to pay the difference. |

| How much does GAP insurance cost? | Between $400 and $600 from car dealerships; an average of $61 a year from insurance companies. |

Explore related products

What You'll Learn

![]()

GAP insurance is not a state requirement

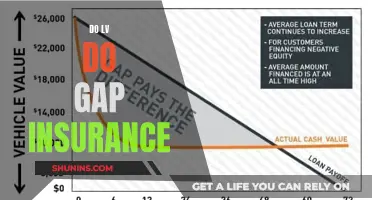

When a vehicle is declared a total loss, standard car insurance will only pay up to the current value of the car, which may be less than the outstanding loan or lease amount. GAP insurance covers the difference between the depreciated value of the car and the loan amount owed.

GAP insurance is typically only available for brand-new vehicles or models that are less than three years old. It is not required in any state, including California, and is banned from being a mandatory condition of a loan or auto sale. However, it may be required by the terms of your lease or loan agreement, especially if you have little money down or a protracted loan payoff period.

When purchasing GAP insurance, it is generally more expensive to buy it from a dealership than from a traditional insurer. It can be added to your comprehensive auto insurance policy, with some insurers charging as little as $20 a year.

Vehicle Insurance: Per Person or Car?

You may want to see also

Explore related products

![]()

GAP insurance is available from Toyota at the time of financing

Guaranteed Auto Protection, or GAP insurance, is available from Toyota at the time of financing. It is an optional insurance policy that covers the difference or "gap" between your vehicle's current market value and the balance remaining on your finance or lease contract. This comes into effect if your vehicle is deemed a "total loss" by your insurance company due to theft, accident, fire, or flood.

GAP insurance is beneficial if you owe more on your car loan than the car is worth. For example, if you owe $20,000 on a car that is totaled, but the insurance company determines the vehicle's market value is only $15,000, GAP insurance would cover the remaining $5,000 balance. This type of insurance is especially useful if you made a small down payment on the car, took out a long-term loan, or bought a car that depreciates quickly in value.

When purchasing a new car, you can buy GAP insurance from your car insurance provider, an online insurer, or the finance team at Toyota. It is important to note that GAP insurance is not a state requirement and must be sought out or specifically added to your car insurance coverage. Additionally, GAP insurance through Toyota is only available at the time of financing and cannot be added on at a later date.

Before purchasing GAP insurance, it is recommended to review your financing or leasing agreement to ensure that you do not already have GAP insurance included. It is also a good idea to contact your insurance company to see if GAP insurance is part of your regular vehicle insurance policy. By doing so, you can make an informed decision about whether you need to purchase additional GAP insurance from Toyota or another provider.

Insurance Revoked: DMV Notified?

You may want to see also

Explore related products

![]()

GAP insurance may cover your deductible

While GAP insurance typically does not cover your deductible, there are certain instances where it may. GAP insurance purchased through a car dealership may cover your primary insurance policy's deductible. However, this type of GAP insurance is usually much more expensive than buying GAP coverage from a car insurance company. If you have a $3,000 gap after your collision insurance pays out and a $500 collision deductible, GAP insurance purchased through a car insurance company will cover $2,500, leaving you to pay the remaining $500 deductible.

It is important to note that GAP insurance is not a requirement in most cases. However, if you are leasing a vehicle, your lease agreement may require you to have GAP insurance in case of a total loss. Additionally, some lenders or leasing companies may require GAP insurance to protect themselves from car owners who walk away from a loan or lease if the car is stolen or totalled.

GAP insurance is designed to cover the "gap" between what you owe on your vehicle and its worth at the time of an accident. For example, if you owe $20,000 on a car that is totalled, but your insurance company determines the vehicle's market value is only $15,000, GAP insurance would cover the remaining $5,000 balance. This type of insurance can provide valuable protection and peace of mind, especially if you have a large car loan or a vehicle that depreciates quickly in value.

When considering whether to purchase GAP insurance, it is important to review your financing or leasing agreement to see if you already have it. Additionally, contact your insurance company to understand if GAP insurance is part of your regular vehicle insurance policy. By taking these steps, you can make an informed decision about whether GAP insurance is right for you.

IDV: Vehicle Insurance's Claim Value

You may want to see also

Explore related products

![]()

GAP insurance is beneficial for lessees and drivers who still owe on their auto loans

GAP insurance is highly beneficial for lessees and drivers who are yet to pay off their auto loans. This is because it covers the difference between the depreciated value of the car and the loan amount owed if the car is involved in an accident.

If you lease a vehicle, your lease agreement may require you to have GAP insurance in case of a total loss. GAP insurance is not a state requirement, unlike liability insurance. However, it is beneficial for those who have taken out large auto loans, made small down payments, or have long loan terms.

For instance, if you took out a $30,000 auto loan for your new Toyota vehicle and it is worth $27,000 at the time of the accident, your auto insurance company would pay you $27,000. The GAP insurance would then cover the remaining $3,000, ensuring you don't have to.

GAP insurance is particularly useful if you have a long loan payoff period, a small down payment, or a vehicle that depreciates quickly. It can protect you from financial losses by minimising the gap between the depreciated value of your car and the loan amount you owe.

You can purchase GAP insurance from your car insurance provider, an online insurer specialising in GAP coverage, or the finance team at car dealerships like Beechmont Toyota. It is recommended to review your loan balance frequently and cancel the GAP insurance once you owe less than the book value of your vehicle.

Switching Auto Insurance: A Quick Guide

You may want to see also

Explore related products

![[2025 Upgrade] Windshield Sun Shade Umbrella, Scratch-Free Car Sunshade for SUVs, Foldable Automotive Interior Sun Protection | Highly UV Block Coating Auto Heat Shield Accessories(XX-Large)](https://m.media-amazon.com/images/I/61HCk9khFDL._AC_UL320_.jpg)

![]()

You can purchase GAP insurance from your car insurance provider

Guaranteed Asset Protection (GAP) insurance is an optional product that covers the difference between the amount you owe on your auto loan and the amount your insurance company pays out if your car is stolen or totaled. This is particularly useful if your loan balance is higher than the value of your vehicle.

When you purchase or lease a car, the dealer will likely offer you GAP insurance as one of several optional add-ons. However, you can also purchase GAP insurance from your car insurance provider, an online insurer that specializes in GAP coverage, or from the finance team at Toyota.

Before purchasing GAP insurance, it is important to consider the following:

- Contact your insurance company to see if GAP insurance is already included in your regular vehicle insurance policy.

- Review your financing or leasing agreement to see if you already have GAP insurance.

- Compare prices and coverage from different providers before purchasing.

- Be aware that GAP insurance typically requires you to also have collision and comprehensive coverage.

By purchasing GAP insurance from your car insurance provider, you can ensure that you have the necessary coverage in case your vehicle is stolen or totaled. This will protect you from having to pay thousands of dollars for a car you no longer have.

In summary, while GAP insurance is not a state requirement, it is a valuable addition to your car insurance coverage, especially if you have a small down payment, a long-term loan, or a vehicle that depreciates quickly.

Transfer Vehicle Insurance: A Quick Guide

You may want to see also

Frequently asked questions

Guaranteed Auto Protection (GAP) insurance covers the difference between the amount you owe on your vehicle and its market value at the time of an accident.

No, GAP insurance is not a state requirement. However, if you lease a vehicle, your lease agreement may require you to have GAP insurance.

You can purchase GAP insurance from your car insurance provider, an online insurer, or from the finance team at Toyota.

GAP insurance costs an average of $61 per year, but prices can vary depending on the provider. Car dealerships typically charge between $400 and $700 for GAP insurance.