When it comes to healthcare coverage in the United States, individuals have a choice between Medicare and private insurance. Medicare is a government-provided health insurance program, while private insurance is offered by employers or purchased individually. Both options have their own advantages and disadvantages, and the preference of Americans may vary depending on their specific needs and circumstances. This paragraph will explore the factors that Americans consider when deciding between Medicare and private insurance to determine which option they prefer.

| Characteristics | Values |

|---|---|

| Medicare costs | The standard premium for Medicare Part B was $164.90 in 2023. Medicare Advantage plans have a $0 premium. The average cost of a Medicare Advantage plan with drug coverage is $28 per month. Original Medicare with a separate Part D and Medigap plan G policy costs a combined average of $224 per month. |

| Private insurance costs | Private health insurance costs an average of $1,458 per month for a 65-year-old on a Silver plan. |

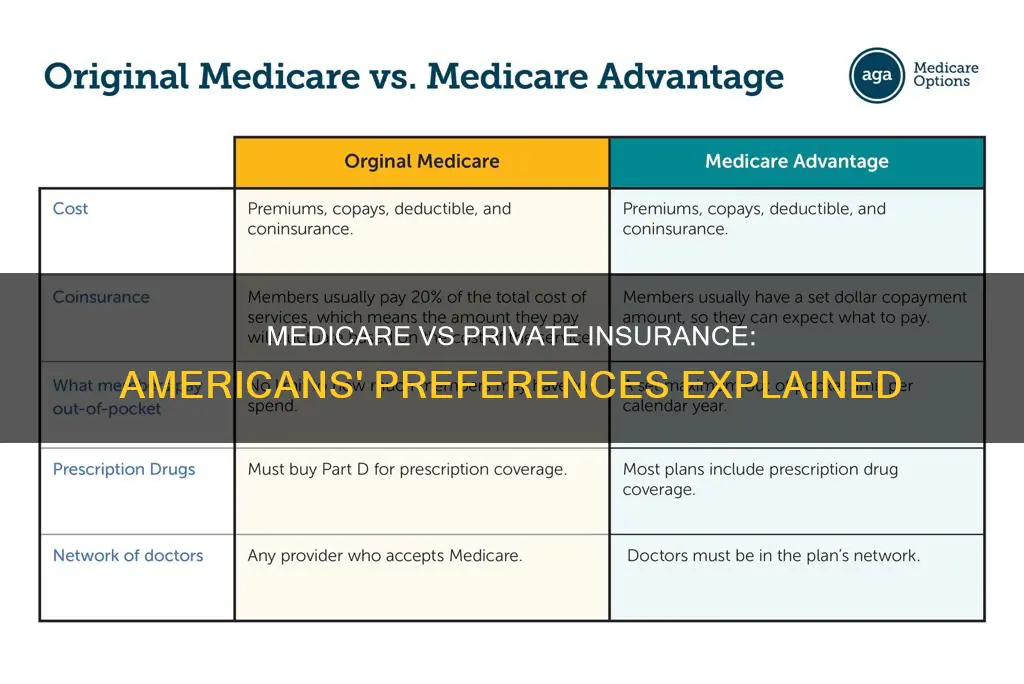

| Medicare coverage | Medicare offers high-quality coverage. Original Medicare (Parts A and B) does not have an out-of-pocket maximum, so medical costs can add up quickly. Medicare Advantage plans can help people with chronic conditions save money on healthcare costs. Medicare Supplement Insurance (Medigap) helps pay your share of costs in Original Medicare, but it generally does not cover long-term care, vision, dental, hearing aids, private-duty nursing, or prescription drugs. |

| Private insurance coverage | Private insurance plans may offer more coverage than Medicare. Private insurance may be a better option if you need to cover a spouse or child. |

| Enrollment | You become eligible for Medicare around your 65th birthday and have an 8-month initial enrollment window. You can keep your private insurance plan even if you enroll in Medicare, but you may incur additional costs and face late enrollment penalties for Medicare in the future. |

| Plan options | Medicare offers Original Medicare and Medicare Advantage plans. Private insurance plans are typically offered through an employer, with a limited number of options, or through the Affordable Care Act (ACA), which allows shopping for plans based on premiums, out-of-pocket costs, and coverage differences. |

Explore related products

$14.99

What You'll Learn

![]()

Medicare vs. private insurance costs

Medicare is a federal insurance programme, while private insurance is administered by private companies. The federal government provides Original Medicare, while private companies administer Medicare Advantage plans on behalf of the government. Medicare is available to individuals aged 65 and older or those with qualifying disabilities, while private insurance allows for dependent coverage.

Medicare is divided into parts, with Part A and Part B provided by the government and known as Original Medicare. Part C, Part D, and Medigap are provided by private health insurance companies. Medicare Part A is premium-free for most people, while the standard premium for Medicare Part B was $164.90 in 2023. Medicare Advantage plans can have a <$0 premium and may offer extra coverage at little to no cost. Medicare Part C plans must cap in-network spending at $9,350 in 2025, excluding prescriptions.

Private insurance premiums vary by location, age, and chosen type of coverage. High deductible plans tend to cost less per month than low deductible plans. Private insurance plans must limit out-of-pocket spending to $9,200 for an individual and $18,400 for a family in 2025.

Medigap, offered by private companies, fills the gaps in Original Medicare coverage. Individuals must be signed up for Medicare Part A and B to purchase a Medigap policy and will pay a monthly Part B premium and a Medigap premium.

While it is challenging to make a direct cost comparison between Medicare and private insurance, private insurance payment rates tend to be higher than Medicare rates for hospital and physician services. According to a 2022 Rand Corporation report, private insurance payment rates were 224% higher than Medicare rates for services.

Get Instant Medical Insurance for Your Infant

You may want to see also

Explore related products

![]()

Medicare and private insurance coverage

When deciding between Medicare and private insurance, it is important to consider the costs and coverage offered by both options. Original Medicare (Parts A and B) does not have an out-of-pocket maximum, which means that medical costs can add up quickly. However, Medicare offers high-quality coverage at affordable prices, and certain Medicare plans, such as Special Needs Plans, help people with chronic conditions save money on healthcare costs. Medicare Supplement Insurance (Medigap) is extra insurance that can be purchased to help cover the costs of Original Medicare, although it typically does not cover long-term care, vision, dental, hearing aids, or prescription drugs.

Private insurance, on the other hand, is often obtained through an employer, which means that the options are limited to those provided by the company. Private insurance may be preferable if you need to cover a spouse or child, or if you plan to work past the age of 65. It is also important to note that private insurance typically costs more than Medicare, and you may not be able to receive discounts or subsidies if you are eligible for Medicare.

It is possible to have both Medicare and private insurance at the same time, but this may result in duplicate coverage and additional costs, such as paying two separate premiums. In the case of ACA plans, Medicare will be the primary payer, and the private insurance will be the secondary payer, responsible for any remaining balance.

Overall, Medicare is often considered the better option due to its affordability and quality coverage, but private insurance may be preferable in certain situations, such as when needing to cover a spouse or child.

Blue Cross Medical Insurance: Dental Implant Coverage Explained

You may want to see also

Explore related products

![]()

Medicare and private insurance for families

When it comes to Medicare and private insurance for families, there are several factors to consider. Firstly, it's important to understand the differences between the two types of insurance. Medicare is a public health insurance program provided by the government, while private insurance is offered by private companies, often through an employer's group plan.

One key consideration for families is the eligibility for Medicare. Individuals become eligible for Medicare around their 65th birthday, and there is an 8-month initial enrollment window. However, if an individual is still working and has coverage through their employer or their spouse's employer, they can usually keep that private insurance coverage without penalty if they later enroll in Medicare during a special enrollment period. This flexibility allows families to weigh their options and make choices based on their specific circumstances.

Another factor to consider is the coverage provided by each type of insurance. Original Medicare (Parts A and B) does not have an out-of-pocket maximum, which means medical costs can add up quickly. On the other hand, private insurance plans may offer more comprehensive coverage, including additional benefits such as vision, hearing, and dental services, which are not typically covered by Original Medicare. Medicare Supplement Insurance (Medigap) is an option to purchase from a private company to help cover costs in Original Medicare, but it may not cover long-term care, prescription drugs, or certain other services.

It is possible to have both Medicare and private insurance at the same time, and this combination can provide more comprehensive coverage for families. In this case, a process called "coordination of benefits" determines which insurance provider pays first, with the secondary payer covering any remaining costs not covered by the primary payer. However, it's important to note that the order of payment depends on the specific circumstances, such as the size of the employer and the type of private insurance plan.

When deciding between Medicare and private insurance, or considering a combination of both, it's essential for families to evaluate their healthcare needs, income, and other factors to determine which option provides the most suitable coverage for their situation. Consulting with a Medicare expert or utilizing resources like the State Health Insurance Assistance Program (SHIP) can help individuals and families make informed decisions about their healthcare coverage.

Get Medical Insurance in Madison, Wisconsin: A Guide

You may want to see also

Explore related products

![Medicare and Social Security: [5 in 1] Maximize Your Retirement Benefits, Secure Medical Coverage and Quality Healthcare | Proven Strategies to Protect Your Financial Future Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/71sRJGiWeQL._AC_UL320_.jpg)

![]()

Medicare and private insurance for over 65s

Medicare is the federal health insurance program for people aged 65 and over in the United States. Most people qualify for premium-free Medicare Part A if they or their spouse have worked for at least 10 years. Part A covers inpatient hospital stays, skilled nursing facilities, hospice care, and some home health services. However, it's important to note that there may still be out-of-pocket costs like deductibles and coinsurance. Additionally, if an individual has not worked for at least 10 years, Part A can cost up to $500 per month.

Medicare Part B is medical insurance that covers outpatient care, doctor visits, lab tests, and preventive care. Everyone pays for Part B, which had a monthly premium of $170.10 in 2022. It's important to note that Part B only covers 80% of costs, so individuals may need to purchase additional insurance to cover the remaining 20%.

Medicare Part C, also known as Medicare Advantage, is offered by private insurance companies and bundles hospital and medical insurance with prescription drug coverage. Some plans may also include dental and vision benefits, but they usually limit provider choices.

While Medicare is a popular option for Americans over 65, some individuals choose to stick with private insurance or explore other options like Direct Primary Care (DPC). Private insurance often has higher premiums than original Medicare, but it may offer lower copayments and a more predictable deductible structure. Additionally, private insurance often provides a broader provider network and more customizable benefits.

For those who qualify for both Medicare and private insurance, it is possible to have dual coverage. However, the percentage of adults aged 65 and older with dual coverage decreased from 47.9% in 2017 to 39.6% in 2022, indicating an increased reliance on Medicare coverage alone.

Blue Cross Insurance: Medical, Vision, and Dental Costs Explored

You may want to see also

Explore related products

![]()

Switching between Medicare and private insurance

Medicare is a federal insurance programme, while private insurance is administered by private companies. Medicare is primarily for individual Americans aged 65 and older, whereas private insurance can cover dependents and family members. Medicare offers more coverage combinations and varying levels of coverage, while private insurance plans have a limited number of offices, hospitals, and healthcare providers in their network.

Private insurance companies also offer certain types of Medicare plans, including Medicare Advantage (Part C), Medigap, and Part D (prescription drug) plans. Medicare Advantage combines the coverage of Part A and Part B into a single plan and often includes prescription drug coverage. It may also cover services that Original Medicare does not, such as dental, vision, and hearing care. Medigap is an insurance policy that fills the gaps in Original Medicare coverage and helps pay for some of the costs that Medicare does not cover.

It is possible to have both private insurance and Medicare at the same time. When you have both, a process called "coordination of benefits" determines which insurance provider pays first. This provider is called the primary payer, and they pay for any covered services until the coverage limit is reached. The secondary payer then covers any costs that the primary payer does not, although they may not cover all remaining costs.

If you have an employer-provided plan, COBRA, or TRICARE, you can have both Medicare and private insurance. However, it is important to be aware of the costs of having two active plans, such as paying separate premiums. Additionally, you will need to determine which plan will be billed first for services, as Medicare and ACA plans do not coordinate benefits. Keeping your ACA plan may also result in late enrollment penalties for Medicare.

Davis Vision Insurance: Application Process Simplified

You may want to see also

Frequently asked questions

Medicare is typically better than private insurance because it offers affordable, high-quality coverage. Private insurance, on the other hand, tends to be more expensive and may not offer the same level of coverage. However, private insurance may be useful if you need to cover a spouse or child, or if you plan to work past the age of 65.

Yes, you can have both Medicare and private health insurance at the same time. However, you may need to pay two separate premiums and determine which plan will be billed first for services.

The choice between Medicare and private insurance depends on various factors, including your healthcare needs, income, travel frequency, and whether you need to cover a spouse or family. It's important to review the costs and coverage options for both Medicare and private insurance plans before making a decision.