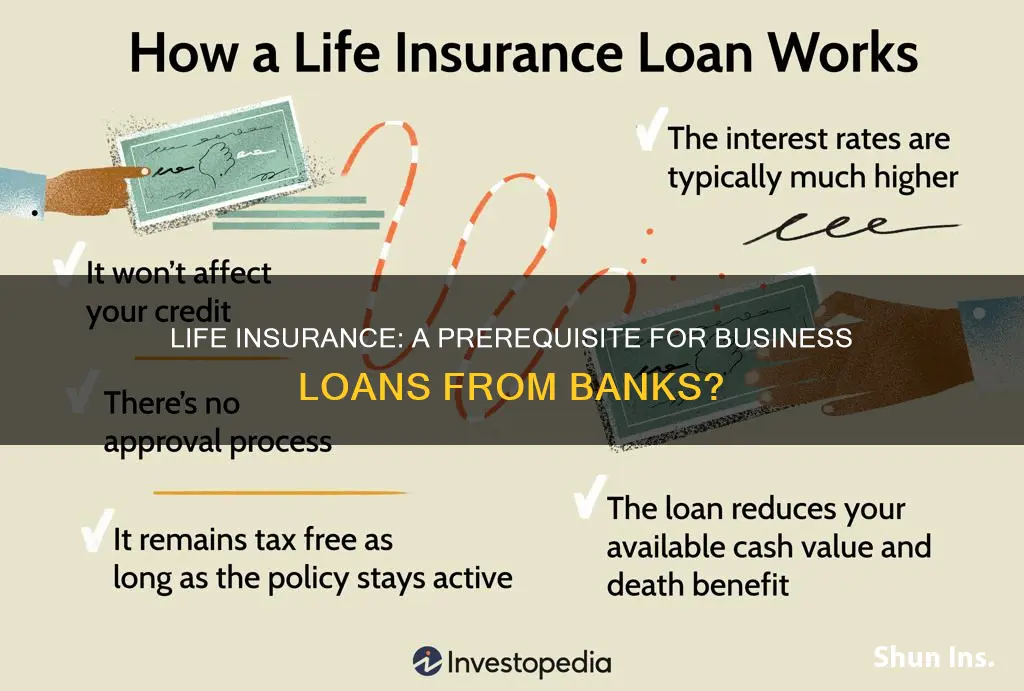

Life insurance is often used as a form of collateral for business loans. This is because banks require insurance for collateral assignment, which ensures they can recover any outstanding loan amount in the event of the borrower's death or default. The insurance policy acts as a safety net for the lender and can increase the likelihood of loan approval. The borrower remains the insured individual and is responsible for paying the premiums. However, the lending institution or bank is listed as the primary beneficiary until the loan is fully repaid. This process is known as a collateral assignment, and it allows the bank to claim the death benefits from the policy, but only for the remaining balance of the unpaid loan.

| Characteristics | Values |

|---|---|

| Do banks require life insurance for business loans? | Yes |

| Why do banks require life insurance for business loans? | To ensure the loan is repaid in the event of the borrower's death |

| What type of life insurance is required for a business loan? | Term life insurance or whole life insurance |

| Who is the beneficiary of the life insurance policy? | The bank is the primary beneficiary until the loan is repaid; after that, the beneficiary is the policyholder's choice |

| What is the process of assigning life insurance as collateral for a business loan? | The policyholder fills out a collateral assignment form, which is then executed by the bank and the insurance company |

| Are there any alternatives to using life insurance as collateral for a business loan? | Yes, other forms of collateral include real estate, financial securities, or a cash account |

Explore related products

What You'll Learn

![]()

Banks require insurance for collateral assignment

A collateral assignment of insurance is a conditional agreement that appoints the lender as the primary beneficiary of the policy's benefits, which serves as collateral for the loan. If the borrower cannot pay, the lender can cash in the insurance policy and reclaim the amount owed. The borrower must be the owner of the policy and keep it current for the duration of the loan, but they do not have to be the insured person.

The collateral assignment process works like a standard loan, with the insurance policy serving as "collateral." The entity that pays out the loan becomes the temporary beneficiary of the policy's death benefit until the loan is repaid. This arrangement is conditional, meaning the entity cannot make changes to the policy, resell it, or access its cash value. Instead, they can only draw on the death benefit if the policyholder defaults.

Collateral assignment offers several advantages, including safeguarding the lender's interests, providing flexibility with capital assets, and serving as low-cost collateral. However, it also has limitations, such as reduced death benefits, difficulty obtaining affordable insurance with low premiums, and limited use of the policy's cash value.

When applying for a collateral assignment of life insurance, individuals can go through their bank or insurer. The process involves securing the loan, filling out the necessary forms, and submitting them for processing. The forms must be completed by all parties, including the borrower, lender, and insurance company, and may require notarization.

Life Insurance: Personal Property Protection or Separate Policy?

You may want to see also

Explore related products

![Loans on Life Insurance Policies, by John M. Taylor, President the Connecticut Mutual Life Insurance Company 1913 [Leather Bound]](https://m.media-amazon.com/images/I/617DLHXyzlL._AC_UY218_.jpg)

![]()

The bank is not the beneficiary, but the assignee

When it comes to business loans, banks often require life insurance as a form of collateral to protect their investment. This is especially true for new and unproven businesses, as banks are hesitant to take on risks without some form of security. By having a life insurance policy in place, business owners can increase their chances of obtaining a loan and provide peace of mind to the bank that they will not default on their payments.

In the event of the borrower's untimely death, the bank will be able to recover the outstanding loan amount from the insurance payout. However, it is important to understand the difference between the bank being the beneficiary and the assignee of the life insurance policy.

The bank is not the beneficiary but the assignee in the case of a collateral assignment. This means that the bank is not directly entitled to the death benefit of the policy. Instead, they are assigned a payout only if the borrower passes away before the loan is fully repaid. The collateral assignment ensures that the bank has recourse to the policy's benefits if the borrower defaults on their loan obligations.

For example, let's say a borrower takes out a $500,000 loan from the bank to fund their business. The bank may require them to purchase a term life insurance policy with a payout of at least $500,000. If the borrower passes away before repaying the loan in full, the insurance payout will be used to cover the remaining balance, and the rest will go to their chosen beneficiary.

The collateral assignment gives the bank the right to claim the death benefits from the policy, but only up to the amount of the unpaid loan balance. The borrower still has the flexibility to choose a loved one as the primary beneficiary of the policy. By assigning the policy as collateral, the borrower provides an added layer of security for the bank, increasing their chances of obtaining the necessary funding for their business ventures.

Overall, the use of life insurance as collateral for business loans provides benefits to both the borrower and the bank. It gives the bank peace of mind and protects their investment, while also helping the borrower obtain the necessary funding to start or grow their business.

Life Insurance with Sleep Apnea: Is It Possible?

You may want to see also

Explore related products

![]()

Absolute vs. conditional assignment

Banks often require life insurance as collateral for business loans. This provides them with a guarantee that they will be able to recover their funds if the borrower defaults or dies.

Now, let's delve into the differences between absolute and conditional assignment in the context of life insurance and business loans:

The type of assignment—absolute or conditional—depends on whether the life insurance policy already exists or is being taken out specifically to collateralize the loan.

Absolute Assignment

- In an absolute assignment, the policyholder transfers full ownership rights of the life insurance policy to another party, known as the assignee.

- The original owner of the policy, or the assignor, signs over the entire policy, and the assignee takes on full ownership.

- The assignee becomes liable for any premiums and gains the authority to change or designate new beneficiaries.

- Absolute assignment is typically used when the policy is taken out specifically to collateralize the loan.

Conditional Assignment

- Conditional assignment, on the other hand, is a temporary arrangement where the policy is used as collateral for a loan.

- The lender becomes the temporary beneficiary of the policy's death benefit until the loan is repaid.

- The assignee, in this case, does not have the authority to make changes to the policy, resell it, or access its cash value.

- Once the loan is repaid, the policy is no longer used as collateral, and full ownership returns to the original policyholder.

- Conditional assignment is typically used when the policyholder already has a life insurance policy in place and uses it as collateral for the loan.

In summary, the key difference between absolute and conditional assignment lies in the level of ownership transferred to the assignee. Absolute assignment involves transferring full ownership of the policy, while conditional assignment is a temporary arrangement where the assignee has limited rights to the policy as collateral for the loan.

Life Insurance and Breast Cancer: What Coverage is Offered?

You may want to see also

Explore related products

![]()

Pros and cons of collateral assignments

Banks often require insurance for collateral assignment to protect their investment and ensure they can recover any outstanding loan amount in the event of the loaner defaulting or dying before repaying the loan. A collateral assignment of insurance is a conditional assignment that appoints the lender as the primary beneficiary of a benefit used as collateral for a loan.

Pros:

- Improved loan eligibility: Collateral assignment can increase the chances of qualifying for a loan, especially if there are other issues, such as a low credit score or small down payment.

- Lower interest rates: Putting up collateral reduces the financial risk for the lender, who may offer a lower interest rate as a result.

- Protection of other assets: Using life insurance as collateral may be preferable to risking the loss of assets such as a home or car.

- Affordability and flexibility: Term life insurance, in particular, is affordable and flexible, giving the bank assurance without straining the borrower's budget.

- No need for additional insurance: Using an existing life insurance policy as collateral can eliminate the need for purchasing additional insurance.

- Access to capital: Collateral assignment allows borrowers to access capital that may otherwise be difficult to obtain.

- Limited death benefits: Assigning only a portion of the death benefits as collateral ensures that the lender does not claim all the death benefits upon the borrower's death.

Cons:

- Reduced death benefits: The primary beneficiary of the life insurance policy will receive a reduced payout if the borrower dies before repaying the loan, as the lender has the first claim on the death benefit.

- Loss of policy control: The borrower loses control over their life insurance policy, as the lender becomes the temporary beneficiary.

- Limited use of cash value: The borrower's ability to access the cash value of their life insurance policy may be restricted until the loan is repaid.

- Additional insurance cost: The borrower must pay premiums for the life insurance policy used as collateral, resulting in an extra cost on top of loan payments.

- Potential qualification issues: There is no guarantee of qualifying for life insurance, especially if the borrower has health issues, which could increase insurance costs or make collateral assignment unfeasible.

- Beneficiary concerns: Using life insurance as collateral may result in insufficient coverage for beneficiaries, such as a spouse or children, if the death benefit is reduced.

Term Life Insurance: Key Traits Explained

You may want to see also

Explore related products

![]()

How to apply for life insurance for collateral assignment

Banks often require life insurance for business loans as a form of protection. This is called a collateral assignment, where the bank is the temporary beneficiary of the policy's death benefit until the loan is repaid.

- Determine the type of life insurance: You can use either term or whole life insurance as collateral. Term life insurance is suitable if the term length meets or exceeds the loan repayment period. Whole life insurance, with its cash value and guaranteed death benefit, is often preferred by lenders.

- Find a lender: Research and choose a lender that accepts life insurance as collateral for business loans.

- Get a life insurance quote: Contact a licensed insurance agent or broker and inform them that you intend to use the policy as collateral for a loan. They will guide you through the process and help you get a quote for the required coverage.

- Apply for life insurance: Complete the necessary application process, which may include a medical exam. Ensure the policy allows for collateral assignments and meets the lender's requirements.

- Secure the loan: Work with your chosen lender to secure the loan. They will inform you of their specific requirements and limitations regarding the collateral assignment of life insurance.

- Fill out the collateral assignment form: Obtain the collateral assignment form from your insurer and fill it out. This form must be completed by all parties involved, including yourself, the lender, and the insurance company. Sign the form, and some banks may require notarization.

- Submit the form: Submit the completed collateral assignment form to your insurer for processing.

- Provide proof of policy to the lender: After your life insurance policy is approved and the collateral assignment is accepted, provide proof of the policy to your lender.

- Continue premium payments: It is crucial to stay current on your life insurance premium payments throughout the loan period. Failure to do so could have serious repercussions as per the loan agreement.

- Loan repayment and release of assignment: Once the loan is fully repaid, the lender will send a release form to the insurance company, ending the collateral assignment.

By following these steps, you can apply for life insurance and use it as collateral to secure a business loan. Remember to carefully review the terms and conditions of the loan and collateral assignment, and seek guidance from financial professionals if needed.

Life Insurance and Government: Understanding Liens and Their Impact

You may want to see also

Frequently asked questions

Yes, banks sometimes require life insurance for business loans. This is to ensure their investment is protected in case the loan recipient dies before the loan is repaid.

Both permanent and term life insurance policies can be used as collateral for a business loan. Term life insurance is often preferred as it is much cheaper.

The bank will be listed as the primary beneficiary of the life insurance policy while the loan is still due. This means that if the loan recipient dies before the loan is repaid, the bank will receive the payout amount to cover the remaining loan balance.