Car insurance rates are influenced by a multitude of factors, including age, gender, driving history, location, vehicle type, and credit score. While insurance rates generally decrease as individuals gain more driving experience, they can begin to creep back up once drivers reach their senior years, typically around 65 to 75 years old. This increase is attributed to a higher risk of accidents due to physical, cognitive, or visual impairments, despite seniors spending less time on the road. However, it is important to note that insurance rates are highly personalized, and various other factors can contribute to fluctuations in insurance premiums.

| Characteristics | Values |

|---|---|

| Insurance rates for 60-year-olds | Insurance rates are typically the lowest for middle-aged drivers. However, car insurance costs for seniors may increase due to their being more prone to car accidents because of physical, cognitive, or visual impairments. |

| Factors affecting insurance rates | Number of years licensed, driving history, age, gender, education, marital status, zip code, mileage, credit score, claims history, vehicle type, and driving record. |

| Ways to lower insurance rates | Maintaining a clean driving record, bundling policies, setting up autopay, paying premiums in full, going paperless, and affiliation with professional organizations. |

Explore related products

What You'll Learn

![]()

Car insurance is most expensive for teenagers

While insurance rates can increase for drivers as they age, car insurance is typically most expensive for teenagers and young adults. This is due to a variety of factors, including inexperience, a lack of driving history, and a higher likelihood of accidents.

Inexperience and lack of driving history are major factors in determining insurance rates for teenagers. Teenagers are considered riskier clients for insurance companies due to their lack of experience behind the wheel. They are more prone to accidents and traffic violations, such as failing to check blind spots or speeding, which can result in higher insurance claims. Additionally, teenagers may engage in riskier behaviours, such as street racing or driving under the influence, further increasing the potential cost of claims.

Another factor contributing to higher insurance rates for teenagers is their propensity for distractions while driving. Technology-related distractions, such as texting, can increase the risks and make insurance more expensive. Credit scores can also play a role, as teenagers may not have an extensive credit history, leading insurers to use other factors to determine their risk level and set higher premiums.

The cost of insuring a teenager can be mitigated by adding them to an existing family insurance policy, which is typically more affordable than a separate policy. Some insurance companies offer discounts for teenagers, such as good student discounts or safety course completion discounts. Shopping around for the best rates and taking advantage of discounts can help reduce the financial burden of insuring teenage drivers.

While car insurance for teenagers tends to be expensive, it is important to encourage safe driving habits and responsible behaviour to keep insurance-related costs down. This includes educating teenagers about the impact of their driving record, grades, and overall driving responsibility on insurance rates. By understanding the factors that influence insurance costs, teenagers and their families can make informed choices to find the most affordable coverage options.

Nurses: Malpractice Insurance—Why It's Necessary

You may want to see also

Explore related products

![]()

Rates decrease for middle-aged drivers

While insurance rates can vary based on several factors, age is one of the most significant determinants of car insurance rates. Teenagers and young adults are considered inexperienced and hence more prone to accidents and risky behaviour, making them a cause of concern for insurance companies. As a result, insurance rates for this demographic are relatively high.

However, as drivers gain more experience behind the wheel, their risk profile decreases, and insurance rates tend to follow suit. Middle-aged drivers, typically those in their 30s and 40s, are considered the safest category of drivers due to their extensive driving experience. As a result, insurance rates for this age group are significantly lower than for younger drivers.

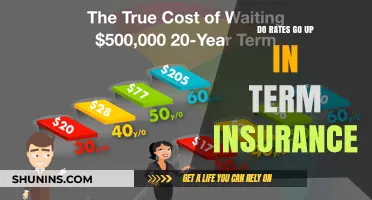

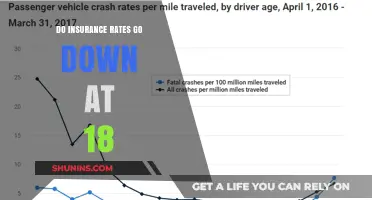

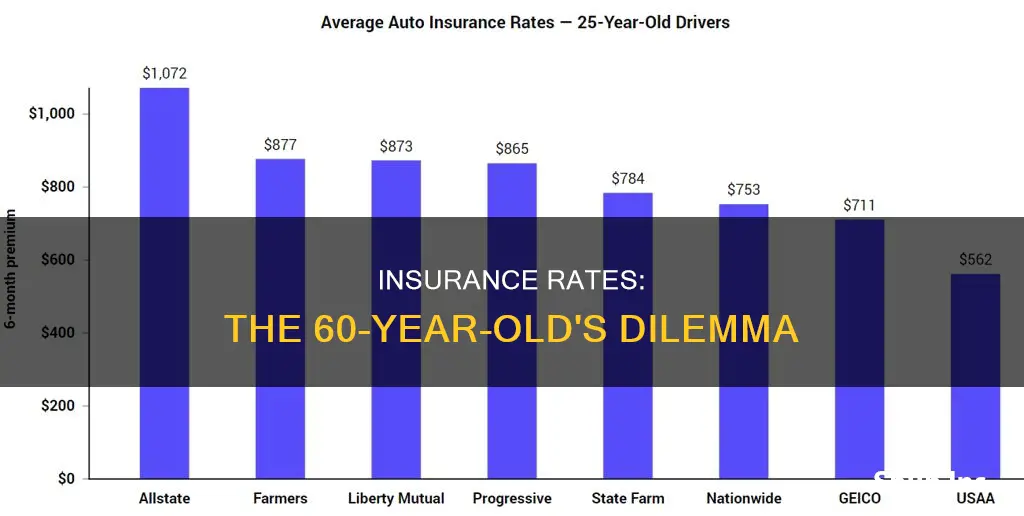

For instance, at Progressive, the average premium per driver decreases substantially from ages 19 to 34 and then stabilizes or decreases slightly from 34 to 75. Similarly, a 60-year-old driver will pay around $158 per month for full coverage, which is considerably less than what a teenager or young adult would pay.

Other factors that can influence insurance rates include gender, driving history, credit history, ZIP code, and the types of coverage purchased. Additionally, it is important to note that insurance rates can vary across different states and insurance providers. While age is a crucial factor, it is not the sole determinant of insurance rates, and other factors can also significantly impact the cost of insurance.

Next Insurance: Admitted Carrier Status

You may want to see also

Explore related products

![]()

Premiums increase for older drivers

While age is one of the most important factors in determining car insurance rates, there are several other factors that influence the cost of insurance premiums. These include gender, driving experience, location, vehicle type, credit score, and driving history.

Young and inexperienced drivers are considered high-risk by insurance companies due to their increased likelihood of exhibiting unsafe driving behaviours and getting into accidents. As a result, teenagers, especially those between 16 and 17 years old, face the highest average insurance costs. Insurance rates typically decrease significantly from ages 19 to 34 as drivers gain more experience and sharpen their driving skills.

Drivers in their 30s, 40s, and 50s often enjoy the lowest insurance rates of their lives. This is because they are considered experienced and are less likely to cause accidents or file insurance claims. However, if these drivers have teenage children or elderly parents living with them, their insurance rates may increase.

As drivers enter their senior years, insurance rates can start to creep back up. While seniors may have a great driving record, they are generally considered more prone to car accidents due to physical, cognitive, or visual impairments. Additionally, repair costs, inflation, and more frequent claims from extreme weather events have contributed to rising insurance rates across the board.

It is worth noting that insurance rates are not solely based on age and can vary depending on individual circumstances and the insurance provider's criteria. Factors such as a clean driving record, higher education levels, and marital status can contribute to lower insurance premiums, while accidents, violations, and claims can lead to higher costs. Therefore, it is recommended to shop around for insurance providers and compare rates regularly to ensure the best deal.

Bodily Injury Insurance: Florida's Law

You may want to see also

Explore related products

![]()

Factors affecting insurance rates

Insurance rates are affected by a multitude of factors, with age being one of the most significant. Generally, insurance rates are lowest for middle-aged drivers, with rates tending to decrease significantly from ages 19 to 34. Drivers in their 30s, 40s, and 50s typically enjoy the lowest insurance rates in their lifetime. This is because they have more experience on the road and are less likely to cause accidents, making them a lower risk to insure.

However, insurance rates can start to increase again for older drivers, typically around 65 to 75 years old. This is because older drivers may be more prone to car accidents due to physical, cognitive, or visual impairments. Despite their years of experience, older drivers may face higher insurance rates due to these factors.

Another critical factor in determining insurance rates is driving history and experience. A clean driving record, free of accidents, violations, and claims, can lead to lower insurance premiums. Conversely, accidents, speeding tickets, and DUIs can cause insurance rates to increase. The number of years licensed is also a factor, with inexperienced drivers often facing higher rates, regardless of age.

Location is another factor that influences insurance rates. Insurance rates vary by state and even by ZIP code. Living in a densely populated area with high traffic congestion can result in higher insurance rates compared to residing in a rural town with less traffic. Additionally, factors such as education, marital status, and vehicle type can also impact insurance rates.

Other factors that can affect insurance rates include mileage, vehicle usage, and credit score. Individuals who drive more miles or use their vehicles for business purposes may face higher rates. On the other hand, those who work from home or are retired and drive less may be eligible for discounts or usage-based insurance plans. Credit scores can also impact insurance rates, although this varies by state, with some states prohibiting its use as a rating factor.

Public Schools and Insurance: Who Pays?

You may want to see also

Explore related products

![]()

How to get cheaper insurance

While insurance rates are typically the lowest for middle-aged drivers, they can increase for older drivers, even those with a great driving record. This is because older drivers are statistically more prone to car accidents due to physical, cognitive, or visual impairments. However, seniors often spend less time on the road, which could translate to savings through programs like Progressive's Snapshot program.

- Shop around: Compare prices from different insurance companies, including smaller insurers, which may offer better customer service and cheaper rates than national companies. Get at least three price quotes by calling companies directly or accessing information online. Your state insurance department may also provide comparisons of prices charged by major insurers.

- Improve your credit score: Establishing a solid credit history can cut your insurance costs. Most insurance companies use credit information to price auto insurance policies, and most companies will allow you to rerate once a year.

- Combine insurance policies: Insure your home and auto at the same place, and consider buying two or more types of insurance from the same company. You may also get a reduction if you have more than one vehicle insured with the same company.

- Take advantage of discounts: Ask about discounts for having a good credit record, low annual mileage, being a long-time customer, having multiple cars, and having no accidents or moving violations in the past three years. You may also get a discount if you take a defensive driving course or have a young driver on the policy who is a good student or has taken a driver's education course.

- Be a good driver: Avoid tickets and accidents, as these can increase your insurance rates.

- Drop comprehensive or collision coverage: If your car is older and worth less than 10 times the premium, purchasing this type of coverage may not be cost-effective.

- Reduce claims: Save up enough money to replace your own car so that you don't have to rely on insurance payouts, which can keep your premium low.

- Prove low mileage: Some insurance companies offer reductions for low annual mileage.

- Move to a cheaper neighborhood: Your location can impact your insurance rates, so consider moving to a neighborhood with cheaper premiums.

Silver&Fit Insurance Coverage Options

You may want to see also

Frequently asked questions

While insurance rates are typically lowest for middle-aged drivers, they may increase for seniors. This is because older drivers are more prone to car accidents due to physical, cognitive, or visual impairments. However, seniors generally spend less time on the road, which could result in savings.

Insurance rates are influenced by factors such as driving experience, accident history, gender, credit score, education level, marital status, location, vehicle type, and mileage.

You can get discounts on your insurance rates by maintaining a clean driving record, having a higher education degree, bundling policies, setting up automatic payments, paying premiums in full, or using a usage-based insurance program.