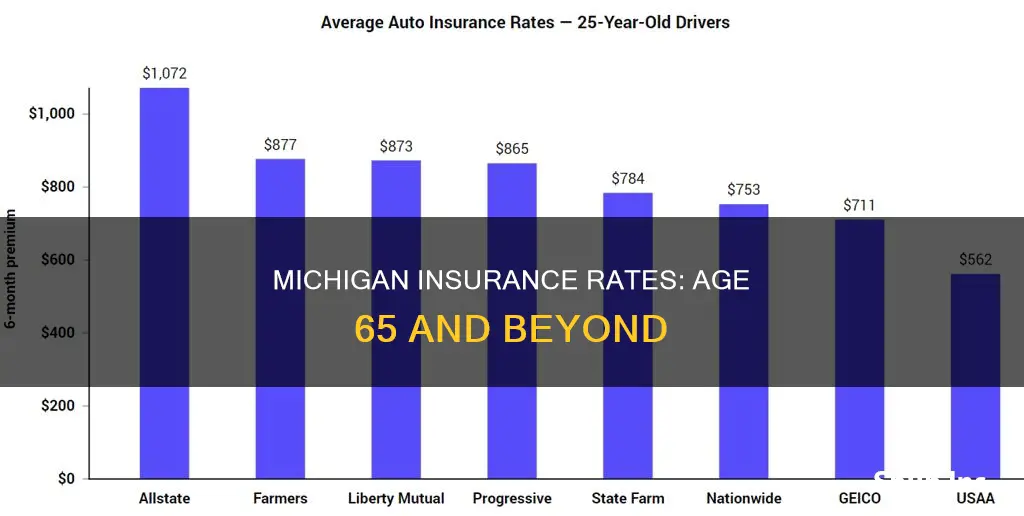

Michigan has some of the highest insurance rates in the US, with an average annual cost of $2,583. Insurance companies assign a risk profile to drivers based on their age, with younger drivers considered riskier than middle-aged ones. While rates decrease until the driver is 62, they tend to increase for those over 65. This is due to a variety of factors, including slower reaction times and poorer vision. Additionally, drivers over 70 may struggle to find an insurer as they are considered high-risk.

| Characteristics | Values |

|---|---|

| Insurance rates for seniors over 65 | Typically begin to rise |

| Average increase in insurance rates from age 60 to 65 | $44 per year |

| Average insurance rates for a 50-year-old in Michigan | $2,730 per year |

| Average insurance rates for a 16-year-old in Michigan | $9,693 per year |

| Average insurance rates for Michigan residents | $1,596 per year for state-mandated minimum coverage; $3,156 per year for full coverage |

| Average insurance rates for Detroit residents | $5,667 per year |

| Average insurance rates for Hamtramck residents | Not mentioned, but Hamtramck is listed as a city with high crime rates and traffic congestion, which contribute to higher premiums |

| Factors that affect insurance rates | Age, driving record, vehicle type, location, and demographic factors |

Explore related products

What You'll Learn

![]()

Michigan's no-fault insurance laws

In the context of Michigan's insurance rates, which are some of the highest in the nation, it is important to understand the role of the state's no-fault insurance laws. Michigan's no-fault insurance system is a unique aspect of its insurance laws, and it significantly contributes to the high insurance prices in the state.

The no-fault insurance system in Michigan means that insurance companies are required to cover the costs of accidents, regardless of who is at fault. This system aims to reduce the number of lawsuits filed after accidents, but it also leads to higher insurance premiums for drivers. The insurance companies pass on the cost of covering accidents to the policyholders, resulting in increased rates for all drivers, regardless of their driving record.

Several factors influence the high insurance rates in Michigan, apart from the no-fault insurance laws. One significant factor is inflation, which has impacted the cost of car repairs, medical bills, and auto parts. As a result, insurance companies face higher claim costs, which are then reflected in increased premiums for drivers.

Additionally, Michigan's severe winter weather, including lake-effect snow and black ice, contributes to more accidents and claims. The state's high number of deer-car collisions and the large percentage of uninsured drivers further drive up insurance costs. Legislative changes and economic factors, such as increased driving due to lower unemployment rates, also play a role in the rising insurance premiums.

It is worth noting that insurance rates in Michigan are also impacted by demographic factors. Age, for instance, can significantly affect insurance premiums. Younger drivers are considered riskier and tend to pay higher rates, with rates decreasing until the driver reaches the age of 62. After age 60, and more significantly after age 65, insurance rates tend to increase again due to factors such as potential reaction time and vision changes.

Understanding Driver Points and Their Impact on Insurance Rates

You may want to see also

Explore related products

![]()

Inflation and rising claim costs

Michigan has consistently had some of the highest insurance prices in the nation. Michigan drivers faced a 26% increase in auto insurance premiums in recent years. The Consumer Federation of America highlighted that inflation and rising claim costs are major contributors to these hikes. Inflation affects the cost of everything, including car repairs and medical bills. As the prices for these services rise, so do insurance premiums.

The cost of auto parts and repairs has risen sharply. Stephan Crewdson from J.D. Power explains that the cost of parts has gone up significantly, making repairs more expensive. This increase in repair costs means insurance companies have to pay out more when a claim is made, which in turn drives up premiums. For example, the price of a simple car part, like a bumper, has increased by 10% over the past year. When you multiply that by the number of claims insurers handle, the costs add up quickly.

The cost of claims has also been rising due to higher medical expenses. The Consumer Federation found that Michigan drivers paid an average of $2,133 annually for car insurance in 2022, down from $2,611 in 2019. However, with rising claim costs, this trend may reverse. The broader impact of inflation can’t be ignored either. Inflation affects not just car parts, but almost everything we buy. This includes consumer goods, which have seen price hikes across the board.

Another factor contributing to higher insurance premiums in Michigan is the Michigan Catastrophic Claims Association (MCAA) Fees. Starting July 1, 2023, drivers with unlimited Personal Injury Protection (PIP) coverage must pay $122 per vehicle, up from $86 the previous year. This fee hike addresses a $3.7 billion deficit in the MCAA fund, which reimburses insurance companies for medical costs exceeding $600,000 per claim. The deficit was partly caused by a recent court ruling that required the state to cover the lifetime medical costs for crash victims injured before the 2019 insurance reform.

Full Coverage Auto Insurance in Utah: What You Need to Know

You may want to see also

Explore related products

![]()

Extreme weather and accident rates

Extreme weather and high accident rates are key contributors to rising insurance costs in Michigan. The state experiences severe winter weather, including lake-effect snow and black ice, which result in more accidents and, consequently, higher insurance premiums. From 1980 to 2024, there were 60 confirmed weather/climate disaster events in Michigan, with losses exceeding $1 billion each. These events included flooding, severe storms, and winter storms.

In addition to extreme weather, Michigan also experiences a high number of deer-car collisions, and a large percentage of uninsured drivers, further contributing to rising insurance costs. The state's no-fault insurance system, legislative changes, and increased collision rates are also key factors in the rising cost of insurance in Michigan.

The frequency of accidents is a significant factor in determining insurance rates. In Michigan, accident rates have risen since 2020, contributing to the increase in premiums. Higher accident rates lead to more insurance claims, which drive up insurance costs. Poor weather conditions, such as heavy rain, dense fog, snow, ice, and slush, can reduce visibility and make it difficult for drivers to maintain control of their vehicles, increasing the risk of accidents.

Age is another factor that insurance companies consider when determining rates. In Michigan, insurance rates generally decrease with age, as younger, less-experienced drivers are considered riskier. However, rates may start to rise again after the age of 60 or 65, as older drivers may experience slower reaction times and poorer vision. According to CarInsurance.com, insurance rates typically increase by $44 per year from age 60 to 65 and continue to rise thereafter. Seniors over the age of 70 may face challenges in finding an insurer as they are considered a higher-risk group due to higher accident rates.

Insurency Sandstorm: Why Files Are Duplicated in Drives

You may want to see also

Explore related products

![]()

Age and risk profile

Age is a significant factor in determining insurance rates in Michigan. Insurance companies assign a risk profile to drivers based on their perceived experience level and age is a critical component of this assessment.

Younger drivers, especially those who are brand new to driving, are considered high-risk and tend to pay the highest insurance rates. In Michigan, 16-year-old drivers pay an average of $9,693 per year, while 20-year-olds pay about half of that amount. As drivers gain experience, their insurance rates decrease until they reach their early sixties.

After age 60, insurance rates start to increase again, with a more noticeable jump after age 65. This is because insurers assume that older drivers may have slower reaction times and poorer vision, which can increase the risk of accidents. The frequency of accidents is higher among older drivers, particularly those over 70, making it more challenging for them to find insurers willing to accept them as new customers.

However, some insurance providers offer discounts to senior drivers with clean driving records or those who complete approved defensive driving courses. These discounts can help offset the increase in insurance rates for older adults.

In Michigan, insurance rates are also influenced by factors such as location, driving record, vehicle type, and coverage level. Urban areas like Detroit have higher insurance rates due to higher crime rates, traffic congestion, and accident frequencies. Additionally, Michigan's unique no-fault insurance laws, which require Personal Injury Protection (PIP), contribute to higher insurance costs in the state.

Auto Insurance: Home Office Expense?

You may want to see also

Explore related products

![]()

Location and insurance rates

Location is a significant factor in determining insurance rates, and this is true for Michigan as well. Michigan has consistently had some of the highest insurance rates in the nation. The average Michigan driver pays $2,583 a year for car insurance, compared to the national average of $2,168 annually.

Several factors contribute to Michigan's high insurance rates, including the state's unique insurance laws, such as its no-fault insurance system and the requirement for Personal Injury Protection (PIP) coverage. This coverage helps pay for medical expenses after an accident, regardless of fault, but it also drives up insurance costs. In addition, Michigan has seen a recent increase in collision rates, severe winter weather, and a high number of deer-car collisions, all of which contribute to higher insurance premiums.

Within Michigan, insurance rates can vary significantly depending on the city or ZIP code. For example, drivers in Detroit, a city with a high crime rate and traffic congestion, face the highest rates in the state, paying around $5,667 per year for full coverage insurance. Hamtramck is another city with similar characteristics that experiences high insurance premiums. On the other hand, cities with lower crime rates and less traffic congestion will generally have lower insurance rates.

Insurers consider location when setting rates because it affects the risk they perceive. They use ZIP codes to gather information on various factors that can influence rates, including the frequency of car accidents, car theft and vandalism rates, claims rates, weather conditions, and the prevalence of uninsured drivers. These factors help insurers assess the likelihood of a claim being made, which directly impacts the insurance premiums charged to residents of a particular area.

Additionally, age is a critical factor in determining insurance rates. Insurance companies assign a risk profile to drivers based on their perceived experience level and physical capabilities. Younger drivers are considered riskier and tend to pay higher premiums, while rates decrease until the driver reaches their early 60s. After that, rates typically start to rise again, as insurers assume that older drivers may have slower reaction times and poorer vision, increasing the risk of accidents.

The Unemployment Effect: Auto Insurance Industry Trends and Insights

You may want to see also

Frequently asked questions

Yes, insurance rates in Michigan increase after the age of 65. This is due to insurance companies assigning a risk profile to drivers based on their perceived experience level and health. While drivers in their 40s can often expect to get cheap insurance rates, rates for older drivers start to creep up once they reach their 70s.

The average insurance rate for a 50-year-old driver in Michigan is $2,730 per year. This decreases by 255% by the time the driver reaches 62, but then starts to increase again. The exact rate will depend on the driver's location, driving record, and vehicle type.

Michigan has some of the highest insurance rates in the nation due to a variety of factors, including severe winter weather, high accident rates, and legislative changes. The state's no-fault insurance laws, which require drivers to carry Personal Injury Protection (PIP), also drive up insurance costs.