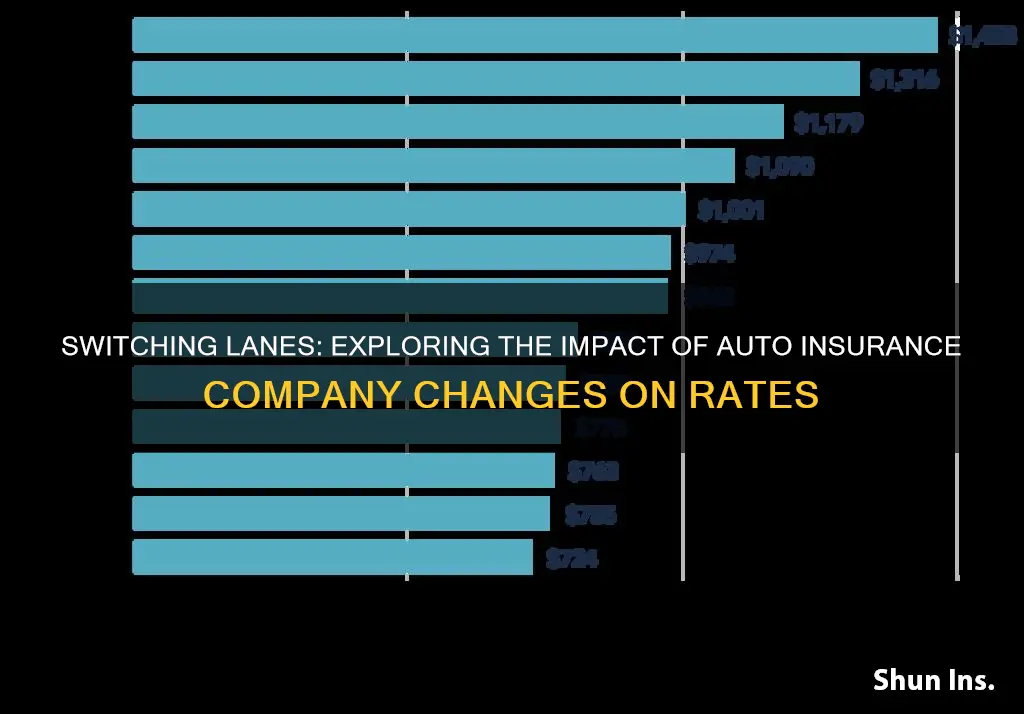

Changing auto insurance companies is relatively painless and can save you money, or help you get stronger customer service or a policy better tailored to your needs. You can switch at any time, even if you just renewed your policy, and it won't affect your credit score. However, you may be charged a cancellation fee, and you will need to ensure there is no lapse in coverage between the end of your former policy and the beginning of your new one.

Explore related products

![ESSENTIAL Car Auto Insurance Registration BLACK Document Wallet Holders 2 Pack - [BUNDLE, 2pcs] - Automobile, Motorcycle, Truck, Trailer Vinyl ID Holder & Visor Storage - Strong Closure On Each -](https://m.media-amazon.com/images/I/61px7jy3NmL._AC_UL320_.jpg)

What You'll Learn

![]()

Cancellation fees and refunds

To avoid cancellation fees, you can wait until the end of your policy and choose not to renew. You can also check with your current insurance company to see if they charge a cancellation fee and how much it is. If you have prepaid your premiums, you can ask your insurance company if you can receive a prorated refund. It is also a good idea to initiate coverage with a new insurer prior to cancellation to avoid a lapse in coverage, which can result in high out-of-pocket costs in the event of an accident while uninsured.

When switching auto insurance companies, it is important to follow the proper steps to ensure a smooth transition. First, determine the amount of coverage you need and compare quotes from multiple companies to find the best deal. Then, buy your new insurance policy and set an activation date. Make sure your new policy is active before cancelling your old policy to avoid an illegal lapse in coverage. Finally, cancel your old policy and carry your new insurance ID.

F Endorsement and Auto Insurance: What's the Real Cost?

You may want to see also

Explore related products

![]()

Adjusting your coverage

Adjusting your auto insurance coverage is a great way to save money on your monthly premiums. Here are some ways you can adjust your coverage:

- Reduce your coverage: If you have an older car that isn't worth much, you may want to consider dropping collision and comprehensive coverage. You can also lower your policy limits to reduce your premium. However, make sure you're still complying with your state's insurance laws and any coverage requirements from your lender or lessor.

- Increase your deductible: Raising your deductible will lower your premium. For example, going from a $250 to a $500 deductible could reduce the cost of your collision and comprehensive coverage by up to 30%. Just be mindful of your budget, as a higher deductible means you'll pay more out of pocket when you file a claim.

- Drop add-ons: Evaluate your coverage needs and remove any add-ons that you no longer require. For example, if you're working from home or retired and driving less, you may not need roadside assistance.

- Adjust your liability limits: If you want your insurance to pay more than the state-required minimums for bodily injury and property damage after an accident, you'll need to increase your liability limits.

- Take advantage of discounts: Most major insurers offer discounts based on your driving history, vehicle features, and policy choices. For example, many insurers offer discounts for going paperless, paying online, or agreeing to automated payments. Review all the discounts offered by your insurer to maximize your savings.

- Compare rates: Shop around for lower rates by getting quotes from multiple insurers. Compare the prices and coverage options to find the best deal. It's recommended to get at least three quotes and to comparison shop every 6-12 months when your policy is up for renewal.

Aetna Insurance: Understanding the Gap Phase

You may want to see also

Explore related products

![]()

Changing your deductible

Raising your deductible will usually result in a lower rate, whereas reducing your deductible will increase your rate. For instance, if you increase your deductible from $500 to $1,000, your rate will likely drop. On the other hand, decreasing your deductible from $1,000 to $500 will probably cause your rate to increase.

It's important to note that changing your deductible won't impact what you pay if you've already filed a claim. The coverage that applies is based on the date and time the loss occurred. Additionally, changing your deductible within 90 days of a claim can be a red flag for insurance companies, as it may suggest an element of fraud. Therefore, it's best to wait a few months after closing a claim before making any changes to your deductible.

Gap Insurance: Worth the Cost?

You may want to see also

Explore related products

![]()

Adding or removing drivers

Adding or removing a driver from your auto insurance policy is a straightforward process, but it may vary depending on your insurance provider and policy. Here are the general steps to guide you through the process:

Adding a Driver

- Contact your insurance provider: Notify your insurance provider that you would like to add a driver to your auto insurance policy. This can typically be done by phone or through your insurance company's online portal.

- Provide driver information: You will need to provide relevant information about the driver, including their full name, date of birth, driver's license number, and driving history. Some insurance companies may also require details such as the driver's relationship to you, their address, and their driving experience.

- Underwriting process: The insurance company will assess the driver's risk profile based on factors like their age and driving record. This assessment helps determine the impact on your policy's premium.

- Premium adjustment: Depending on the driver's risk profile, your insurance premium may increase or decrease. Your insurance provider will inform you of the updated premium amount and any payment adjustments.

- Policy documentation: Once the driver has been added, your insurance provider will send you updated policy documents. Carefully review these documents to ensure their accuracy.

Removing a Driver

- Contact your insurance provider: Notify your insurance provider of your intention to remove a driver from your auto insurance policy, providing them with the driver's full name and date of birth.

- Verification of the driver's status: Your insurance provider may require confirmation that the driver is no longer using your insured vehicle. This may include verifying that the driver has obtained their own insurance policy or no longer resides with you.

- Adjusted premium: Removing a driver from your policy can result in a premium adjustment. The impact on your premium will depend on factors such as the driver's risk profile and the number of remaining drivers on the policy. Your insurance provider will inform you of the updated premium amount and any necessary payment adjustments.

- Updated policy documents: After the driver has been removed, your insurance provider will send you updated policy documents. Review these documents to ensure they accurately reflect the changes.

It is important to note that the process of adding or removing a driver may differ depending on your insurance provider's specific procedures. Contact your insurance company or agent directly to obtain the most accurate and up-to-date information.

Temporary Licenses and Auto Insurance: What's the Deal?

You may want to see also

Explore related products

![]()

Adding or removing vehicles

For example, if you decide to go from being a two-car household to a one-car household and sell your old minivan, removing the minivan from your policy will likely trigger a rate decrease. On the other hand, if you add a second car to your insurance, your rate will almost certainly go up.

It's important to note that the specific impact on your rates will depend on the make and model of the vehicle you're adding or removing, as well as other factors such as your location and driving history.

When making changes to your auto insurance policy, it's always a good idea to shop around and compare quotes from multiple companies to ensure you're getting the best rate. You can also speak to your insurance agent to discuss any other cost-saving measures that may be available to you.

Collision Insurance: Protection Against Crash Costs

You may want to see also