Gender has traditionally been a factor in setting insurance premiums, with men and women paying different rates for various types of insurance. While gender-based pricing is still prevalent in most US states, several states have banned the practice, and the debate remains open. The use of gender in insurance pricing is influenced by factors such as regulations, individual risk profiles, and the specific policies of insurance companies and states. Statistical data plays a crucial role in these determinations, with young male drivers often considered higher-risk due to their higher likelihood of accidents. However, gender is not the sole factor in determining insurance rates, and other considerations, such as age, driving record, and vehicle type, also come into play.

| Characteristics | Values |

|---|---|

| Gender affecting insurance rates | In the US, insurance companies may use gender to determine insurance rates. |

| Gender X rates | There are no guidelines in Canada for setting rates for gender X drivers. Some insurers offer rates similar to female drivers, while others use the average between male and female rates. |

| Gender as a risk factor | Insurance companies traditionally tie gender to an applicant's risk, with men being considered higher-risk drivers. |

| Gender-based pricing | Men typically pay more for car insurance than women, especially in the 18-25 age group. |

| Regulatory environment | The use of gender in insurance pricing varies by state and insurance provider. Some states prohibit or limit its use, while others allow it with no restrictions. |

| Consumer preference | Individuals, consumer advocates, and politicians prefer that insurance premiums are based on controllable factors such as behaviour rather than gender. |

| Transgender and non-binary individuals | Depending on the insurance company and state, transgender and non-binary individuals may have to identify as male or female when applying for insurance. |

Explore related products

$12.82 $16.95

$24.95

What You'll Learn

![]()

Gender and risk

In the places where gender is used as a factor, men typically pay more for car insurance than women, as they are considered to be higher-risk drivers. However, this is not always the case, and some women may be charged more for their insurance than men. Additionally, women over 25 are often charged more than men of the same age.

The use of gender in setting insurance rates is based on statistical analysis. Men, especially those between the ages of 18 and 25, are more likely to be involved in accidents than women. They are also more likely to engage in riskier driving behaviours, such as speeding and aggressive driving. Women, on the other hand, are generally considered safer drivers and are less likely to be involved in serious accidents. They are, however, more frequently involved in injury crashes and are more likely to make insurance claims.

While gender may be a factor in setting insurance rates, it is not the only one. Other factors that insurance companies consider include age, driving record, vehicle type, individual credit scores, and where the applicant lives.

Understanding Excess Medical Auto Insurance Coverage

You may want to see also

Explore related products

$21.99

$21.99

$21.99

![]()

Gender-neutral insurance rates

In the context of car insurance, gender has traditionally been a significant rating factor, with men often paying higher premiums than women, particularly among younger drivers. However, there has been a growing movement towards gender-neutrality in the industry. As of 2021, over 20 US states offer gender-neutral options on driver's license forms, and some states, like California, Hawaii, Massachusetts, Montana, North Carolina, and Pennsylvania, have banned the use of gender in setting car insurance rates.

Insurers typically justify using gender as a criterion for premiums by citing actuarial soundness, claiming that it reflects differences in risk levels between genders. For example, historical data suggests that young male drivers are more likely to be involved in accidents and file more claims, leading to higher premiums. However, consumer advocates argue that insurance rates should be based on controllable factors such as behaviour, rather than inherent characteristics like gender.

The impact of gender on insurance rates varies across different types of insurance and geographical locations. For instance, in the United States, gender is a permitted factor in determining car insurance rates in most states, while several European countries have introduced rules prohibiting gender discrimination in insurance pricing.

The inclusion of non-binary gender identities in insurance applications is another aspect of the gender-neutral insurance rates discussion. While some insurers accommodate non-binary individuals, they may still be required to identify as male or female, depending on their state and the insurer's policies. The situation is similar for transgender individuals, who may face challenges in obtaining affordable insurance due to potential higher rates associated with mental and physical health considerations.

Finding the Best Auto Insurance Rates in Wisconsin

You may want to see also

Explore related products

$21.99

$21.99

![]()

Gender X insurance rates

The use of gender as a factor in setting insurance rates has been a long-standing practice. However, the inclusion of "Gender X" on driver's licenses in Ontario, Canada, has introduced a new dimension to insurance rate calculations. Currently, there are no standard guidelines in Canada for determining insurance rates for individuals with the "Gender X" marker. Insurance companies employ different approaches, with some offering rates comparable to those for female drivers, while others use an average of male and female rates.

The lack of uniform guidelines can lead to inconsistencies in insurance rates for individuals with the "Gender X" identifier. To navigate this situation, it is advisable for "Gender X" individuals to consult a broker and explore multiple insurance providers to find the most suitable rates. While the use of gender in insurance pricing is being contested and regulated in various states and countries, it is still a prevalent factor in many regions.

In the context of auto insurance, gender has traditionally been a significant factor in setting rates, with men often paying more than women due to statistical data indicating a higher risk of accidents. However, this trend is not universal, and certain states and countries have banned the use of gender as an underwriting factor. For example, California has introduced a nonbinary option on driver's licenses and prohibited gender as a rating factor.

The consideration of gender in insurance rates extends beyond auto insurance. Health insurance and long-term care insurance are other areas where gender has been a factor in rate-setting, leading to debates about gender-based price discrimination. As societal views on gender evolve, insurance companies are increasingly challenged to reevaluate their criteria for determining rates and move towards more equitable practices.

While the absence of standard guidelines for "Gender X" insurance rates in Canada may present challenges, it also underscores the evolving nature of gender's role in insurance. As more jurisdictions question the fairness of using gender as an underwriting factor, individuals with diverse gender identities may anticipate more inclusive insurance practices in the future. In the interim, shopping around for insurance and working with knowledgeable brokers remain essential steps for "Gender X" individuals to secure the most favourable rates.

How Much Does Family Auto Insurance Cost Monthly?

You may want to see also

Explore related products

![]()

Gender and insurance rates by state

The use of gender as a factor in setting insurance rates has been a topic of debate and investigation by many state insurance regulators. In the United States, insurance companies traditionally tie gender to an applicant's risk, and it is often considered when setting premiums. However, this practice is not uniform across all states, and regulations vary regarding the inclusion of gender as a rating factor.

In most states, gender plays a role in determining car insurance rates. Men generally pay higher premiums than women in these states, with statistics indicating that they are considered higher-risk drivers. However, this trend is not consistent across all states or insurance companies, and some states have actively outlawed the use of gender as a rating factor. California, Hawaii, Massachusetts, Montana, North Carolina, and Pennsylvania have banned the use of gender in setting insurance rates.

The impact of gender on insurance rates extends beyond car insurance to other types of insurance as well. Studies have shown that women over the age of 25 tend to pay more for car insurance than men, and gender can also influence health insurance premiums. The consideration of gender in insurance rates is based on the notion of risk assessment, with insurance companies arguing that gender is an actuarially sound criterion.

While gender has been a historical factor in insurance rates, there is a growing preference for premiums to be based on controllable factors such as behaviour rather than inherent characteristics like gender. In recent years, the focus has shifted to other rating factors, such as credit scores, which can have a significant impact on insurance rates. The variation in credit scores between men and women has been suggested as a contributing factor to the changing landscape of gender-based insurance rates.

The specific impact of gender on insurance rates can vary by state, and it is essential to consider the unique regulations and practices of each state. While gender may be a factor in some states, it is not the sole determinant of insurance rates, and other factors such as driving history, age, and location also play a significant role in the final premium amount. Shopping around for insurance and considering multiple carriers can help individuals find the most favourable rates, as each company may rate risks differently.

Max Auto Insurance: Is It Worth the Hype?

You may want to see also

Explore related products

![]()

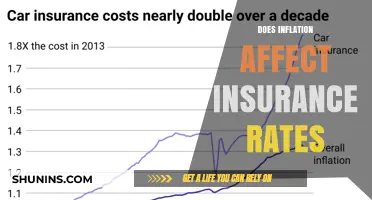

Gender and insurance rates over time

Gender has traditionally been one of the factors that insurers consider when setting premiums. However, in recent years, there has been a pushback against this practice, with some states and countries prohibiting the use of gender as a rating factor. Despite this, gender continues to influence insurance rates in various ways.

Historically, women have paid more for health and life insurance, while men have paid more for car insurance. Before the implementation of the Affordable Care Act (ACA), women were charged up to 80% more for health insurance on the individual market. The ACA now prohibits insurers from using gender as a factor in setting health insurance premiums, making the pricing more equitable. Similarly, in the European Union, a 2012 nondiscrimination law has likely contributed to more gender-neutral insurance rates.

In the case of car insurance, women tend to pay less than men due to lower accident rates and fewer serious accidents. This difference is most pronounced among younger drivers, with men under 20 paying 14% more than women of the same age. However, the gap narrows as drivers age, with minimal differences in premiums between men and women in their 30s. Over the last few years, the gender gap in car insurance rates has decreased, with women paying less in the majority of states.

When it comes to disability insurance, women, particularly those in the medical field, often face higher premiums. This is because they tend to file more disability claims and are disabled for longer periods. On the other hand, men typically pay more for life insurance. Actuaries, employed by insurance companies, assess risk using statistical models and consider gender, along with other factors like age, health, and occupation, when determining insurance rates.

While the impact of gender on insurance rates has diminished over time, it still plays a role in certain types of insurance. The trend towards gender-neutral rates is gaining momentum, with more states and countries enacting laws to prohibit gender-based discrimination in insurance pricing.

The Myth of Red Cars: Higher Insurance Rates?

You may want to see also

Frequently asked questions

Yes, gender does affect insurance rates. Men are often associated with riskier driving behaviours and are statistically more likely to be involved in accidents, resulting in higher insurance premiums.

Insurance companies use gender to assess risk based on driving patterns and accident statistics. Men, especially those between the ages of 18 and 25, are more likely to be involved in accidents and are thus considered higher-risk drivers. This results in insurance companies charging higher premiums to insure them.

Insurance companies traditionally tie gender to an applicant's risk and use it as a factor when setting premiums. They argue that gender is an actuarially sound criterion for establishing premiums.

The impact of gender on insurance rates varies by state and insurance provider. Some states prohibit the use of gender in setting insurance rates, while others allow it with limitations. It's important to shop around and compare rates from multiple insurance companies to find the best rates for your specific circumstances.